エタノール・バイオ燃料の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Ethanol Biofuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 127 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721511

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

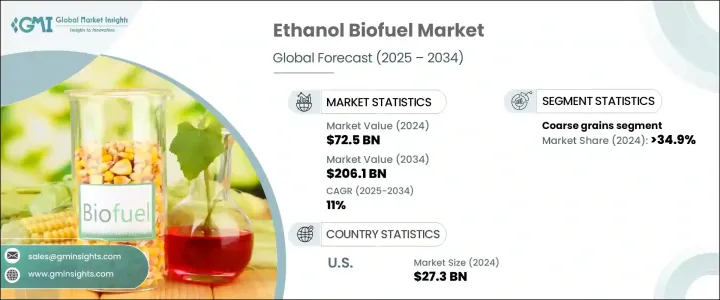

エタノール・バイオ燃料の世界市場規模は2024年に725億米ドルとなり、CAGR 11%で成長し、2034年には2,061億米ドルに達すると予測されています。

エタノール・バイオ燃料は、各国が化石燃料に代わる持続可能な代替燃料を探す中で、世界的に支持され続けています。二酸化炭素排出量の削減、再生可能エネルギー目標の達成、低炭素経済への移行が急務となり、バイオ燃料インフラへの投資が世界的に活発化しています。主に粗粒穀物や砂糖作物などの再生可能バイオマスを原料とするエタノールは、輸送部門に信頼性が高く、環境に配慮したソリューションを提供します。政府による規制の強化、石油価格の上昇、気候変動に対する消費者の意識の高まりに伴い、エタノール・バイオ燃料は、性能と持続可能性のバランスがとれた戦略的エネルギー資源として浮上しています。既存の自動車エンジンやインフラとの適合性に加え、E10やE85のようなクリーンな混合燃料に対する需要の高まりが、市場の魅力をさらに高めています。さらに、酵素技術と発酵プロセスの進歩により生産コストが削減され、変換効率が向上しているため、各地域でエタノール・バイオ燃料の商業的実現可能性が高まっています。

エタノール・バイオ燃料エタノールは、ガソリンに代わる、よりクリーンで持続可能な代替燃料として、特に輸送分野で広く認知されつつあります。エタノールはガソリンと混合することで、一酸化炭素や粒子状物質などの有害な排出ガスを低減し、オクタン価を高めることができます。こうした利点から、E10(エタノール10%)やE85(エタノール85%)のようなエタノール混合燃料は、消費者と政府の双方にとって魅力的な選択肢となっています。エタノールは既存の燃料システムに柔軟に組み込むことができるため、排出量削減目標に対する短期的・中期的な現実的ソリューションとして位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 725億米ドル |

| 予測金額 | 2,061億米ドル |

| CAGR | 11% |

航空業界では、エタノールを原料とする持続可能な航空燃料(SAF)への移行が進んでいます。エタノールを原料とするSAFは、従来のジェット燃料と比較してライフサイクル排出量を最大80%削減できる可能性が実証されており、航空輸送の脱炭素化のための実行可能かつ拡張可能な道筋となっています。この用途の拡大は、世界の燃料市場におけるエタノールの地位をさらに強固なものにしています。

同市場は、粗粒穀物、砂糖作物、植物油など、原料の種類によって分類されます。2024年には、粗粒穀物セグメントがエタノール・バイオ燃料市場で34.9%のシェアを占める。デンプン含有量が多い粗粒穀物は、発酵可能な糖に容易に変換されるため、バイオ燃料生産に特に効率的です。混合義務や農業生産者への補助金など、政府による支援政策が、エタノール生産における粗粒穀物の使用を大きく後押ししています。

米国のエタノール・バイオ燃料市場は、2024年に273億米ドルと評価されました。再生可能燃料基準(RFS)は年間150億ガロンのエタノール混合を義務付けており、安定した需要と継続的な成長を保証しています。エタノールは、持続可能性とエネルギー安全保障を推進する国の戦略において、依然として重要な役割を担っています。

主要市場参入企業には、ADM、BP、カーギル、シェブロン、コーデックス、デュポン、グリーン・プレインズ、ロイヤル・ダッチ・シェル、バレロ・エナジー、リオンデルバセル・インダストリーズなどがあります。これらの企業は、生産能力の拡大、先進バイオ燃料技術への投資、長期原料契約の締結に注力しています。また、世界の持続可能性目標に沿った再生可能燃料を供給する一方で、二酸化炭素排出量を最小限に抑える取り組みも行っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:原料別、2021-2034

