|

市場調査レポート

商品コード

1721529

CTスキャナーの市場機会、成長促進要因、産業動向分析、2025~2034年予測CT Scanner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| CTスキャナーの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月03日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

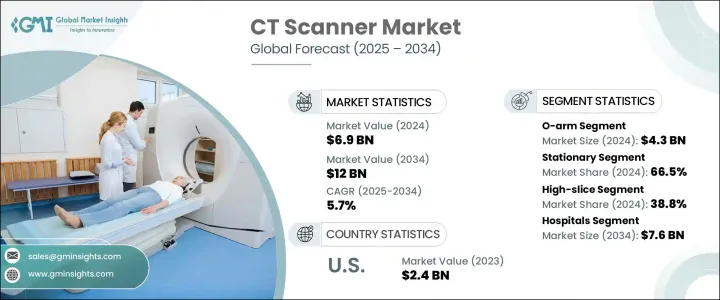

世界のCTスキャナー市場は、2024年には69億米ドルとなり、CAGR 5.7%で成長し、2034年には120億米ドルに達すると予測されています。

ヘルスケアプロバイダーが疾病の早期発見、精密医療、治療成績の向上を優先する中、高度画像診断ソリューションの需要は増加の一途をたどっています。コンピュータ断層撮影(CT)スキャナは、人体の高解像度断面画像を提供することで、これらの目標を達成する上で極めて重要な役割を果たしています。日常的なスクリーニングから緊急診断まで、CTスキャナーは現代の医療画像診断の要となっています。複雑な内部構造を可視化し、がん、心血管疾患、内蔵損傷、神経疾患などの正確な診断を可能にするため、ヘルスケア機関はますますこのシステムに頼るようになっています。政府や民間ヘルスケア・プロバイダーがインフラを拡大し、デジタル・ヘルス技術を採用するにつれて、CTスキャナー市場は一貫した成長を遂げると予想されます。この勢いは、スキャン時間の短縮、放射線被曝の低減、AIや機械学習アルゴリズムを使用した画像の鮮明度の向上を目指す継続的なイノベーションによってさらに支えられています。ヘルスケア産業が低侵襲処置と患者中心のケアに傾く中、CT画像の採用は著しいペースで成長を続けています。

市場はアーキテクチャ別にOアームシステムとCアームシステムに区分され、Oアームセグメントは2024年に43億米ドルを生み出します。このセグメントは2025年から2034年にかけてCAGR 5.6%で成長すると予測されています。Oアームシステムは、手術室で直接リアルタイムの2Dおよび3Dイメージング機能を提供することで、外科イメージングを変革しています。コンパクトで移動可能な設計により、手術ワークフローへのシームレスな統合が可能になり、患者を専用の画像処理室に搬送する必要性を最小限に抑えることができます。外科医は、手技中の可視性と精度が向上することで合併症のリスクを低減し、手術結果の改善につながります。術中画像診断と精密誘導手術に対する需要の高まりは、予測期間にわたってこの分野の持続的成長を促進すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 69億米ドル |

| 予測金額 | 120億米ドル |

| CAGR | 5.7% |

タイプ別では、市場はポータブルCTスキャナーと据置型CTスキャナーに分けられます。据置型は2024年に46億米ドル、市場シェア66.5%を占める。これらのシステムは、優れた画像解像度、高速スキャン、大量のヘルスケア環境における堅牢な性能で知られています。反復再構成、AI搭載診断ツール、マルチスライススキャン機能などの最近の進歩により、据置型CTシステムの診断価値が高まっています。幅広い医療用途で一貫した高品質のイメージングを求める病院や診断センターにとって、CTシステムは依然として好ましい選択肢です。

北米CTスキャナー市場は、2024年に27億米ドルと評価され、2034年には46億米ドルに達すると予測されています。この地域の市場拡大の原動力は、慢性疾患の罹患率の上昇と、診断インフラおよび研究開発への旺盛な投資です。特に米国は、高いヘルスケア支出と大手医療機器メーカーの存在感を背景に、先進的な画像ソリューションを通じてイノベーションをリードし続けています。

世界のCTスキャナー業界の著名企業には、富士フイルムホールディングス、アキュレイ、メドトロニック、島津製作所、Xoran Technologies、Koning Health、キヤノン、GE HealthCare Technologies、PLANMED、CurveBeam AI、サムスン電子、シーメンス・ヘルティニアーズ、Neusoft Medical Systems、Koninklijke Philips、Shenzhen Anke High-techなどがあります。これらの企業は、AIによる機能強化、反復的イメージング技術、戦略的提携に多額の投資を行い、診断能力の向上と世界の事業拡大を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界中で慢性疾患の有病率が増加

