|

市場調査レポート

商品コード

1721491

ガラスとアルミ容器包装の市場機会と促進要因、産業動向分析、2025年~2034年予測Glass and Aluminum Containers Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ガラスとアルミ容器包装の市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月07日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

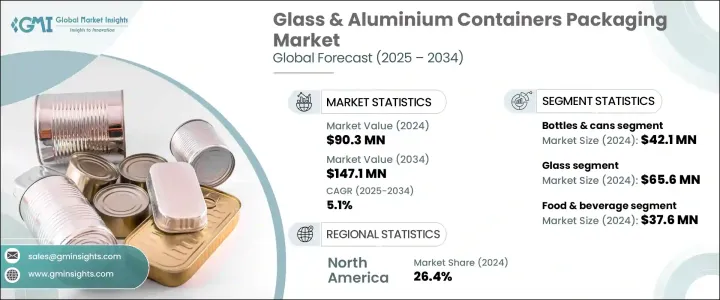

ガラス・アルミ容器包装の世界市場は2024年に9,030万米ドルと評価され、CAGR 5.1%で成長し、2034年には1億4,710万米ドルに達すると予測されています。

持続可能性が各産業を定義する力となるにつれ、環境に優しいパッケージングへの需要が急速に加速しています。消費者はもはや機能性だけを求めているのではなく、環境に対する価値観に沿った製品を積極的に選ぶようになっています。このような行動の変化により、ブランドはカーボンフットプリントを削減し、循環型経済を促進する包装形態を優先するようになっています。完全にリサイクル可能で再利用できるガラスとアルミは、このグリーン革命をリードしています。eコマースの急増による健康と衛生への関心の高まり、プラスチック使用に対する規制圧力の高まりは、持続可能な包装へのシフトをさらに強めています。

飲食品、化粧品、医薬品などの業界は、コンプライアンス基準を満たすためだけでなく、消費者の信頼を得るためにもこの移行を進めています。今やブランドは、包装を地球へのコミットメントを伝え、顧客ロイヤルティを高める戦略的資産と見なしています。コスト効率と美観を向上させる技術革新により、ガラスやアルミの容器は、高級品にも日用品にも選ばれるようになってきています。生産技術の進化に伴い、メーカーはより強く、より軽く、より手頃な価格で、廃棄物ゼロの目標に沿ったソリューションを提供できるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 9,030万米ドル |

| 予測金額 | 1億4,710万米ドル |

| CAGR | 5.1% |

トレイとホイル容器の需要は着実に増加しており、2025年から2034年までのCAGRは5.3%と予測されています。アルミ箔容器は、主にその優れた耐熱性、軽量構造、高いリサイクル性により、フードデリバリーおよび調理済み食品セグメント全体で強い支持を受けています。こうした利点は、食品の保存中や輸送中に食品の鮮度を確実に保つと同時に、持続可能性の目標にも合致しています。同時に、ガラストレーはその電子レンジ対応特性と高級感のある外観から、高級包装の分野でも勢いを増しています。消費者の嗜好が利便性、衛生性、エコ志向にシフトする中、両フォーマットは多様な商業的使用事例に拡大しつつあります。

アルミ包装分野だけでも、2034年までのCAGRは3.8%と予想されています。強度が高く、軽量で、空気、湿気、汚染物質を遮断して製品の完全性を守る能力が評価され、アルミニウムは食品、飲食品、医薬品包装の最重要選択肢になりつつあります。プラスチック廃棄物の削減を目指す世界の政策により、アルミニウムへの移行が加速しています。このような進歩により、アルミニウムの費用対効果とライフサイクル全体にわたる持続可能性が向上し、大規模な用途に実用的な選択肢となっています。

米国のガラス・アルミ容器包装市場は、2034年までに3,220万米ドルに達すると予測されています。環境意識の高まりとプラスチック廃棄物に対する政策主導の行動が、この動向に拍車をかけています。使い捨てプラスチックに対する連邦政府のプログラムや地域の禁止措置は、メーカーにリサイクル可能で低炭素な包装形態を採用するよう促しています。より薄く耐久性のあるガラスや、最適化されたアルミのリサイクル工程などの技術革新は、企業がグリーン目標を達成しながら排出量とコストを削減するのに役立っています。

Ball Corporation、Verallia、Ardagh Group、Crown Holdings、O-I Glass(Owens-Illinois)などの大手企業は、グリーン技術や循環型経済への取り組みに積極的に投資しています。これらの企業は、生産能力を拡大し、リサイクル可能な製品ラインを導入し、持続可能なパッケージング・ソリューションを共同開発するためにブランドとの戦略的提携に取り組んでいます。自動化、廃棄物削減、環境効率の高いプロセスを通じて、進化する規制の枠組みに沿いながら、次世代パッケージングの新たなベンチマークを打ち立てています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 持続可能な包装への需要の高まり

- 厳しい環境規制

- リサイクル技術の進歩

- 成長する飲料および医薬品産業

- 高級感と美的魅力

- 業界の潜在的リスク&課題

- 高い生産コストと輸送コスト

- 壊れやすさと取り扱いの問題

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021 –2034

- 主要動向

- ガラス

- アルミニウム

第6章 市場推計・予測:容器の種類別、2021 –2034

- 主要動向

- ボトルと缶

- 瓶

- トレイ/ホイル容器

- チューブ

- バイアル/アンプル

第7章 市場推計・予測:最終用途産業別、2021 –2034

- 主要動向

- 食品・飲料

- パーソナルケア&化粧品

- 医薬品

- 工業・化学品

- その他

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- O-I Glass(Owens-Illinois)

- Ardagh Group

- Verallia

- BA Glass

- Vitro

- Gerresheimer

- Heinz-Glas

- Nihon Yamamura Glass Co.

