|

市場調査レポート

商品コード

1928962

往復動エンジン市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Reciprocating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 往復動エンジン市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月13日

発行: Global Market Insights Inc.

ページ情報: 英文 245 Pages

納期: 2~3営業日

|

概要

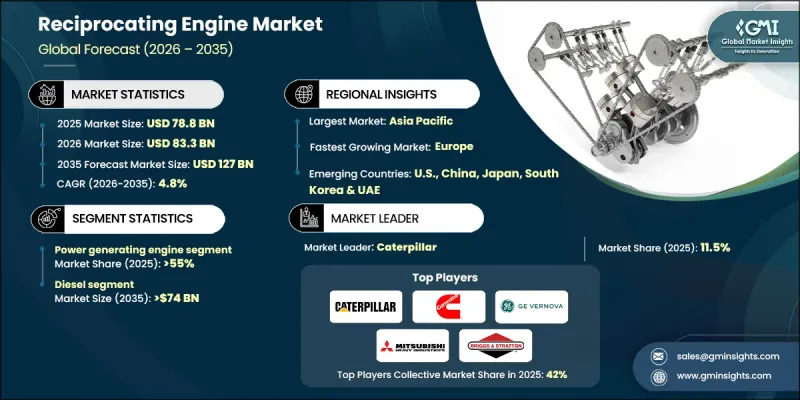

世界の往復動エンジン市場は、2025年に788億米ドルと評価され、2035年までにCAGR 4.8%で成長し、1,270億米ドルに達すると予測されております。

市場成長は、運用柔軟性と保守容易性を高めるモジュール化・簡素化されたエンジン設計の継続的な革新によって推進されています。燃料効率技術の導入拡大と厳格な排出規制が相まって、次世代往復動エンジンの形成が進んでいます。先進的なデジタル監視システムと予知保全ツールの統合により、信頼性が向上し、ダウンタイムが最小化されています。現代の往復動エンジンは、堅牢なエンジニアリングと運用戦略を組み合わせ、多様な用途において一貫した効率的な動力を提供します。燃焼効率の向上、熱的安定性の維持、複数燃料タイプへの対応を実現しています。産業用、商業用、分散型発電システムに及ぶ用途において、これらのエンジンはエネルギーレジリエンスを支えると同時に、再生可能エネルギー源とのシームレスな統合を可能にします。ハイブリッド技術、燃料最適化、制御システムの進歩により性能がさらに向上し、非常用電源と連続発電の両方に理想的な選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 788億米ドル |

| 予測金額 | 1,270億米ドル |

| CAGR | 4.8% |

2025年時点で電力セグメントは55%のシェアを占めており、2035年までCAGRCAGR4%で成長が見込まれます。その拡大は、信頼性の高い電力ソリューションへの需要増加、柔軟なモジュール設計、分散型発電システムの導入拡大によって支えられています。このセグメントにおけるレシプロエンジンは、起動が速いこと、高効率であること、再生可能エネルギーとの統合性に優れていることから好まれています。

ガスエンジンセグメントは、窒素酸化物、二酸化硫黄、粒子状物質の排出量が少ないことから、2035年までにCAGR5.5%で成長すると予測されています。これらのクリーンな運転特性により、環境規制や地球規模の持続可能性目標への準拠を優先する企業にとって、ガスエンジンは魅力的な選択肢となっています。

北米の往復動エンジン市場は、エネルギーインフラの近代化、高性能・低排出エンジンへの移行、継続的な産業拡大により、2035年までに200億米ドル規模に達すると予測されています。エンジン性能と効率性における継続的な技術革新が、同地域全体の市場見通しをさらに強化すると見込まれます。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 原材料の入手可能性と調達分析

- 製造能力評価

- サプライチェーンのレジリエンスとリスク要因

- 流通ネットワーク分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 往復動エンジンのコスト構造分析

- 価格動向分析(米ドル/MW)

- 地域別

- 定格出力別

- 新たな機会と動向

- デジタル化とIoT統合

- 新興市場への進出

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的ダッシュボード

- 戦略的取り組み

- 主要な提携・協力関係

- 主要なM&A活動

- 製品革新と新製品発売

- 市場拡大戦略

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:燃料別、2022-2035

- ディーゼル

- ガス

- その他

第6章 市場規模・予測:定格出力別、2022-2035

- 0.5 MW~1 MW

- 1MW超~2MW

- 2MW超~3.5MW

- 3.5MW超~5MW

- 5MW超~7.5MW

- 7.5MW超

第7章 市場規模・予測:用途別、2022-2035

- 電力

- 船舶

- 機械

第8章 市場規模・予測:シリンダー構成別、2022-2035

- 直列

- V型

- ラジアル

- 対向ピストン

第9章 市場規模・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- スペイン

- オランダ

- デンマーク

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- タイ

- シンガポール

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- オマーン

- クウェート

- エジプト

- トルコ

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第10章 企業プロファイル

- AB Volvo Penta

- Briggs &Stratton

- Caterpillar

- Cummins

- GE Vernova

- Guascor Energy

- Honda Motor

- IHI Corporation

- J C Bamford Excavators

- Kawasaki Heavy Industries

- KUBOTA Corporation

- Lister Petter

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Perkins Engines

- Rehlko

- Rolls-Royce

- Wartsila

- Yamaha Motor

- Yanmar Holdings