採掘ポンプの市場機会、成長促進要因、産業動向分析と2025年~2034年予測

Mining Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721554

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

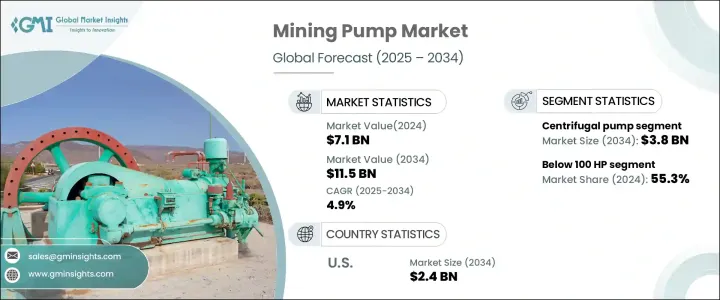

世界の採掘ポンプ市場は、2024年には71億米ドルとなり、CAGR 4.9%で成長し、2034年には115億米ドルに達すると推定されています。

この着実な成長軌道は、近代的な採鉱ニーズをサポートする持続可能で高効率なソリューションへの広範な産業シフトを反映しています。世界中の政府がより環境に優しいインフラを推進し、メーカーが運用コストを最小限に抑えながら生産性を最適化しようとする中、技術的に高度な採掘ポンプへの需要が高まっています。新興国を中心とした工業化の進展に伴い、銅、リチウム、ニッケル、コバルトなどの鉱物や金属に対する世界の需要が急増し続けています。この需要は、拡大する電気自動車(EV)産業、再生可能エネルギー・プロジェクト、インフラ開発イニシアティブによってさらに増幅されています。鉱業はこの勢いに呼応し、安定した原料供給を確保するための活動を活発化させており、採掘ポンプメーカーに大きなビジネスチャンスをもたらしています。採掘プロセスの自動化とデジタル化が進むにつれ、リアルタイムで監視し、ダウンタイムを削減するインテリジェントポンプソリューションの必要性がこれまで以上に高まっています。

採掘ポンプ市場の成長は、主に採掘作業の増加、効率的なウォーターハンドリングシステムの必要性、電池材料の世界の需要の急増によってもたらされています。鉱業会社は、生産性の向上、エネルギー消費の削減、環境規制への対応のため、先進的な機械に多額の投資を行っています。効果的なポンプソリューションは、特に採水、スラリー移動、廃棄物処理作業において、これらの目標を達成する上で極めて重要な役割を果たしています。耐久性があり、高性能でエネルギー効率の高いポンプへのニーズが高まっているため、メーカーは最先端の技術を製品ラインに組み込む必要に迫られています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 71億米ドル |

| 予測金額 | 115億米ドル |

| CAGR | 4.9% |

採掘ポンプ市場は、遠心ポンプ、脱水ポンプ、スラリーポンプ、多段ポンプ、ダイヤフラムポンプなど、ポンプタイプ別に区分されます。遠心ポンプは、2024年に売上高トップのカテゴリーに浮上し、金額で22億米ドルを占める。これらのポンプは、脱水、摩耗性スラリーの移送、長距離の流体移送などの作業に鉱業で広く使用されています。その需要は、汎用性とコスト効率に後押しされています。鉱業では運転コストが上昇しているため、高度な制御システムと優れた油圧設計を備えた省エネ型遠心ポンプが好まれる傾向にあります。

定格出力に関しては、市場には100HP未満、100~500HP、500HP以上のポンプが含まれます。100HP未満のポンプが2024年には55.3%の市場シェアを占めています。これらのポンプは、その手頃な価格、適応性、厳しい現場条件下での運転能力により、小規模事業で一般的に使用されています。水移送、脱水、スラリー管理など、低容量で十分だが安定した性能が不可欠なさまざまな用途に使用されています。

米国の採掘ポンプ市場は2024年に15億米ドルを生み出し、ポンプ技術の進歩、採掘活動の拡大、鉱物需要の増加がその原動力となっています。同国の鉱業部門は、建設、自動車、エレクトロニクスなどの産業に原材料を供給し、経済の重要な構成要素であり続けています。重要な鉱物の需要が国内および世界で増加する中、米国の採掘事業は成長を続け、現代の持続可能性と効率性の目標に沿った高性能ポンプの必要性を押し上げています。

