|

市場調査レポート

商品コード

1721592

バイオフォトニクス市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Biophotonics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| バイオフォトニクス市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月10日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

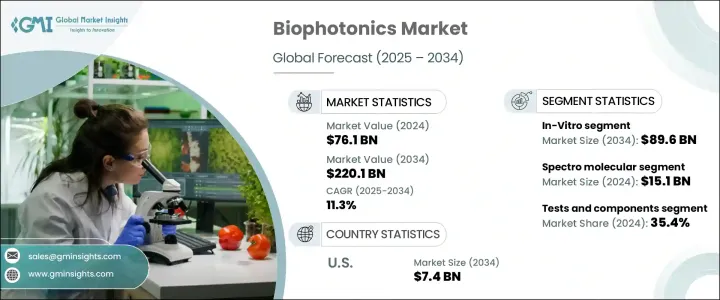

世界のバイオフォトニクス市場は、2024年に761億米ドルと評価され、CAGR 11.3%で成長し、2034年には2,201億米ドルに達すると推定されています。

この顕著な成長軌道は、医療技術の急速な進歩と、診断および治療プラットフォーム全体におけるナノテクノロジーの加速的な統合が主な要因です。ナノスケールで光と物質の相互作用を強化するナノテクノロジーの能力は、生体システムの分析方法に革命をもたらし、バイオフォトニックデバイスをより効率的で精密なものにしています。これらの技術は現在、バイオマーカーの検出や組織の画像化において感度と特異性を向上させ、特に初期段階の疾患検出において、より正確な診断とオーダーメイド治療への道を開いています。

非侵襲的な処置やリアルタイム診断が重視されるようになり、バイオフォトニック・イノベーションに対する需要はヘルスケア環境全体で急増しています。正確な分子データに大きく依存する個別化医療への世界の注目の高まりは、高度な光学技術の必要性をさらに強めています。技術進化と同時に、ヘルスケア業界では研究開発、自動化、データ主導の意思決定への投資が拡大しており、研究、診断、治療にわたるバイオフォトニックアプリケーション合理化に役立っています。さらに、世界の慢性疾患の増加により、効率的で正確かつ迅速な診断方法の探求が深まっており、これも市場の持続的拡大に寄与しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 761億米ドル |

| 予測金額 | 2,201億米ドル |

| CAGR | 11.3% |

技術は、In-VitroプラットフォームとIn-Vivoプラットフォームに二分されます。このうち、In-Vitro分野は顕著な成長を記録しており、2034年までに896億米ドルに達すると予測されています。この急成長の主な要因は、ラボベースの診断における画期的な進歩、AI主導の分析と自動化の統合です。これらの進歩は、人為的ミスを最小限に抑え、業務効率を高め、検査室のワークフローをより正確で迅速なものにしています。ヘルスケア部門が疾患の早期発見を優先し続ける中、In-Vitroバイオフォトニック・プラットフォームの採用は急速に拡大しています。

用途別では、シースルーイメージング、顕微鏡、インサイドイメージング、分光分子、分析センシング、光治療、表面イメージング、バイオセンサーなど、さまざまなセグメントにまたがっています。分光分子セグメントは圧倒的な市場シェアを占め、2024年の市場規模は151億米ドル。この分野でのリーダーシップは、分子レベルでの感度と診断精度を向上させた分光ツールの進化によるものです。これらのツールは、疾病に関連する生化学的変化を特定する上で重要な役割を果たしており、これにより早期かつ個別化された介入戦略を可能にしています。

最終用途の観点から、市場は検査とコンポーネント、医療診断、医療治療、非医療用途に区分されます。検査・コンポーネント分野は2024年に35.4%と最大のシェアを占め、高度な診断ツールや精密画像技術の需要増に支えられています。

地域別では、米国が北米バイオフォトニクス市場をリードしており、2034年には74億米ドルの市場規模に達すると予測されています。これは、研究開発支出の多さ、高度なヘルスケアインフラ、慢性疾患の負担増に対応した高度診断ソリューションの需要増が背景にあります。

この業界は、サーモフィッシャーサイエンティフィック社、カールツァイス社、浜松ホトニクス株式会社、オリンパス株式会社、オックスフォード・インストゥルメンツ社などの主要企業が市場の55%から60%を占めており、緩やかな統合が続いています。これらの企業は高精度のバイオフォトニック技術への投資を続け、競争力を強化するために地理的な足跡を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ナノテクノロジーの出現

- 高齢化と生活習慣病の増加

- 細胞・組織診断におけるバイオフォトニクスの使用増加

- 家庭用POCデバイスの需要増加

- AIとMLとの統合の高まり

- 業界の潜在的リスク&課題

- 技術コストの高さ

- 商業化の遅い速度

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:技術別、2021 –2034

- 主要動向

- 体外

- 生体内

第6章 市場推計・予測:用途別、2021 –2034

- 主要動向

- シースルーイメージング

- 顕微鏡検査

- 内部イメージング

- 分光分子

- 分析センシング

- 光療法

- 表面イメージング

- バイオセンサー

第7章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- テストとコンポーネント

- 医療治療

- 医療診断

- 非医療用途

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- オーストラリア

- 韓国

- 日本

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第9章 企業プロファイル

- Becton、Dickinson and Company

- Carl Zeiss AG

- Glenbrook Technologies

- Hamamatsu Photonics K.K

- IDEX

- IPG Photonics Corporation

- NU Skin Enterprises

- Olympus Corporation

- Oxford Instruments PLC

- PerkinElmer Inc.

