|

市場調査レポート

商品コード

1721568

動物用ワクチンの市場機会と促進要因、産業動向分析、2025年~2034年予測Animal Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 動物用ワクチンの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月04日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

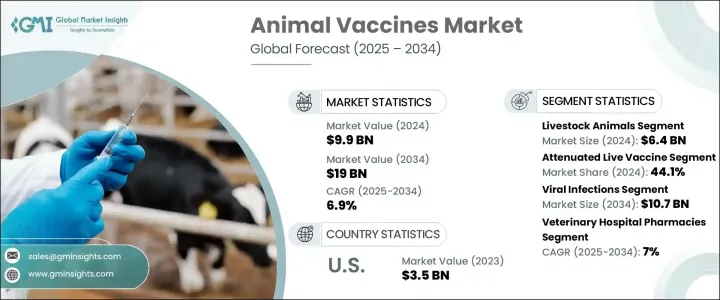

動物用ワクチンの世界市場規模は2024年に99億米ドルとなり、CAGR 6.9%で成長し、2034年には190億米ドルに達すると予測されています。

動物用ワクチンに対する世界の需要は、動物の健康や食品の安全性に対する懸念が高まるにつれて増加傾向にあります。人獣共通感染症を予防し、動物疾病の発生による経済的損失を削減することが重視されるようになり、ワクチン接種プログラムの重要性は倍増しています。世界の動物人口が着実に増加し、ペットの飼育や所有が増加する傾向にあることから、獣医療に対する認識や優先順位が変化しています。ペットの飼い主は、伴侶動物がより長く健康に暮らせるよう、予防接種を含む予防ヘルスケアに投資する傾向が強まっています。同時に、畜産農家は、サプライチェーンを麻痺させ、国際貿易に影響を与えかねない伝染性の高い病気から牛群を守るため、積極的な予防接種戦略を採用しています。世界各国の政府は、動物の健康に関連する規制を強化し、動物の福祉を守り、食品サプライチェーンを確保し、種を超えた疾病伝播のリスクを最小限に抑えるために、強制予防接種プログラムを実施しています。公衆衛生の不可欠な一部としての動物衛生に対するこうした幅広い認識が、市場の成長に大きく寄与しています。

市場セグメンテーションは、家畜とコンパニオンアニマルの2つの主要カテゴリーに大別されます。2024年には、家畜カテゴリーが64億米ドルの評価額で市場を独占しています。家禽、牛、豚、水産養殖などの家畜種は、世界の食料安全保障と農業経済に不可欠です。これらの家畜の疾病発生を予防することは、生産性を維持し経済的損失を最小限に抑えるために極めて重要です。口蹄疫、豚熱、鳥インフルエンザの発生は、この分野では依然として深刻な懸念事項であり、強力なワクチン戦略の必要性を強めています。コンパニオンアニマル・セグメントも、ペット飼育の増加やペットの健康への関心の高まりにより拡大しているが、畜産セグメントが最も高い収益を上げ続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 99億米ドル |

| 予測金額 | 190億米ドル |

| CAGR | 6.9% |

動物用医薬品分野のワクチンには、弱毒生ワクチン、結合型ワクチン、不活化ワクチン、DNAワクチン、組換えワクチンなど、いくつかの種類があります。これらの中で、弱毒生ワクチンは2024年に最も高い市場シェアを占め、全体の44.1%を占めました。これらのワクチンは、強力な免疫応答を産生し、長期的な予防効果を発揮することから広く支持されています。体液性免疫と細胞媒介免疫の両方を刺激する能力があるため、反復投与の必要性が低くなることが多く、家畜と伴侶動物の両方のワクチン接種プログラムで好まれる選択肢となっています。

2024年の動物用ワクチン世界市場の40.6%を北米が占めています。この圧倒的なシェアは、この地域の家畜や家畜の人口が多いことによる。米国はペットの飼育でリードしており、牛、鶏、豚からなる農業部門が確立されています。牛群の健康維持と感染症リスクの最小化に継続的に注力していることが、同地域でのワクチン普及の原動力となっています。

世界の動物用ワクチン市場を形成している主要企業には、Zoetis、Merck Animal Health、Virbac、Boehringer Ingelheim International、Bioveta、Brilliant Bio Pharma、Dechra Pharmaceuticals、Vetoquinol、Neogen Corporation、Elanco Animal Health、Hipra Animal Health Limited、Henry Schein Animal Health(Covetrus, Inc.)などがあります。これらの企業は、広範な研究開発を通じてワクチン・ポートフォリオを積極的に拡大しています。獣医団体や政府機関との戦略的パートナーシップは、ワクチンの入手しやすさの向上に役立っています。さらに、遺伝子工学や組み換えDNAのような先端技術の採用により、進化する疾病の脅威に合わせた、より効果的で長持ちするワクチンの開発が可能になっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 人獣共通感染症の発生率の上昇

- 畜産業の拡大と食料安全保障への懸念

- ペットの飼育と動物の健康への支出の増加

- ワクチン技術の進歩

- 動物の病気の発生増加

- 業界の潜在的リスク&課題

- 高い開発コスト

- 厳格な規制要件

- 促進要因

- 成長可能性分析

- 規制情勢

- 製品パイプライン分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:動物の種類別、2021-2034

- 主要動向

- 家畜

- 家禽

- 牛

- 豚

- 養殖業

- 羊とヤギ

- コンパニオンアニマル

- 犬歯

- ネコ科

- 馬

- 鳥類

第6章 市場推計・予測:ワクチンの種類別、2021-2034

- 主要動向

- 弱毒生ワクチン

- 結合ワクチン

- 不活化ワクチン

- DNAワクチン

- 組み換えワクチン

- その他のワクチンの種類

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 細菌感染症

- ウイルス感染

- 寄生虫感染症

- 真菌感染症

- その他の用途

第8章 市場推計・予測:投与経路別、2021-2034

- 主要動向

- 注射ワクチン

- 経口ワクチン

- 浸漬/スプレーワクチン

第9章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 動物病院薬局

- 小売薬局

- eコマース

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Boehringer Ingelheim International

- Brilliant Bio Pharma

- Bioveta

- Ceva Sante Animale

- Durvet

- Dechra Pharmaceuticals

- Elanco Animal Health

- Henry Schein Animal Health(Covetrus、Inc.)