世界の採掘ポンプ市場の主要企業には、Sulzer、The Weir Group、Xylem、KSB、Schurco Slurry、Multotec Group、荏原製作所、The Gorman-Rupp Company、Flowserve Corporation、Grundfos Holding、鶴見製作所、NETZSCH Pumpen &Systeme、JEE Pumps、Metso Outotec Corporationなどがあります。これらの企業は、競争力を強化するために技術革新を活用し、エネルギー効率の高いポンプに注力し、予知保全とリアルタイム性能追跡をサポートするIoT対応技術を統合しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- 小売業者

- 影響要因

- 促進要因

- 鉱物と金属に対する世界の需要の増加

- 技術的進歩

- 廃水管理への傾向

- 採掘事業の拡大

- 業界の潜在的リスク&課題

- 頻繁なメンテナンスと交換

- 変動する価格

- 促進要因

- テクノロジーとイノベーションの情勢

- 消費者購買行動分析

- 人口動向

- 購入決定に影響を与える要因

- 消費者製品の採用

- 優先流通チャネル

- 成長可能性分析

- 規制情勢

- 価格分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:ポンプタイプ別、2021-2034

- 主要動向

- 遠心ポンプ

- 排水ポンプ

- スラリーポンプ

- 多段ポンプ

- ダイヤフラムポンプ

- その他(ピストンポンプ、ペリスタルティックポンプなど)

第6章 市場推計・予測:電源別、2021-2034

- 主要動向

- 電動・ソーラーポンプ

- ディーゼルポンプ

- その他(ガソリン・太陽光など)

第7章 市場推計・予測:流量別、2021-2034

- 主要動向

- 100 m³/h以下

- 100~500 m³/h

- 500 m³/h以上

第8章 市場推計・予測:馬力別、2021-2034

- 主要動向

- 100HP以下

- 100~500馬力

- 500HP以上

第9章 市場推計・予測:技術別、2021-2034

- 主要動向

- 従来型

- スマート

第10章 市場推計・予測:用途別、2021-2034

- 主要動向

- 鉱山排水

- 鉱物処理

- 水・廃水処理

- 粉塵抑制

- その他(潤滑等)

第11章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接

- 間接的

第12章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第13章 企業プロファイル

- Ebara Corporation

- Flowserve Corporation

- Grundfos Holding

- Gorman-Rupp

- JEE Pumps

- KSB

- Metso Outotec Corporation

- Multotec Group

- NETZSCH Pumps &Systems

- Schurco Slurry

- Sulzer

- The Gorman-Rupp Company

- The Weir Group

- Tsurumi Manufacturing

- Xylem

目次

The Global Mining Pump Market was valued at USD 7.1 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 11.5 billion by 2034. This steady growth trajectory reflects a broader industry shift toward sustainable and high-efficiency solutions that support modern mining needs. As governments across the globe push for greener infrastructure and manufacturers seek to optimize productivity while minimizing operational costs, the demand for technologically advanced mining pumps is rising. With growing industrialization, particularly in emerging economies, the global appetite for minerals and metals such as copper, lithium, nickel, and cobalt continues to surge. This demand is further amplified by the expanding electric vehicle (EV) industry, renewable energy projects, and infrastructure development initiatives. The mining industry, responding to this momentum, is ramping up activities to ensure consistent raw material supply, which in turn is creating substantial opportunities for mining pump manufacturers. As mining processes become increasingly automated and digitized, the need for intelligent pumping solutions that offer real-time monitoring and reduced downtime is more critical than ever.

The growth of the mining pump market is primarily driven by increasing mining operations, the need for efficient water handling systems, and the surging global demand for battery materials. Mining companies are investing heavily in advanced machinery to improve productivity, reduce energy consumption, and meet environmental regulations. Effective pumping solutions play a pivotal role in achieving these goals, especially in water extraction, slurry movement, and waste handling operations. The rising need for durable, high-performance, and energy-efficient pumps is compelling manufacturers to integrate cutting-edge technologies into their product lines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.1 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 4.9% |

The mining pump market is segmented by pump type, including centrifugal, dewatering, slurry, multi-stage, and diaphragm pumps. Centrifugal pumps emerged as the top revenue-generating category in 2024, accounting for USD 2.2 billion in value. These pumps are widely used in mining for tasks such as dewatering, transporting abrasive slurries, and transferring fluids over long distances. Their demand is fueled by their versatility and cost-efficiency. With operational costs rising in the mining industry, there is a clear preference for energy-saving centrifugal pumps equipped with advanced control systems and better hydraulic designs.

