エアダクトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Air Ducts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721504

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

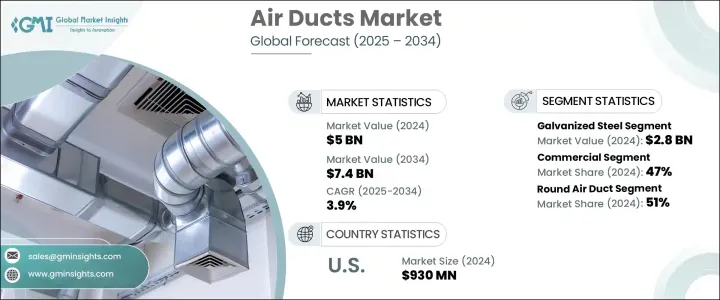

エアダクトの世界市場は、2024年に50億米ドルとなり、CAGR3.9%で成長し、2034年までには74億米ドルに達すると推定されています。

この成長の主な原動力は、世界の都市化の急速なペースと、エネルギー効率に関する厳しい規制の導入の高まりです。世界の都市が拡大を続ける中、住宅、商業、工業用インフラのニーズが急増し、高度なHVACシステムの需要に直接影響を与えています。これらのシステムは、最適な室内温度と空気の質を維持するためにエアダクトに大きく依存しています。開発途上地域でも先進地域でも建設活動が活発化しているため、最新のHVACシステムが設置されるようになり、その結果、効率的で持続可能でメンテナンスが容易なエアダクトの需要が高まっています。

HVACシステムは現在、主に熱的快適性とエネルギー効率を確保するために、新しい建物の中核的な機能となっています。環境に配慮した建築が重視されるようになったことで、エアダクト業界に新たなビジネスチャンスが生まれ、特に環境に優しい材料を使った製品に注目が集まっています。極端な気候の地域では、特に冷房と換気システムが不可欠であり、耐久性が高く効率的なエアダクトシステムの使用が明らかに増加しています。オフィス、小売店、交通機関、複合施設など、人の出入りが多い場所では、室内空気の質を維持することが重要です。これらのエリアでは24時間空気循環が必要とされるため、機能的でありながらアーキテクチャと見た目に調和した高性能ダクトの必要性が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 50億米ドル |

| 予測金額 | 74億米ドル |

| CAGR | 3.9% |

2024年には、亜鉛メッキ鋼板エアダクトが市場で最大のシェアを占め、28億米ドル以上の収益を上げました。この材料は、その優れた耐久性と経年劣化に対する耐性により、請負業者や建設業者の間で依然として好ましい選択肢となっています。亜鉛メッキ鋼製ダクトは、手入れが最小限で済み、性能が長持ちするため、長期にわたって費用対効果が高いです。ポリマーベースのエアダクトも牽引力を増しており、2025年から2034年までのCAGRは約3.6%と予想されています。これらのダクトは、主にPVCやポリエチレンなどのコスト効率と耐久性に優れたプラスチックで作られています。軽量で耐食性に優れ、設置が容易なため、予算とスケジュールが厳しいプロジェクトに信頼性の高いソリューションを提供します。また、滑らかな内面は空気抵抗を最小限に抑え、気流の改善とHVAC全体の性能向上につながります。

2024年のエアダクト市場は、商業部門が世界の売上シェアの約47%を占め、圧倒的な強さを見せました。商業施設、特に都心部では、エネルギー効率と空気品質の遵守をサポートするHVACシステムが優先されています。こうした空間では美観も重要な役割を果たし、モダンなインテリアデザインとシームレスに融合するエアダクトの需要を押し上げています。商業施設で使用されるダクトは、さまざまなレイアウトや構造構成に対応しながら、最適なエアフローを提供する必要があります。