- 主要動向

- 粗粒

- 砂糖作物

- 植物油

- その他

第6章 市場規模・予測:用途別、2021-2034

- 主要動向

- 交通機関

- 航空

- その他

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- スペイン

- 英国

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ADM

- Borregaard

- Blue Biofuel

- BTG Bioliquids

- Cargill

- Chevron

- Clariant

- COFCO

- CropEnergies

- Munzer Bioindustrie

- Neste

- POET LLC

- Praj Industries

- Raizen

- The Andersons

- TotalEnergies

- UPM

- Valero

- Verbio

- Wilmar International

- Zilor

目次

The Global Ethanol Biofuel Market was valued at USD 72.5 billion in 2024 and is estimated to grow at a CAGR of 11% to reach USD 206.1 billion by 2034. Ethanol biofuel continues to gain traction worldwide as countries look for sustainable alternatives to fossil fuels. The growing urgency to reduce carbon emissions, meet renewable energy targets, and transition toward low-carbon economies has intensified global investments in biofuel infrastructure. Ethanol, derived primarily from renewable biomass like coarse grains and sugar crops, offers a reliable and environmentally responsible solution for the transportation sector. With increasing government mandates, rising oil prices, and heightened consumer awareness about climate change, ethanol biofuel emerges as a strategic energy resource that balances performance with sustainability. Its compatibility with existing vehicle engines and infrastructure, combined with rising demand for cleaner fuel blends like E10 and E85, is further fueling its market appeal. Additionally, advances in enzyme technology and fermentation processes are reducing production costs and improving conversion efficiencies, boosting the commercial viability of ethanol biofuels across regions.

Ethanol biofuel is being widely recognized as a cleaner and more sustainable alternative to gasoline, especially in transportation. When blended with gasoline, ethanol helps lower harmful emissions, such as carbon monoxide and particulate matter, while also increasing octane levels. These benefits make ethanol blends like E10 (10% ethanol) and E85 (85% ethanol) attractive choices for both consumers and governments, aiming to reduce environmental impact without compromising vehicle performance. The flexibility of ethanol to be integrated into existing fuel systems positions it as a practical short- and mid-term solution to emissions reduction goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $72.5 Billion |

| Forecast Value | $206.1 Billion |

| CAGR | 11% |

The aviation industry is increasingly shifting toward sustainable aviation fuel (SAF) produced from ethanol, which supports net-zero carbon initiatives. Ethanol-based SAF has demonstrated the potential to cut lifecycle emissions by up to 80% compared to conventional jet fuel, making it a viable and scalable path for decarbonizing air travel. This growing application further strengthens ethanol's position in the global fuel market.

The market is categorized based on feedstock types, including coarse grains, sugar crops, and vegetable oils. In 2024, the coarse grains segment accounted for a 34.9% share of the ethanol biofuel market. High starch content makes coarse grains particularly efficient for biofuel production, as they are easily converted into fermentable sugars. Supportive government policies, including blending mandates and subsidies for agricultural producers, have significantly encouraged the use of coarse grains in ethanol production.

The U.S. Ethanol Biofuel Market was valued at USD 27.3 billion in 2024. The Renewable Fuel Standard (RFS) mandates the blending of 15 billion gallons of ethanol annually, ensuring steady demand and continued growth. Ethanol remains a key player in the country's strategy to advance sustainability and energy security.

Leading market participants include ADM, BP, Cargill, Chevron, Codexis, DuPont, Green Plains, Royal Dutch Shell, Valero Energy, and LyondellBasell Industries. These companies are focusing on expanding production capacity, investing in advanced biofuel technologies, and entering long-term feedstock agreements. Many are also working to minimize their carbon footprints while delivering renewable fuels that align with global sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Feedstock, 2021 - 2034 (MToe, USD Billion)

- 5.1 Key trends

- 5.2 Coarse grain

- 5.3 Sugar crop

- 5.4 Vegetable oil

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (MToe, USD Billion)

- 6.1 Key trends

- 6.2 Transportation

- 6.3 Aviation

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (MToe, USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Spain

- 7.3.4 UK

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ADM

- 8.2 Borregaard

- 8.3 Blue Biofuel

- 8.4 BTG Bioliquids

- 8.5 Cargill

- 8.6 Chevron

- 8.7 Clariant

- 8.8 COFCO

- 8.9 CropEnergies

- 8.10 Munzer Bioindustrie

- 8.11 Neste

- 8.12 POET LLC

- 8.13 Praj Industries

- 8.14 Raizen

- 8.15 The Andersons

- 8.16 TotalEnergies

- 8.17 UPM

- 8.18 Valero

- 8.19 Verbio

- 8.20 Wilmar International

- 8.21 Zilor

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 127 Pages

- 納期

- 2~3営業日