|

市場調査レポート

商品コード

1721625

ビルオートメーション用エネルギーハーベスティング市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Building Automation Energy Harvesting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ビルオートメーション用エネルギーハーベスティング市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月08日

発行: Global Market Insights Inc.

ページ情報: 英文 138 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

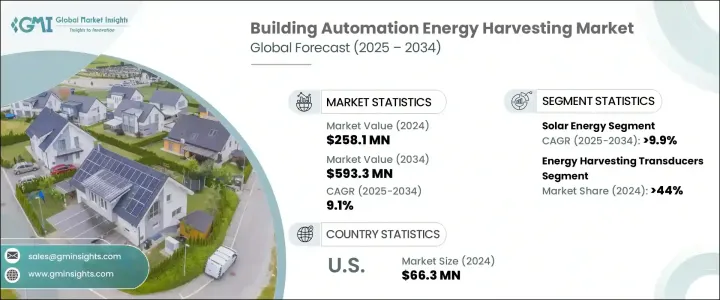

世界のビルオートメーション用エネルギーハーベスティング市場は、2024年に2億5,810万米ドルと評価され、CAGR 9.1%で成長し、2034年には5億9,330万米ドルに達すると予測されています。

この顕著な成長軌道は、住宅と商業環境の両方でインテリジェントエネルギーシステムへのシフトが広がっていることを反映しています。持続可能性が各業界の中心になるにつれ、ビル事業者、施設管理者、開発者は、運用コストを下げながらエネルギー効率を高める自動化技術の採用を増やしています。HVACシステムから照明、高度なセキュリティ・ネットワークに至るまで、オートメーションは最新のビル設計に不可欠なものとなりつつあります。この変革は、ゼロ・エミッション構造の世界の推進、エネルギー使用に関する政府の厳しい義務付け、従来のエネルギー源のコスト上昇によってさらに拍車がかかっています。消費者も企業も同様に、環境に優しい住環境や職場環境を優先しており、外部エネルギー・グリッドへの依存を最小限に抑えるエネルギー・ハーベスティング・ソリューションに対する旺盛な需要を生み出しています。加えて、モノのインターネット(IoT)とAI対応プラットフォームの普及拡大により、自動化技術のシームレスな統合という新たな機会が生まれ、よりスマートで応答性の高いインフラへの道が開かれました。

エネルギー効率が世界的に重要な関心事となるにつれ、照明、HVAC、厨房機器、セキュリティ・ユニットなどの自動化システムが台頭し続けています。ビルは、従来のエネルギー源への依存を減らし、全体的な運用管理を改善する高度な制御システムを備えています。排出量の削減と建物効率の向上に焦点を当てた規制の枠組みが、建設業者や不動産所有者にスマート技術の採用を促しています。エネルギーハーベスティングは、長期的に大幅なエネルギー節約を実現しながら、これらの規制へのコンプライアンスを確保するための重要な要素として浮上しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2億5,810万米ドル |

| 予測金額 | 5億9,330万米ドル |

| CAGR | 9.1% |

太陽エネルギーは、インテリジェントビルへの移行において依然として圧倒的な力を持っており、その分野は2034年までCAGR 9.9%で成長すると予測されています。気候に対する懸念の高まりと、自給自足の電力システムに対する需要の高まりが、ビル分野での太陽光発電の採用を加速しています。ソーラー技術はビルオートメーションプラットフォームと容易に統合でき、暖房、冷房、照明などの重要な機能にクリーンエネルギーを供給します。これにより、電気代が削減されるだけでなく、不動産所有者や開発業者にとって、エネルギーの自立と環境に対する責任が強化されます。

コンポーネントでは、エネルギーハーベスティング変換器が2024年の市場シェアの44%を占めています。これらのデバイスは、ワイヤレスでセルフパワーのセンサーネットワークをサポートし、バッテリー交換や複雑な配線の必要性を排除します。照明、温度制御、居住検知、セキュリティ・システムに応用することで、エネルギー管理の合理化と持続可能な運用が可能になります。スマートビルディングの基盤要素として、変換器は最小限のメンテナンスで拡張可能なエネルギー制御を提供し、効率的なビルのアップグレードをサポートします。

アジア太平洋ビルオートメーション用エネルギーハーベスティング市場は、急速な都市化と建設活動の増加により、2024年には24%のシェアを占める。この地域の国々は、進化する持続可能性の目標に沿うため、エネルギー収集オートメーションに支えられたグリーンビルディングの実践を採用しています。政府主導の取り組みとスマート不動産ソリューションに対する需要の高まりが、地域市場の拡大をさらに加速させています。

主要企業には、ZF Friedrichshafen AG、Perpetua Power、Advanced Linear Devices, Inc.、EnOcean GmbH、Texas Instruments Incorporated、Renesas Electronics Corporation、Cedrat Technologies、STMicroelectronics、Mide Technology Corp.、Laird Connectivity、ABB、Honeywell、Kinergizer、富士通、Mouser Electronics、Powercast Corporationなどがあります。主要企業は、トランスデューサとPMICの性能と統合を強化するため、研究開発に多額の投資を行っています。オートメーション開発企業、インフラ・プロジェクト、公共プログラムとの戦略的提携は、世界なプレゼンスの拡大に役立っています。さらに、改修や新築向けにカスタマイズされたカスタムIoTベースのソリューションが人気を集め、オートメーション機能を強化し、長期的な市場成長を促進しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- トランプ政権の関税が貿易と産業全体に与える影響

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:ソース別、2021-2034

- 主要動向

- 太陽エネルギー

- 振動と運動エネルギー

- 熱エネルギー

- 無線周波数(RF)

- その他

第6章 市場規模・予測:コンポーネント別、2021-2034

- 主要動向

- エネルギーハーベスティングトランスデューサー

- 電源管理集積回路(PMIC)

- その他

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- Advanced Linear Devices、Inc.

