|

市場調査レポート

商品コード

1721474

浸潤性乳管がん治療薬の市場機会と成長促進要因、産業動向分析、2025年~2034年予測Invasive Ductal Carcinoma (IDC) Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 浸潤性乳管がん治療薬の市場機会と成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月03日

発行: Global Market Insights Inc.

ページ情報: 英文 142 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

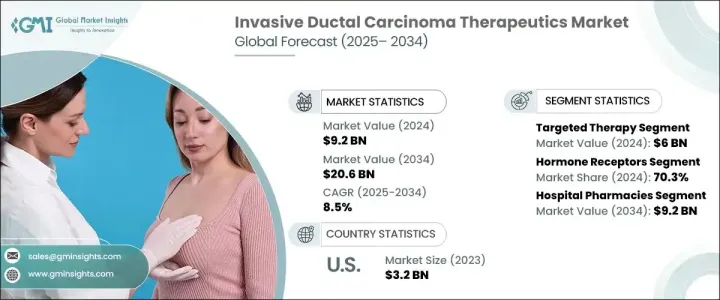

浸潤性乳管がん治療薬の世界市場は、2024年には92億米ドルと評価され、CAGR 8.5%で成長し、2034年には206億米ドルに達すると予測されています。

この堅調な成長見通しは、世界中で乳がんの有病率が一貫して上昇しており、浸潤性乳管がんが最も頻繁に診断されるサブタイプであることが背景にあります。浸潤性乳管がんは浸潤性乳がん症例全体の80%近くを占めており、腫瘍学において重要な領域となっています。乳がん検診プログラムが拡大し、早期発見が改善するにつれて、ヘルスケアプロバイダーはIDCの診断数が顕著に増加していることを目の当たりにしています。その結果、生存率を向上させるだけでなく、生活の質を高める効果的で患者中心の治療に対する需要が高まり続けています。がんの負担の増大は、治療革新の必要性を加速させており、IDC治療薬の領域は、先進的なソリューションでその必要性を満たすべく急速に進化しています。患者や臨床医の意識の高まり、有利な償還シナリオ、先進国や新興経済諸国における医療インフラの拡大も、この市場の持続的な勢いに寄与しています。

従来の化学療法がIDCを管理する上で重要な要素であることに変わりはないが、革新的な標的治療へのシフトが加速しています。ホルモン療法と生物学的製剤は、その有効性の向上と毒性プロファイルの低減により、好ましい治療選択肢となりつつあります。アロマターゼ阻害薬や選択的エストロゲン受容体分解薬(SERDs)などの治療薬は、診断のかなりの部分を占めるホルモン受容体陽性(HR+)IDC症例に特に有効です。これらの治療は、患者がより少ない副作用でより良好な病勢コントロールを達成するのに役立っており、医師と患者の双方がこのような先進的アプローチに傾倒するよう促しています。その結果、標的治療薬はIDC治療プロトコールに不可欠な要素となりつつあり、市場の上昇基調をさらに強めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 92億米ドル |

| 予測金額 | 206億米ドル |

| CAGR | 8.5% |

IDC治療薬市場は、最終用途別に病院、腫瘍クリニック、その他のヘルスケア施設に区分されます。病院は、統合的ながん治療、最先端の診断システム、集学的ながん治療チームへのアクセスを提供できることから、2034年までに36億米ドルの売上が見込まれています。このような環境は、化学療法、免疫療法、精密医療を含む複雑な治療レジメンの包括的管理をサポートし、IDC治療の有力な選択肢であり続ける。

北米では、米国が浸潤性乳管がん治療薬市場でトップシェアを占めているが、これは同地域の高い疾患罹患率と強力なヘルスケア体制に支えられています。有名ながん治療センターが存在し、新規治療薬へのアクセスが広がっていることが、浸潤性乳管がん治療薬の採用を後押ししています。

この分野の主要企業には、AbbVie、AstraZeneca、Bristol-Myers Squibb、Celldex Therapeutics、Eli Lilly、F. Hoffmann-La Roche、Janssen Pharmaceuticals、Macrogenics、Merck、Novartis、Pfizerなどがあります。これらの企業は、より優れた臨床結果と副作用の少ない最先端の免疫療法や併用療法を導入するため、研究開発に多額の投資を行っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 乳がんの罹患率と認知度の向上

- 診断技術の向上

- 治療選択肢の拡大

- 業界の潜在的リスク&課題

- 治療費が高め

- 特定の治療法に対する副作用と耐性

- 促進要因

- 成長可能性分析

- 規制情勢

- パイプライン分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤の種類別、2021-2034

- 主要動向

- 標的療法

- アベマシクリブ

- アドトラスツズマブエムタンシン

- エベロリムス

- トラスツズマブ

- リボシクリブ

- パルボシクリブ

- ペルツズマブ

- オラパリブ

- その他の標的療法

- ホルモン療法

- 選択的エストロゲン受容体モジュレーター(SERM)

