|

市場調査レポート

商品コード

1721497

静油圧トランスミッション市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Hydrostatic Transmission Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 静油圧トランスミッション市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月07日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

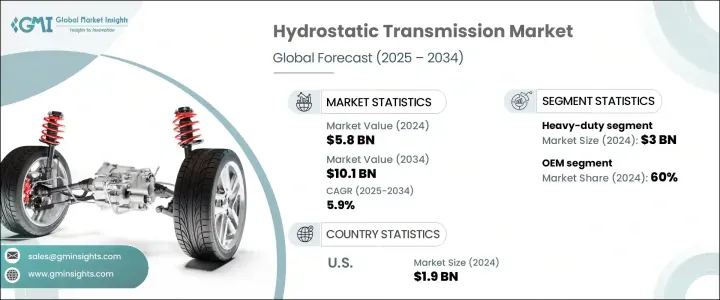

静油圧トランスミッションの世界市場規模は、2024年に58億米ドルとなり、CAGR 5.9%で成長し、2034年には101億米ドルに達すると予測されています。

世界中の産業がよりスマートでクリーン、そしてエネルギー効率の高い技術へと進化を続ける中、静油圧トランスミッションシステムは強い支持を集めています。この市場は、自動車、農業、建設、鉱業などの分野からの需要が高まっており、スムーズで応答性が高く、燃料効率の高い電力供給へのニーズが設計の優先順位を変えています。産業用および車両用プラットフォームにおける自動化と電動化の採用の増加は、トランスミッション技術に大きな影響を及ぼしています。

メーカーは、次世代機器のニーズに対応するため、シームレスな機械操作とインテリジェント制御をサポートする高度な機能の統合に注力しています。エンドユーザーは、精密なハンドリング、排出ガスの削減、高い信頼性を保証するシステムに傾倒しており、これらは、性能主導で持続可能性を意識する今日の状況において極めて重要な要素となっています。さらに、インフラ投資の拡大、労働力不足、スマート農業と自動マテリアルハンドリングの推進が、特に北米、欧州、アジア太平洋、中東・アフリカの静油圧トランスミッション市場に大きな勢いを与えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 58億米ドル |

| 予測金額 | 101億米ドル |

| CAGR | 5.9% |

主要産業全体の成長は、エネルギー効率の高いトランスミッションシステムに対する嗜好の高まりと、シームレスな電力変調に対する需要が大きな原動力となっています。車両性能の向上、正確な制御、燃費の改善は、採用を推進する中核的な利点のひとつです。油圧技術の成熟が進むにつれ、メーカーは電子制御やスマートセンサーなどのインテリジェント機能をシステムに組み込むようになっています。これらの技術革新は車両アーキテクチャを再定義し、よりスムーズな操作とシステムの信頼性向上を可能にしています。自動化された持続可能な機械に向けた動きは、重建設、農業機械、産業車両などのセクターにおける旺盛な需要を後押ししています。

市場セグメンテーションでは、容量別にライトデューティ、ミディアムデューティ、ヘビーデューティの各システムを分類しています。このうち、ヘビーデューティ用静圧トランスミッションは、2024年に30億米ドルの圧倒的なシェアを占めています。この優位性は、高トルク、長寿命、高負荷で過酷な用途での信頼性を実現する能力に起因しています。ヘビーデューティ・システムは、燃料効率を維持しながら過酷な条件下でも安定した性能を発揮するため、特に魅力的です。業界のリーダーたちは、精密制御モジュール、電子管理ユニット、省エネ機能強化などを備えた次世代システムを開発し、高まる産業界の要求に応えています。これらのアップグレードは、ミッションクリティカルな業務におけるヘビーデューティ・ソリューションの足場を固めています。

流通に基づくと、市場はOEMチャネルとアフターマーケットチャネルに分かれます。OEM部門は2024年に60%のシェアを確保し、新しい車両設計へのハイドロスタティックシステムの統合が進んでいることに支えられています。消費者は、内蔵された安全性と自動化機能と同期して動作する工場設置型ユニットをますます好むようになっています。OEMは、ADASやその他のインテリジェントな運転システムとの互換性に最適化されたユニットを提供することで対応しています。この需要は、スムーズなドライブコントロールと燃費節約が譲れないプレミアムモデルの間で特に高いです。安全性と持続可能性の強化を推進する規制上の義務付けが、引き続きOEMの採用を後押ししています。

米国静油圧トランスミッション市場は2024年に19億米ドルを生み出し、2025年から2034年にかけてCAGR 6.2%で成長する見通しです。成長の主な原動力は、油圧システム設計の革新、インフラ投資、農業と建設における精度に焦点を当てた機器の急増です。ハイブリッド変速機やセンサーベースの制御機能の採用が加速しています。自動化と持続可能な産業慣行に国家的な重点が置かれる中、米国市場では様々な用途で展開が急ピッチで進んでいます。

Parker Hannifin社、Dana社、Bosch Rexroth社、John Deere社、CNH Industrial社、Eaton社、Danfoss社、Mahindra &Mahindra社、Husqvarna社、Kubota社などの企業は、研究開発投資、戦略的パートナーシップ、革新的な製品の発売により、優位性を高めています。多くの企業が、ライフサイクル性能と運転効率を最適化するために、IoT対応システムと診断技術に投資しています。OEMとの協業により、先進的な車両プラットフォームへの統合が簡素化される一方、合併や地域拡大により、世界プレーヤーは新興市場の急増する需要によりよく対応できるようになっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- オフロード車両や特殊車両での使用増加

