整形外科用手術ロボットの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Orthopedic Surgical Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721499

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

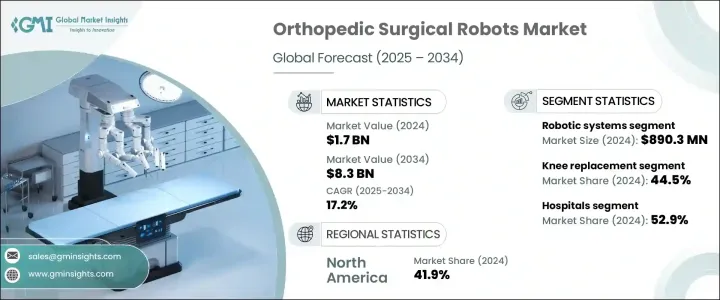

整形外科用手術ロボットの世界市場規模は2024年に17億米ドルとなり、CAGR17.2%で成長し、2034年には83億米ドルに達すると予測されています。

ヘルスケアプロバイダーが手技の正確性を高め、合併症を最小限に抑え、患者の回復を早める方法を模索しているため、高度なロボット支援手術システムの需要が急増し続けています。変形性関節症、靭帯損傷、退行性骨疾患、骨折などの整形外科疾患の有病率が世界的に上昇を続ける中、外科的介入をロボットプラットフォームで行う医療施設が増えています。人口の高齢化、低侵襲手術に対する意識の高まり、関節や脊椎の手術件数の増加が、このシフトをさらに加速させています。

加えて、外科医は、その強化された視覚化機能、リアルタイムのデータ統合、複雑な手技中の器用さの向上により、ロボットシステムを受け入れています。ロボット工学が整形外科手術の実施方法を一変させたことで、より多くの病院や外科センターが患者ケアの最適化のためにこれらのシステムに投資しています。価値観に基づく医療の推進と、いくつかの国における有利な保険適用も、この動向を後押ししています。ロボット工学がAIと機械学習によって進化するにつれて、これらのシステムは今後10年間、整形外科ヘルスケアにおいてさらに大きな役割を果たすと予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 17億米ドル |

| 予測金額 | 83億米ドル |

| CAGR | 17.2% |

コンポーネント分野には、ロボットシステム、アクセサリー、ソフトウェア、サービスが含まれます。ロボットシステムは、2024年に8億9,030万米ドルを生み出しました。これらのシステムは、外科医が繊細な整形外科手術、特に脊椎や関節の手術を行う際に、より優れたコントロールと精度を提供するため、人気を集めています。インプラントのアライメントを改善し、合併症のリスクを低減し、回復時間を短縮する能力により、病院や専門クリニックで好まれています。3D視覚化、触覚フィードバック、高度な画像サポートなどの機能により、ロボットプラットフォームは手術ワークフローを変革し、全体的な治療成績を向上させています。

エンドユース別では、病院セグメントが2024年に52.9%のシェアを占めています。病院は、強力な臨床インフラ、整形外科症例の流入の多さ、技術的アップグレードの重視の高まりから、引き続き市場を独占しています。病院は、手技の一貫性を高め、人的ミスを減らし、複雑な症例をより効率的に管理するために、ロボットシステムに大きく依存しています。老人患者の増加や有利な償還政策も、病院がロボット支援手術ソリューションを採用し、規模を拡大することを容易にしています。

北米整形外科用手術ロボット市場は2024年に41.9%のシェアを占めました。同地域の優位性は、強固なヘルスケアインフラ、AI搭載技術の採用の高まり、精密ベースで低侵襲な整形外科手術のニーズの高まりによる。変形性関節症や骨粗鬆症のような関節関連疾患が増加し続ける中、北米の病院や外科センターは、次世代ロボットシステムの診療への統合を主導しています。

世界整形外科用手術ロボット市場の有力企業には、Medtronic、Think Surgical、Globus Medical、Brainlab、Accuray、MicroPort Orthopedics、Intuitive、Johnson &Johnson、CUREXO、Smith &Nephew、Asensus Surgical、Zimmer Biomet、Corin、Stryker、NUVASIVEなどがあります。これらの企業は研究開発に積極的に投資し、手術精度の向上、AIとハプティクスの統合、多様な臨床ニーズに合わせたソリューションの開発に取り組んでいます。その多くは、病院や販売代理店との提携を通じて世界のプレゼンスを拡大する一方、ユーザーの導入とパフォーマンスを高めるために、強固な販売後サポートとトレーニングを提供しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 整形外科疾患および外傷の増加