- アロマターゼ阻害剤

- 選択的エストロゲン受容体分解薬(SERD)

- 化学療法

- 免疫療法

第6章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- ホルモン受容体

- HER2陽性

- トリプルネガティブ乳がん(TNBC)

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 腫瘍学クリニック

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- AbbVie

- AstraZeneca

- Bristol-Myers Squibb Company

- Celldex Therapeutics

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Gilead Sciences

- Janssen Pharmaceuticals

- Macrogenics

- Merck

- Novartis

- Pfizer

The Global Invasive Ductal Carcinoma Therapeutics Market was valued at USD 9.2 billion in 2024 and is projected to grow at a CAGR of 8.5% to reach USD 20.6 billion by 2034. This robust growth outlook is fueled by the consistently rising prevalence of breast cancer worldwide, with invasive ductal carcinoma being the most frequently diagnosed subtype. IDC accounts for nearly 80% of all invasive breast cancer cases, making it a significant area of focus in oncology. As breast cancer screening programs expand and early detection improves, healthcare providers are witnessing a notable increase in the number of IDC diagnoses. This, in turn, continues to drive demand for effective, patient-centric therapies that not only improve survival rates but also enhance the quality of life. The growing burden of cancer has accelerated the need for treatment innovation, and the IDC therapeutics space is rapidly evolving to meet that need with advanced solutions. Increasing awareness among patients and clinicians, favorable reimbursement scenarios, and expanding healthcare infrastructure across developed and emerging economies are also contributing to this market's sustained momentum.

While conventional chemotherapy remains a key component in managing IDC, the shift toward innovative and targeted therapies is gaining speed. Hormone-based therapies and biologics are becoming the preferred treatment options due to their enhanced efficacy and reduced toxicity profiles. Therapies such as aromatase inhibitors and selective estrogen receptor degraders (SERDs) are especially effective in hormone receptor-positive (HR+) IDC cases, which represent a significant portion of diagnoses. These treatments are helping patients achieve better disease control with fewer side effects, prompting both physicians and patients to lean toward such advanced approaches. As a result, targeted therapeutics are becoming an indispensable element in IDC care protocols, further reinforcing the market's upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $20.6 Billion |

| CAGR | 8.5% |

The IDC therapeutics market is segmented by end-use into hospitals, oncology clinics, and other healthcare facilities. Hospitals are expected to generate USD 3.6 billion by 2034, owing to their ability to provide integrated cancer care, state-of-the-art diagnostic systems, and access to multidisciplinary oncology teams. These environments support comprehensive management of complex treatment regimens involving chemotherapy, immunotherapy, and precision medicines, thereby remaining the go-to option for IDC treatment.

In North America, the U.S. holds a leading share of the invasive ductal carcinoma therapeutics market, backed by the region's high disease prevalence and strong healthcare framework. The presence of renowned cancer treatment centers and widespread access to novel therapeutics are driving the adoption of IDC treatments.

Leading companies in this space include AbbVie, AstraZeneca, Bristol-Myers Squibb, Celldex Therapeutics, Eli Lilly, F. Hoffmann-La Roche, Janssen Pharmaceuticals, Macrogenics, Merck, Novartis, and Pfizer. These players are investing heavily in R&D to introduce cutting-edge immunotherapies and combination therapies that deliver better clinical outcomes and fewer side effects.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence and awareness of breast cancer

- 3.2.1.2 Improved diagnostic technologies

- 3.2.1.3 Expanding therapeutic options

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Side effects and resistance to certain therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Targeted therapy

- 5.2.1 Abemaciclib

- 5.2.2 Ado-trastuzumab emtansine

- 5.2.3 Everolimus

- 5.2.4 Trastuzumab

- 5.2.5 Ribociclib

- 5.2.6 Palbociclib

- 5.2.7 Pertuzumab

- 5.2.8 Olaparib

- 5.2.9 Other targeted therapies

- 5.3 Hormone therapy

- 5.3.1 Selective estrogen receptor modulators (SERMs)

- 5.3.2 Aromatase inhibitors

- 5.3.3 Selective estrogen receptor degraders (SERDs)

- 5.4 Chemotherapy

- 5.5 Immunotherapy

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hormone receptor

- 6.3 HER2+

- 6.4 Triple-negative breast cancer (TNBC)

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Oncology clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 AstraZeneca

- 9.3 Bristol-Myers Squibb Company

- 9.4 Celldex Therapeutics

- 9.5 Eli Lilly and Company

- 9.6 F. Hoffmann-La Roche

- 9.7 Gilead Sciences

- 9.8 Janssen Pharmaceuticals

- 9.9 Macrogenics

- 9.10 Merck

- 9.11 Novartis

- 9.12 Pfizer