- Cedrat technologies

- EnOcean GmbH

- Fujitsu

- Honeywell

- Kinergizer

- Laird Connectivity

- Mide Technology Corp.

- Mouser Electronics

- Perpetua Power

- Powercast Corporation

- Renesas Electronics Corporation

- STMicroelectronics

- Texas Instruments Incorporated

- ZF Friedrichshafen AG

The Global Building Automation Energy Harvesting Market was valued at USD 258.1 million in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 593.3 million by 2034. This remarkable growth trajectory reflects a widespread shift toward intelligent energy systems across both residential and commercial environments. As sustainability takes center stage across industries, building operators, facility managers, and developers are increasingly adopting automation technologies that drive energy efficiency while lowering operational costs. From HVAC systems to lighting and advanced security networks, automation is becoming integral to modern building design. This transformation is further fueled by the global push for zero-emission structures, stringent government mandates on energy usage, and the rising costs of conventional energy sources. Consumers and businesses alike are prioritizing eco-friendly living and working environments, creating robust demand for energy harvesting solutions that minimize reliance on external energy grids. In addition, the growing penetration of the Internet of Things (IoT) and AI-enabled platforms has unlocked new opportunities for seamless integration of automation technologies, paving the way for smarter, more responsive infrastructure.

As energy efficiency becomes a critical global concern, automated systems for lighting, HVAC, kitchen appliances, and security units continue to gain ground. Buildings are equipped with advanced control systems that reduce dependence on traditional energy sources and improve overall operational management. Regulatory frameworks focused on reducing emissions and increasing building efficiency are prompting builders and property owners to embrace smart technologies. Energy harvesting is emerging as a key component in ensuring compliance with these regulations while delivering significant long-term energy savings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $258.1 million |

| Forecast Value | $593.3 million |

| CAGR | 9.1% |

Solar energy remains a dominant force in the transition toward intelligent buildings, with its segment projected to grow at a CAGR of 9.9% through 2034. Growing climate concerns and the rising demand for self-sufficient power systems are accelerating solar adoption in the building sector. Solar technologies integrate easily with building automation platforms, providing clean energy to power critical functions such as heating, cooling, and lighting. This not only reduces electricity bills but also enhances energy independence and environmental responsibility for property owners and developers.

In terms of components, energy-harvesting transducers accounted for 44% of the market share in 2024. These devices support wireless and self-powered sensor networks, eliminating the need for battery changes or complex wiring. Their application in lighting, temperature control, occupancy sensing, and security systems ensures streamlined energy management and sustainable operations. As a foundational element of smart building infrastructure, transducers offer scalable energy control with minimal maintenance, supporting efficient building upgrades.

The Asia Pacific Building Automation Energy Harvesting Market held a 24% share in 2024, driven by rapid urbanization and increasing construction activity. Nations across the region are adopting green building practices supported by energy-harvesting automation to align with evolving sustainability goals. Government-led initiatives and rising demand for smart real estate solutions are further accelerating regional market expansion.

Key players include ZF Friedrichshafen AG, Perpetua Power, Advanced Linear Devices, Inc., EnOcean GmbH, Texas Instruments Incorporated, Renesas Electronics Corporation, Cedrat Technologies, STMicroelectronics, Mide Technology Corp., Laird Connectivity, ABB, Honeywell, Kinergizer, Fujitsu, Mouser Electronics, and Powercast Corporation. Leading companies are investing heavily in R&D to enhance transducer and PMIC performance and integration. Strategic alliances with automation developers, infrastructure projects, and public programs are helping broaden their global presence. Additionally, custom IoT-based solutions tailored for retrofitting and new builds are gaining traction, enhancing automation capabilities and driving long-term market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Impact of Trump administration tariffs on trade & overall industry

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Source, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Solar energy

- 5.3 Vibration & kinetic energy

- 5.4 Thermal energy

- 5.5 Radio Frequency (RF)

- 5.6 Others

Chapter 6 Market Size and Forecast, By Component, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Energy harvesting transducer

- 6.3 Power Management Integrated Circuits (PMIC)

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Advanced Linear Devices, Inc.

- 8.3 Cedrat technologies

- 8.4 EnOcean GmbH

- 8.5 Fujitsu

- 8.6 Honeywell

- 8.7 Kinergizer

- 8.8 Laird Connectivity

- 8.9 Mide Technology Corp.

- 8.10 Mouser Electronics

- 8.11 Perpetua Power

- 8.12 Powercast Corporation

- 8.13 Renesas Electronics Corporation

- 8.14 STMicroelectronics

- 8.15 Texas Instruments Incorporated

- 8.16 ZF Friedrichshafen AG