- 低侵襲診断法への関心の高まり

- CTスキャナーが他の画像診断法に対して提供する利点

- CTスキャナーにおける技術の進歩

- 業界の潜在的リスク&課題

- 設置とメンテナンスに多大なコストがかかる

- CTスキャンに伴うリスク

- 促進要因

- 成長可能性分析

- テクノロジーの情勢

- 規制情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:アーキテクチャ別、2021 –2034

- 主要動向

- Oアーム

- Cアーム

第6章 市場推計・予測:タイプ別、2021 –2034

- 主要動向

- ポータブル

- 据置型

第7章 市場推計・予測:技術別、2021 –2034

- 主要動向

- ハイスライス

- ミッドスライス

- ロースライス

- コーンビーム

第8章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 人間

- 診断

- 神経学

- 腫瘍学

- 心臓病学

- その他

- 術中

- 診断

- 調査

- 獣医

第9章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 病院

- CRO

- 外来手術センター

第10章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- ポーランド

- オーストリア

- スイス

- スロバキア

- チェコ共和国

- ノルウェー

- フィンランド

- スウェーデン

- デンマーク

- ベネルクス

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 台湾

- インドネシア

- ベトナム

- カンボジア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Accuray

- Canon

- CurveBeam AI

- FUJIFILM Holdings Corporation

- GE HealthCare Technologies

- Koning Health

- Koninklijke Philips

- Medtronic

- Neusoft Medical Systems

- PLANMED

- Samsung Electronics

- Shenzhen Anke High-tech

- Shimadzu Corporation

- Siemens Healthineers

- Xoran Technologies

The Global CT Scanner Market was valued at USD 6.9 billion in 2024 and is expected to grow at a CAGR of 5.7% to reach USD 12 billion by 2034. The demand for advanced diagnostic imaging solutions continues to rise as healthcare providers prioritize early disease detection, precision medicine, and improved treatment outcomes. Computed Tomography (CT) scanners play a pivotal role in meeting these goals by delivering high-resolution, cross-sectional images of the human body. From routine screenings to emergency diagnostics, CT scanners have become a cornerstone of modern medical imaging. Healthcare institutions are increasingly relying on these systems to visualize complex internal structures, enabling accurate diagnoses for conditions such as cancer, cardiovascular diseases, internal injuries, and neurological disorders. As governments and private healthcare providers expand infrastructure and adopt digital health technologies, the CT scanner market is expected to witness consistent growth. This momentum is further supported by ongoing innovations that aim to reduce scanning times, lower radiation exposure, and enhance image clarity using AI and machine learning algorithms. With the healthcare industry leaning toward minimally invasive procedures and patient-centric care, the adoption of CT imaging continues to grow at a significant pace.

The market is segmented by architecture into O-arm and C-arm systems, with the O-arm segment generating USD 4.3 billion in 2024. This segment is projected to grow at a CAGR of 5.6% between 2025 and 2034. O-arm systems are transforming the surgical imaging landscape by offering real-time 2D and 3D imaging capabilities directly in operating rooms. Their compact and mobile design enables seamless integration into surgical workflows, minimizing the need to transport patients to dedicated imaging suites. Surgeons benefit from enhanced visibility and accuracy during procedures, which reduces the risk of complications and leads to better surgical outcomes. The growing demand for intraoperative imaging and precision-guided surgeries is expected to drive sustained growth in this segment over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $12 Billion |

| CAGR | 5.7% |

In terms of type, the market is divided into portable and stationary CT scanners. The stationary segment dominated in 2024, generating USD 4.6 billion and accounting for a 66.5% market share. These systems are known for their superior image resolution, high-speed scanning, and robust performance in high-volume healthcare settings. Recent advancements such as iterative reconstruction, AI-powered diagnostic tools, and multi-slice scanning capabilities have elevated the diagnostic value of stationary CT systems. They remain the preferred choice for hospitals and diagnostic centers seeking consistent, high-quality imaging across a wide range of medical applications.

The North America CT Scanner Market was valued at USD 2.7 billion in 2024 and is forecasted to reach USD 4.6 billion by 2034. The region's market expansion is driven by the rising incidence of chronic diseases, along with strong investments in diagnostic infrastructure and R&D. The U.S., in particular, continues to lead innovation through advanced imaging solutions fueled by high healthcare expenditure and a strong presence of leading medical device manufacturers.

Some of the prominent players in the global CT scanner industry include FUJIFILM Holdings Corporation, Accuray, Medtronic, Shimadzu Corporation, Xoran Technologies, Koning Health, Canon, GE HealthCare Technologies, PLANMED, CurveBeam AI, Samsung Electronics, Siemens Healthineers, Neusoft Medical Systems, Koninklijke Philips, and Shenzhen Anke High-tech. These companies are heavily investing in AI-driven enhancements, iterative imaging technologies, and strategic collaborations to elevate diagnostic capabilities and expand their global footprint.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases worldwide

- 3.2.1.2 Rising preference for minimally invasive diagnostic procedures

- 3.2.1.3 Advantages offered by CT scanner over other imaging modalities

- 3.2.1.4 Technological advancements in CT scanner

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Significant installation and maintenance cost

- 3.2.2.2 Risks associated with CT scan

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Architecture, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 O-arm

- 5.3 C-arm

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Portable

- 6.3 Stationary

Chapter 7 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 High-slice

- 7.3 Mid-slice

- 7.4 Low-slice

- 7.5 Cone beam

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Human

- 8.2.1 Diagnostic

- 8.2.1.1 Neurology

- 8.2.1.2 Oncology

- 8.2.1.3 Cardiology

- 8.2.1.4 Others

- 8.2.2 Intraoperative

- 8.2.1 Diagnostic

- 8.3 Research

- 8.4 Veterinary

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 CROs

- 9.4 Ambulatory surgical centers

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Poland

- 10.3.8 Austria

- 10.3.9 Switzerland

- 10.3.10 Slovakia

- 10.3.11 Czech Republic

- 10.3.12 Norway

- 10.3.13 Finland

- 10.3.14 Sweden

- 10.3.15 Denmark

- 10.3.16 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Taiwan

- 10.4.7 Indonesia

- 10.4.8 Vietnam

- 10.4.9 Cambodia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Accuray

- 11.2 Canon

- 11.3 CurveBeam AI

- 11.4 FUJIFILM Holdings Corporation

- 11.5 GE HealthCare Technologies

- 11.6 Koning Health

- 11.7 Koninklijke Philips

- 11.8 Medtronic

- 11.9 Neusoft Medical Systems

- 11.10 PLANMED

- 11.11 Samsung Electronics

- 11.12 Shenzhen Anke High-tech

- 11.13 Shimadzu Corporation

- 11.14 Siemens Healthineers

- 11.15 Xoran Technologies