- Hipra Animal Health Limited

- Indian Immunologicals

- Merck Animal Health

- Neogen Corporation

- Vetoquinol

- Virbac

- Zoetis

The Global Animal Vaccines Market was valued at USD 9.9 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 19 billion by 2034. The global demand for animal vaccines is on the rise as concerns over animal health and food safety gain increasing prominence. With the growing emphasis on preventing zoonotic diseases and reducing economic losses from animal disease outbreaks, the importance of vaccination programs has grown multifold. A steady rise in the global animal population, along with the increasing trend of pet adoption and ownership, is reshaping how veterinary care is perceived and prioritized. Pet owners today are more inclined to invest in preventive healthcare, including vaccinations, to ensure longer and healthier lives for their companion animals. At the same time, livestock farmers are adopting proactive immunization strategies to safeguard their herds against highly contagious diseases that can cripple supply chains and impact international trade. Governments across the globe are tightening regulations related to animal health, implementing compulsory vaccination programs to protect animal welfare, secure the food supply chain, and minimize the risk of cross-species disease transmission. This broader awareness of animal health as an integral part of public health is significantly contributing to market growth.

The animal vaccines market is broadly segmented into two key categories: livestock and companion animals. In 2024, the livestock category dominated the market with a valuation of USD 6.4 billion. Livestock species such as poultry, cattle, swine, and aquaculture are critical to global food security and agricultural economies. Preventing disease outbreaks in these animals is crucial to maintaining productivity and minimizing financial losses. Incidences of foot-and-mouth disease, swine fever, and avian influenza remain serious concerns in this sector, reinforcing the need for robust vaccination strategies. While the companion animal segment is also expanding due to rising pet ownership and increased attention to pet wellness, the livestock segment continues to generate the highest revenue.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $19 Billion |

| CAGR | 6.9% |

Vaccines in the animal health sector include several types, such as attenuated live, conjugate, inactivated, DNA, recombinant, and others. Among these, attenuated live vaccines held the highest market share in 2024, accounting for 44.1% of the total. These vaccines are widely favored for their ability to produce strong immune responses and deliver long-term protection. Their capability to stimulate both humoral and cell-mediated immunity often reduces the need for repeated doses, making them a preferred option in both livestock and companion animal vaccination programs.

North America accounted for 40.6% of the global animal vaccines market in 2024. This dominant share is driven by a large population of domesticated animals and livestock in the region. The United States leads in pet ownership and has a well-established agricultural sector comprising cattle, poultry, and swine. The ongoing focus on maintaining herd health and minimizing infectious disease risks continues to drive vaccine adoption in the region.

Key players shaping the global animal vaccine landscape include Zoetis, Merck Animal Health, Virbac, Boehringer Ingelheim International, Bioveta, Brilliant Bio Pharma, Dechra Pharmaceuticals, Vetoquinol, Neogen Corporation, Elanco Animal Health, Hipra Animal Health Limited, and Henry Schein Animal Health (Covetrus, Inc.). These companies are actively expanding their vaccine portfolios through extensive research and development. Strategic partnerships with veterinary organizations and government agencies are helping improve vaccine accessibility. Additionally, the adoption of advanced technologies like genetic engineering and recombinant DNA is enabling the creation of more effective, long-lasting vaccines tailored to evolving disease threats.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of zoonotic diseases

- 3.2.1.2 Expanding livestock industry and food security concerns

- 3.2.1.3 Increasing pet adoption and expenditure on animal health

- 3.2.1.4 Advancements in vaccine technology

- 3.2.1.5 Increasing outbreaks of animal diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development costs

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Product pipeline analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Livestock animals

- 5.2.1 Poultry

- 5.2.2 Cattle

- 5.2.3 Swine

- 5.2.4 Aquaculture

- 5.2.5 Sheep and goats

- 5.3 Companion animals

- 5.3.1 Canine

- 5.3.2 Feline

- 5.3.3 Equine

- 5.3.4 Avian

Chapter 6 Market Estimates and Forecast, By Vaccine Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Attenuated live vaccine

- 6.3 Conjugate vaccine

- 6.4 Inactivated vaccine

- 6.5 DNA vaccine

- 6.6 Recombinant vaccine

- 6.7 Other vaccine types

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Bacterial infections

- 7.3 Viral infections

- 7.4 Parasitic infections

- 7.5 Fungal infections

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Injection vaccines

- 8.3 Oral vaccines

- 8.4 Immersion/spray vaccines

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 E-commerce

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Boehringer Ingelheim International

- 11.2 Brilliant Bio Pharma

- 11.3 Bioveta

- 11.4 Ceva Sante Animale

- 11.5 Durvet

- 11.6 Dechra Pharmaceuticals

- 11.7 Elanco Animal Health

- 11.8 Henry Schein Animal Health (Covetrus, Inc.)

- 11.9 Hipra Animal Health Limited

- 11.10 Indian Immunologicals

- 11.11 Merck Animal Health

- 11.12 Neogen Corporation

- 11.13 Vetoquinol

- 11.14 Virbac

- 11.15 Zoetis