- Ball Corporation

- Crown Holdings

- Trivium Packaging

- Can-Pack Group

- Toyo Seikan Group

- Silgan Holdings

The Global Glass & Aluminum Containers Packaging Market was valued at USD 90.3 million in 2024 and is estimated to grow at a CAGR of 5.1% to reach at USD 147.1 million by 2034. As sustainability becomes a defining force across industries, the demand for eco-friendly packaging is rapidly accelerating. Consumers are no longer just looking for functionality-they are actively choosing products that align with their environmental values. This behavioral shift is prompting brands to prioritize packaging formats that reduce carbon footprints and foster circular economy practices. Glass and aluminum, being fully recyclable and reusable, are leading this green revolution. The surge in e-commerce heightened focus on health and hygiene, and increasing regulatory pressures against plastic use are further intensifying the shift toward sustainable packaging.

Industries such as food and beverage, cosmetics, and pharmaceuticals are making this transition not only to meet compliance standards but also to earn consumer trust. Brands now view packaging as a strategic asset that communicates their commitment to the planet and drives customer loyalty. With innovations improving cost-efficiency and aesthetics, glass and aluminum containers are becoming the go-to choice for both premium and everyday products. As production technologies evolve, manufacturers are able to offer stronger, lighter, and more affordable solutions that align with zero-waste goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $90.3 Million |

| Forecast Value | $147.1 Million |

| CAGR | 5.1% |

The demand for trays and foil containers is increasing steadily, with projections indicating a CAGR of 5.3% from 2025 to 2034. Aluminum foil containers are seeing strong uptake across the food delivery and ready-to-eat meal segments, primarily due to their excellent thermal resistance, lightweight structure, and high recyclability. These benefits ensure food remains fresh during storage and transit while aligning with sustainability goals. At the same time, glass trays are gaining momentum in high-end packaging due to their microwave-safe properties and premium look. With consumer preferences shifting toward convenience, hygiene, and eco-consciousness, both formats are expanding into diverse commercial use cases.

The aluminum packaging segment alone is anticipated to witness a CAGR of 3.8% through 2034. Praised for its strength, low weight, and ability to safeguard product integrity by blocking air, moisture, and contaminants, aluminum is becoming a top choice for food, beverage, and pharmaceutical packaging. Global policies aimed at reducing plastic waste are accelerating the shift to aluminum, especially as recycling infrastructure and technologies continue to improve. These advancements enhance aluminum's cost-effectiveness and sustainability across its lifecycle, making it a practical choice for large-scale applications.

The U.S. Glass & Aluminum Containers Packaging Market is forecasted to reach USD 32.2 million by 2034. Growing environmental awareness and policy-driven action against plastic waste are fueling this trend. Federal programs and local bans on single-use plastics are encouraging manufacturers to adopt recyclable, low-carbon packaging formats. Innovations such as thinner yet more durable glass and optimized aluminum recycling processes are helping companies cut emissions and costs while meeting green targets.

Major players, including Ball Corporation, Verallia, Ardagh Group, Crown Holdings, and O-I Glass (Owens-Illinois), are actively investing in green technologies and circular economy initiatives. These companies are scaling up production capabilities, introducing recyclable product lines, and engaging in strategic collaborations with brands to co-develop sustainable packaging solutions. Through automation, waste reduction, and eco-efficient processes, they are setting new benchmarks in next-generation packaging while aligning with evolving regulatory frameworks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable packaging

- 3.2.1.2 Stringent environmental regulations

- 3.2.1.3 Advancements in recycling technology

- 3.2.1.4 Growing beverage and pharmaceutical industries

- 3.2.1.5 Premium and aesthetic appeal

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and transportation costs

- 3.2.2.2 Breakability and Handling Issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn & million units)

- 5.1 Key trends

- 5.2 Glass

- 5.3 Aluminum

Chapter 6 Market Estimates and Forecast, By Container Type, 2021 – 2034 ($ Mn & million units)

- 6.1 Key trends

- 6.2 Bottles & Cans

- 6.3 Jars

- 6.4 trays/foil containers

- 6.5 tubes

- 6.6 Vials/ampoules

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 ($ Mn & million units)

- 7.1 Key trends

- 7.2 Food & Beverage

- 7.3 Personal Care & Cosmetics

- 7.4 Pharmaceuticals

- 7.5 Industrial & Chemicals

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn & million units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 O-I Glass (Owens-Illinois)

- 9.2 Ardagh Group

- 9.3 Verallia

- 9.4 BA Glass

- 9.5 Vitro

- 9.6 Gerresheimer

- 9.7 Heinz-Glas

- 9.8 Nihon Yamamura Glass Co.

- 9.9 Ball Corporation

- 9.10 Crown Holdings

- 9.11 Trivium Packaging

- 9.12 Can-Pack Group

- 9.13 Toyo Seikan Group

- 9.14 Silgan Holdings