- Thermo Fisher Scientific

- TOSHIBA CORPORATION

- Zecotek Photonics Inc.

- Zenalux Biomedical Inc

The Global Biophotonics Market was valued at USD 76.1 billion in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 220.1 billion by 2034. This remarkable growth trajectory is largely driven by rapid advancements in medical technology and the accelerating integration of nanotechnology across diagnostic and therapeutic platforms. The ability of nanotechnology to enhance light-matter interactions at the nanoscale has revolutionized the way biological systems are analyzed, making biophotonic devices more efficient and precise. These technologies now offer increased sensitivity and specificity when detecting biomarkers and imaging tissues, paving the way for more accurate diagnostics and tailored treatments, especially in early-stage disease detection.

With a growing emphasis on non-invasive procedures and real-time diagnostics, the demand for biophotonic innovations is surging across healthcare settings. The increasing global focus on personalized medicine, which relies heavily on precise molecular data, further reinforces the need for advanced optical technologies. Alongside technological evolution, the healthcare industry is witnessing greater investment in R&D, automation, and data-driven decision-making, which is helping streamline biophotonic applications across research, diagnostics, and treatment. Additionally, the rise in chronic conditions worldwide is prompting deeper exploration into efficient, accurate, and faster diagnostic methods-another factor contributing to the market's sustained expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $76.1 Billion |

| Forecast Value | $220.1 Billion |

| CAGR | 11.3% |

Based on technology, the market is bifurcated into In-Vitro and In-Vivo platforms. Among these, the In-Vitro segment is registering notable growth and is expected to reach USD 89.6 billion by 2034. This surge is primarily fueled by breakthroughs in lab-based diagnostics, as well as the integration of AI-driven analytics and automation. These advancements are minimizing human error, increasing operational efficiency, and making laboratory workflows more accurate and responsive. As the healthcare sector continues to prioritize early disease detection, the adoption of In-Vitro biophotonic platforms is expanding rapidly.

In terms of application, the market spans various segments, including see-through imaging, microscopy, inside imaging, spectro molecular, analytics sensing, light therapy, surface imaging, and biosensors. The spectro molecular segment held the dominant market share, valued at USD 15.1 billion in 2024. Its leadership in the segment is due to the evolution of spectroscopic tools that now offer enhanced sensitivity and diagnostic precision at the molecular level. These tools play a vital role in identifying biochemical changes linked to disease, thereby enabling early and more personalized intervention strategies.

From an end-use perspective, the market is segmented into tests and components, medical diagnostics, medical therapeutics, and non-medical applications. The tests and components segment accounted for the largest share at 35.4% in 2024, supported by rising demand for advanced diagnostic tools and precision imaging technologies.

Regionally, the United States leads the North American biophotonics market and is expected to achieve a valuation of USD 7.4 billion by 2034, thanks to heavy R&D spending, sophisticated healthcare infrastructure, and increasing demand for advanced diagnostic solutions in response to the growing burden of chronic illnesses.

The industry remains moderately consolidated, with top players like Thermo Fisher Scientific Inc., Carl Zeiss AG, Hamamatsu Photonics K.K., Olympus Corporation, and Oxford Instruments collectively controlling around 55%-60% of the market. These companies continue to invest in high-precision biophotonic technologies and expand their geographic footprint to reinforce their competitive edge.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Emergence of nanotechnology

- 3.2.1.2 Aging population and growing lifestyle diseases

- 3.2.1.3 Increasing use of biophotonics in cell and tissue diagnostics

- 3.2.1.4 Increasing demand for home-based POC devices

- 3.2.1.5 Rising integration with AI & ML

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of technology

- 3.2.2.2 Slow rate of commercialization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 In-Vitro

- 5.3 In-Vivo

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 See-Through imaging

- 6.3 Microscopy

- 6.4 Inside imaging

- 6.5 Spectro molecular

- 6.6 Analytics sensing

- 6.7 Light therapy

- 6.8 Surface imaging

- 6.9 Biosensors

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Tests and components

- 7.3 Medical therapeutics

- 7.4 Medical diagnostics

- 7.5 Non-medical application

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Australia

- 8.4.4 South Korea

- 8.4.5 Japan

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 U.A.E.

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Becton, Dickinson and Company

- 9.2 Carl Zeiss AG

- 9.3 Glenbrook Technologies

- 9.4 Hamamatsu Photonics K.K

- 9.5 IDEX

- 9.6 IPG Photonics Corporation

- 9.7 NU Skin Enterprises

- 9.8 Olympus Corporation

- 9.9 Oxford Instruments PLC

- 9.10 PerkinElmer Inc.

- 9.11 Thermo Fisher Scientific

- 9.12 TOSHIBA CORPORATION

- 9.13 Zecotek Photonics Inc.

- 9.14 Zenalux Biomedical Inc