形状別では、丸型のエアダクトが2024年の市場全体の51%以上を占め、首位に立ちました。空気力学に基づいた設計により、騒音が少なく圧力損失が最小で効率的な気流が確保されるため、住宅用、商業用ともに理想的な形状となっています。また、丸型ダクトは清掃やメンテナンスが容易で、長期的な信頼性と設置の柔軟性に優れています。一般的に亜鉛メッキ鋼などの金属で製造される長方形ダクトは、構造的に堅牢で、標準化された建築設計に適合するため、大規模な商業・工業プロジェクトに好まれます。これらのダクトはしばしば天井や壁システムに組み込まれ、よりコンパクトな設置面積を提供します。丸型と角型の両方の特徴を併せ持つ楕円ダクトの人気も高まっています。強力な送風効率を維持しながらスマートな外観を実現し、性能とデザインが両立する近代的な建物に理想的です。

2024年のエアダクト世界市場では、北米が大きなシェアを占めており、米国だけで約9億3,000万米ドルの売上高を計上し、地域別シェアの80%近くを占めています。米国全域で建設とインフラ開発が堅調に伸びているため、先進的なHVAC設備、特に長期的な持続可能性目標をサポートするシステムの需要が高まっています。建設業者はグリーンビルディングの規制や認証に準拠するため、環境に配慮した材料で作られたダクトを積極的に採用しています。さらに、スマートHVACシステムの採用が増加しているため、接続技術をサポートする互換性のあるエアダクトのニーズが高まっています。その結果、空気品質、エネルギー効率、温度制御を強化するために、古い建物を新世代のダクトで改修する方向にシフトしています。

業界の主要企業は、市場でのプレゼンスを拡大し、進化する顧客ニーズに対応するため、技術のアップグレード、施設の拡張、戦略的パートナーシップに投資しています。こうした動きは、世界市場において変化する建築基準法、エネルギー規範、設計上の期待に沿う高性能ダクトソリューションを提供することを可能にしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 成長促進要因

- 都市化とインフラ開発

- エネルギー効率規制

- 気候変動

- 業界の潜在的リスク・課題

- 高い設置・保守コストめ

- 既存構造物の改修の複雑さ

- 成長促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 亜鉛メッキ鋼

- アルミニウム

- グラスファイバー

- ポリマー

- その他

第6章 市場推計・予測:形状別、2021年~2034年

- 主要動向

- 長方形

- 丸型

- 楕円形

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- 産業用

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第9章 企業プロファイル

- DC Duct &Sheet Metal

- Deflecto

- DUNDAS JAFINE

- Eastern Sheet Metal

- Lindab Group

- Lennox International

- M&M Manufacturing

- Novaflex Group

- Nuaire

- Rubber World Industries

- Ruskin Titus India

- Saint-Gobain

- Sisneros Bros

- Thermaflex

- Tin Man Sheet Metal

- Turnkey Duct Systems

- Zinger Sheet Metal

目次

The Global Air Ducts Market was valued at USD 5 billion in 2024 and is estimated to grow a CAGR of 3.9% to reach USD 7.4 billion by 2034. This growth is largely driven by the rapid pace of urbanization worldwide and the rising adoption of stringent energy efficiency regulations. As global cities continue to expand, the need for residential, commercial, and industrial infrastructure has surged, directly impacting demand for advanced HVAC systems. These systems rely heavily on air ducts to maintain optimal indoor temperatures and air quality. The growing construction activity across developing and developed regions alike is boosting the installation of modern HVAC systems, consequently fueling the demand for air ducts that are efficient, sustainable, and easy to maintain.