- スマート油圧システムの進歩

- 燃費向上のための規制強化

- ハイブリッド油圧電動パワートレインの開発

- 業界の潜在的リスク&課題

- 初期費用が高め

- 複雑なメンテナンス要件

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:容量別、2021-2034

- 主要動向

- 頑丈

- 中型

- 軽作業用

第6章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- 油圧ポンプ

- 油圧モーター

- バルブとコントロール

- フィルター

- その他

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 農業

- 工事

- マテリアルハンドリング

- その他

第8章 市場推計・予測:トランスミッション別、2021-2034

- 主要動向

- 閉ループ

- オープンループ

第9章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- アフターマーケット

- OEM

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- AGCO

- Ariens

- Bosch Rexroth

- CNH Industrial

- Daedong Industrial

- Dana

- Danfoss

- Eaton

- Husqvarna

- Iseki

- JCB

- John Deere

- Kubota

- Mahindra &Mahindra

- MTD

- Parker Hannifin

- Sauer-Danfoss

- Tuff Torq

- Yanmar

- ZF Friedrichshafen

The Global Hydrostatic Transmission Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 10.1 billion by 2034. As industries worldwide continue to evolve toward smarter, cleaner, and more energy-efficient technologies, hydrostatic transmission systems are gaining strong traction. The market is experiencing heightened demand from sectors such as automotive, agriculture, construction, and mining, where the need for smooth, responsive, and fuel-efficient power delivery is reshaping design priorities. The increasing adoption of automation and electrification across industrial and vehicular platforms is significantly influencing transmission technologies.

Manufacturers are focusing on integrating advanced features that support seamless machine operation and intelligent control to match the needs of next-generation equipment. End users are leaning toward systems that ensure precision handling, reduced emissions, and higher reliability-factors that are crucial in today's performance-driven and sustainability-conscious landscape. Moreover, growing infrastructure investments, labor shortages, and the push for smart farming and automated material handling are adding substantial momentum to the hydrostatic transmission market, especially across North America, Europe, Asia Pacific, and the Middle East & Africa.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 5.9% |

Growth across key industries is largely driven by the rising preference for energy-efficient transmission systems and the demand for seamless power modulation. Enhanced vehicle performance, precise control, and improved fuel economy are among the core benefits propelling adoption. As hydraulic technology continues to mature, manufacturers are incorporating intelligent features such as electronic controls and smart sensors into their systems. These innovations are redefining vehicle architecture, allowing smoother operation and greater system reliability. The movement toward automated, sustainable machinery is fueling robust demand in sectors such as heavy construction, agricultural equipment, and industrial vehicles.

Segmented by capacity, the market includes light-duty, medium-duty, and heavy-duty systems. Among these, heavy-duty hydrostatic transmissions held a commanding USD 3 billion in 2024. This dominance stems from their ability to deliver high torque, long operational life, and reliability in high-load, rugged applications. Heavy-duty systems are especially attractive for their consistent performance under extreme conditions while maintaining fuel efficiency. Industry leaders are developing next-gen systems equipped with precision control modules, electronic management units, and energy-saving enhancements to meet escalating industrial requirements. These upgrades are strengthening the foothold of heavy-duty solutions across mission-critical operations.

Based on distribution, the market is split between OEM and aftermarket channels. The OEM segment secured a 60% share in 2024, bolstered by rising integration of hydrostatic systems into new vehicle designs. Consumers are increasingly favoring factory-installed units that work in sync with built-in safety and automation features. OEMs are responding by delivering units optimized for compatibility with ADAS and other intelligent driving systems. The demand is especially high among premium models where smooth drive control and fuel savings are non-negotiable. Regulatory mandates pushing for enhanced safety and sustainability continue to drive OEM adoption.

United States Hydrostatic Transmission Market generated USD 1.9 billion in 2024 and is poised to grow at 6.2% CAGR between 2025-2034. Growth is primarily driven by innovation in hydraulic system designs, infrastructure investments, and the surge in precision-focused equipment in agriculture and construction. The adoption of hybrid transmissions and sensor-based control features is accelerating. With a national focus on automation and sustainable industrial practices, the US market is witnessing fast-paced deployment across varied applications.

Companies such as Parker Hannifin, Dana, Bosch Rexroth, John Deere, CNH Industrial, Eaton, Danfoss, Mahindra & Mahindra, Husqvarna, and Kubota are sharpening their edge with R&D investments, strategic partnerships, and innovative product launches. Many players are investing in IoT-enabled systems and diagnostic technologies to optimize lifecycle performance and operational efficiency. Collaborations with OEMs are simplifying integration into advanced vehicle platforms, while mergers and regional expansions are enabling global players to better serve the surging demand from emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increased use in off-highway and specialty vehicles

- 3.7.1.2 Advancements in smart hydraulic systems

- 3.7.1.3 Regulatory push for fuel efficiency

- 3.7.1.4 Development of hybrid hydrostatic-electric powertrains

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs

- 3.7.2.2 Complex maintenance requirements

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Heavy-duty

- 5.3 Medium-duty

- 5.4 Light-duty

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Hydraulic pumps

- 6.3 Hydraulic motors

- 6.4 Valves & controls

- 6.5 Filters

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Agriculture

- 7.3 Construction

- 7.4 Material handling

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Transmission, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Closed-loop

- 8.3 Open-loop

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Aftermarket

- 9.3 OEM

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AGCO

- 11.2 Ariens

- 11.3 Bosch Rexroth

- 11.4 CNH Industrial

- 11.5 Daedong Industrial

- 11.6 Dana

- 11.7 Danfoss

- 11.8 Eaton

- 11.9 Husqvarna

- 11.10 Iseki

- 11.11 JCB

- 11.12 John Deere

- 11.13 Kubota

- 11.14 Mahindra & Mahindra

- 11.15 MTD

- 11.16 Parker Hannifin

- 11.17 Sauer-Danfoss

- 11.18 Tuff Torq

- 11.19 Yanmar

- 11.20 ZF Friedrichshafen