In terms of power rating, the market includes pumps below 100 HP, between 100-500 HP, and above 500 HP. Pumps below 100 HP dominated the landscape in 2024, holding a 55.3% market share. These pumps are commonly used in small-scale operations due to their affordability, adaptability, and ability to operate under challenging site conditions. They serve various applications such as water transfer, dewatering, and slurry management where lower capacity is sufficient but consistent performance is essential.

The U.S. mining pump market generated USD 1.5 billion in 2024, driven by advancements in pump technologies, expanded mining activities, and rising mineral demand. The country's mining sector remains a crucial component of its economy, supplying raw materials to industries such as construction, automotive, and electronics. As demand for critical minerals increases domestically and globally, U.S. mining operations continue to grow, pushing the need for high-performance pumps that align with modern sustainability and efficiency goals.

Key players in the global mining pump market include Sulzer, The Weir Group, Xylem, KSB, Schurco Slurry, Multotec Group, Ebara Corporation, The Gorman-Rupp Company, Flowserve Corporation, Grundfos Holding, Tsurumi Manufacturing, NETZSCH Pumpen & Systeme, JEE Pumps, and Metso Outotec Corporation. These companies are leveraging innovation to strengthen their competitive edge, focusing on energy-efficient pumps and integrating IoT-enabled technologies that support predictive maintenance and real-time performance tracking.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased global demand for minerals and metals

- 3.2.1.2 Technological advancements

- 3.2.1.3 Inclination towards wastewater management

- 3.2.1.4 Expanded mining operations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Frequent maintenance and replacement

- 3.2.2.2 Fluctuating prices

- 3.2.1 Growth drivers

- 3.3 Technology & innovation landscape

- 3.4 Consumer buying behavior analysis

- 3.4.1 Demographic trends

- 3.4.2 Factors affecting buying decision

- 3.4.3 Consumer product adoption

- 3.4.4 Preferred distribution channel

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Pump Type, 2021 - 2034, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Centrifugal pump

- 5.3 Dewatering pump

- 5.4 Slurry pump

- 5.5 Multi-Stage pump

- 5.6 Diaphragm pump

- 5.7 Others (Piston Pumps, Peristaltic Pumps, etc.)

Chapter 6 Market Estimates & Forecast, By Power Source, 2021 - 2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Electric & Solar Pumps

- 6.3 Diesel pump

- 6.4 Others (Gasoline Solar, etc.)

Chapter 7 Market Estimates & Forecast, By Flow Rate, 2021 - 2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Below 100 m³/h

- 7.3 100 - 500 m³/h

- 7.4 Above 500 m³/h

Chapter 8 Market Estimates & Forecast, By Horsepower, 2021 - 2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Below 100 HP

- 8.3 100 - 500 HP

- 8.4 Above 500 HP

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Conventional

- 9.3 Smart

Chapter 10 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Mine dewatering

- 10.3 Mineral processing

- 10.4 Water & Wastewater Treatment

- 10.5 Dust suppression

- 10.6 Others (Lubrication, etc.)

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 Saudi Arabia

- 12.6.2 UAE

- 12.6.3 South Africa

Chapter 13 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 13.1 Ebara Corporation

- 13.2 Flowserve Corporation

- 13.3 Grundfos Holding

- 13.4 Gorman-Rupp

- 13.5 JEE Pumps

- 13.6 KSB

- 13.7 Metso Outotec Corporation

- 13.8 Multotec Group

- 13.9 NETZSCH Pumps & Systems

- 13.10 Schurco Slurry

- 13.11 Sulzer

- 13.12 The Gorman-Rupp Company

- 13.13 The Weir Group

- 13.14 Tsurumi Manufacturing

- 13.15 Xylem

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日