HVAC systems are now a core feature in new buildings, primarily to ensure thermal comfort and energy efficiency. The growing emphasis on green construction practices is creating fresh opportunities in the air ducts industry, with a particular focus on products made from eco-friendly materials. In regions with extreme climates, especially where cooling and ventilation systems are indispensable, there is an evident rise in the use of durable and efficient air duct systems. Commercial buildings are leading adopters of these systems, as air ducts are critical to maintaining indoor air quality in high-traffic zones such as offices, retail stores, transit stations, and multi-use complexes. These areas require round-the-clock air circulation, increasing the necessity for high-performance ducts that are both functional and visually compatible with the architecture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 3.9% |

In 2024, galvanized steel air ducts held the largest share of the market, generating revenue of over USD 2.8 billion. This material remains a preferred choice among contractors and builders due to its exceptional durability and resistance to wear over time. Galvanized steel ducts require minimal upkeep and offer prolonged performance, making them cost-effective over the long term. Polymer-based air ducts are also gaining traction and are expected to register a CAGR of around 3.6% from 2025 to 2034. These ducts are primarily made from cost-efficient and durable plastics such as PVC and polyethylene. They are lightweight, corrosion-resistant, and easy to install, providing a reliable solution for projects with tight budgets and strict timelines. Their smooth inner surfaces also minimize air resistance, leading to improved airflow and better overall HVAC performance.

The commercial sector dominated the air ducts market in 2024, accounting for about 47% of the global revenue share. Commercial facilities, especially those in urban centers, are prioritizing HVAC systems that support energy efficiency and air quality compliance. In these spaces, aesthetics also play a key role, pushing demand for air ducts that seamlessly integrate with modern interior designs. Ducts used in commercial setups must provide optimal airflow while being adaptable to various layouts and structural configurations.

By shape, round air ducts took the lead in 2024, capturing over 51% of the total market. Their aerodynamic design ensures efficient airflow with reduced noise and minimal pressure drop, making them ideal for both residential and commercial applications. Round ducts are also easier to clean and maintain, offering better long-term reliability and installation flexibility. Rectangular ducts, typically manufactured from metals like galvanized steel, are favored for large-scale commercial and industrial projects due to their structural robustness and compatibility with standardized building designs. These ducts are often integrated into ceilings or wall systems, offering a more compact footprint. Oval ducts, combining the features of both round and rectangular types, are also becoming increasingly popular. They offer a sleek appearance while maintaining strong airflow efficiency, making them ideal for modern buildings where performance and design go hand in hand.

North America represented a significant share of the global air ducts market in 2024, with the United States alone contributing approximately USD 930 million in revenue, which equated to nearly 80% of the regional share. The robust growth in construction and infrastructure development across the U.S. has spurred demand for advanced HVAC installations, particularly systems that support long-term sustainability goals. Builders are actively adopting ducts made from eco-conscious materials to comply with green building regulations and certifications. Moreover, the increased incorporation of smart HVAC systems is driving the need for compatible air ducts that can support connected technologies. This is resulting in a shift toward retrofitting older buildings with new-generation ductwork to enhance air quality, energy efficiency, and temperature control.

Key players in the industry are investing in technology upgrades, facility expansions, and strategic partnerships to expand their market presence and meet evolving customer needs. These moves are enabling them to deliver high-performance air duct solutions that align with changing building codes, energy norms, and design expectations across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Urbanization and infrastructure development

- 3.5.1.2 Energy efficiency regulation

- 3.5.1.3 Climate change

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High installation and maintenance costs

- 3.5.2.2 Complexity of retrofitting in existing structures

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Galvanized steel

- 5.3 Aluminum

- 5.4 Fiber glass

- 5.5 Polymers

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Shape, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Rectangular

- 6.3 Round

- 6.4 Oval

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 DC Duct & Sheet Metal

- 9.2 Deflecto

- 9.3 DUNDAS JAFINE

- 9.4 Eastern Sheet Metal

- 9.5 Lindab Group

- 9.6 Lennox International

- 9.7 M&M Manufacturing

- 9.8 Novaflex Group

- 9.9 Nuaire

- 9.10 Rubber World Industries

- 9.11 Ruskin Titus India

- 9.12 Saint-Gobain

- 9.13 Sisneros Bros

- 9.14 Thermaflex

- 9.15 Tin Man Sheet Metal

- 9.16 Turnkey Duct Systems

- 9.17 Zinger Sheet Metal

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日