- ロボット支援手術技術の進歩

- 低侵襲手術(MIS)の需要増加

- 高齢化人口の増加

- 業界の潜在的リスク&課題

- ロボット手術システムと手術手順の高コスト

- 限定的な払い戻しポリシー

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 規制情勢

- テクノロジーの情勢

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021 –2034

- 主要動向

- ロボットシステム

- アクセサリー

- ソフトウェアとサービス

第6章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 膝関節置換術

- 股関節置換術

- 肩関節置換術

- 脊椎手術

- その他の用途

第7章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 病院

- 外来手術センター(ASC)

- 専門整形外科クリニック

- その他の用途

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Accuray

- Asensus Surgical

- Brainlab

- Corin

- CUREXO

- Globus Medical

- Intuitive

- Johnson &Joshnson

- Medtronic

- MicroPort Orthopedics

- NUVASIVE

- Smith &Nephew

- Stryker

- Think Surgical

- Zimmer Biomet

目次

The Global Orthopedic Surgical Robots Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 17.2% to reach USD 8.3 billion by 2034. The demand for advanced robotic-assisted surgical systems continues to surge as healthcare providers look for ways to increase procedural accuracy, minimize complications, and ensure quicker patient recovery. As the prevalence of orthopedic disorders-including osteoarthritis, ligament injuries, degenerative bone diseases, and fractures-continues to rise globally, more healthcare facilities are shifting toward robotic platforms for surgical interventions. Aging populations, growing awareness about minimally invasive surgeries, and the increasing volume of joint and spinal procedures are further accelerating this shift.

In addition, surgeons are embracing robotic systems due to their enhanced visualization capabilities, real-time data integration, and improved dexterity during complex procedures. With robotics transforming the way orthopedic surgeries are performed, more hospitals and surgical centers are investing in these systems to optimize patient care. The push for value-based care and favorable insurance coverage in several countries is also supporting this trend. As robotics evolve with AI and machine learning, these systems are expected to play an even bigger role in orthopedic healthcare over the coming decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 17.2% |

The component segment includes robotic systems, accessories, software, and services. The robotic systems segment generated USD 890.3 million in 2024. These systems are gaining traction because they offer surgeons greater control and precision in performing delicate orthopedic surgeries, particularly in spinal and joint procedures. Their ability to improve implant alignment, reduce the risk of complications, and shorten recovery time makes them a preferred choice across hospitals and specialty clinics. With features like 3D visualization, haptic feedback, and advanced imaging support, robotic platforms are transforming the surgical workflow and enhancing overall outcomes.

By end use, the hospitals segment held a 52.9% share in 2024. Hospitals continue to dominate the market due to their strong clinical infrastructure, a high influx of orthopedic cases, and a growing emphasis on technological upgrades. They rely heavily on robotic systems to improve procedural consistency, reduce human error, and manage complex cases with greater efficiency. The rising number of geriatric patients and favorable reimbursement policies are also making it easier for hospitals to adopt and scale robotic-assisted surgical solutions.

North America Orthopedic Surgical Robots Market held a 41.9% share in 2024. The region's dominance is driven by its robust healthcare infrastructure, rising adoption of AI-powered technologies, and an increasing need for precision-based, minimally invasive orthopedic procedures. As joint-related conditions like osteoarthritis and osteoporosis continue to rise, North American hospitals and surgical centers are leading the charge in integrating next-gen robotic systems into their practices.

Prominent companies in the Global Orthopedic Surgical Robots Market include Medtronic, Think Surgical, Globus Medical, Brainlab, Accuray, MicroPort Orthopedics, Intuitive, Johnson & Johnson, CUREXO, Smith & Nephew, Asensus Surgical, Zimmer Biomet, Corin, Stryker, and NUVASIVE. These players are actively investing in R&D to refine surgical accuracy, integrate AI and haptics, and develop tailored solutions for diverse clinical needs. Many are expanding their global presence through partnerships with hospitals and distributors, while offering robust post-sales support and training to enhance user adoption and performance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of orthopedic disorders and injuries

- 3.2.1.2 Advancements in robotic-assisted surgery technology

- 3.2.1.3 Increasing demand for minimally invasive surgeries (MIS)

- 3.2.1.4 Rising geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of robotic surgical systems and procedures

- 3.2.2.2 Limited reimbursement policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Robotic systems

- 5.3 Accessories

- 5.4 Software and services

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Knee replacement

- 6.3 Hip replacement

- 6.4 Shoulder replacement

- 6.5 Spinal surgeries

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers (ASCs)

- 7.4 Specialty orthopedic clinics

- 7.5 Other end uses

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accuray

- 9.2 Asensus Surgical

- 9.3 Brainlab

- 9.4 Corin

- 9.5 CUREXO

- 9.6 Globus Medical

- 9.7 Intuitive

- 9.8 Johnson & Joshnson

- 9.9 Medtronic

- 9.10 MicroPort Orthopedics

- 9.11 NUVASIVE

- 9.12 Smith & Nephew

- 9.13 Stryker

- 9.14 Think Surgical

- 9.15 Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日