|

市場調査レポート

商品コード

1721472

ゲートオールアラウンドトランジスタの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Gate-All-Around (GAA) Transistor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ゲートオールアラウンドトランジスタの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月11日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

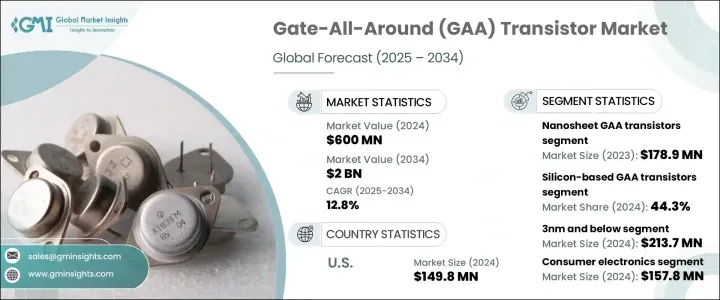

ゲートオールアラウンドトランジスタの世界市場は、2024年に6億米ドルと評価され、CAGR12.8%で成長し、2034年までには20億米ドルに達すると予測されています。

この成長の原動力は、高性能プロセッサの需要増加、5Gネットワークの拡大、エッジコンピューティング技術の台頭です。GAAトランジスタは、モバイルプロセッサ、ネットワークハードウェア、AI駆動型プラットフォームで使用される次世代チップセットで重要な役割を果たすことになります。従来のFinFET設計に比べてエネルギー効率が向上し、スイッチング速度が速く、静電制御に優れているGAAトランジスタは、最新のコンピューティングアプリケーションの性能要求に対応する理想的なソリューションです。クラウドコンピューティング、電気通信、自動車などのデータ集約型産業が進化する中、GAAトランジスタは将来技術の礎石として台頭しつつあります。

ナノシートGAAトランジスタは市場で最も顕著なセグメントとなっており、2023年には1億7,890万米ドルを生み出します。これらのトランジスタは、短チャネル効果の高度な制御、3nm以下のプロセスノードに対するスケーラビリティの向上、トランジスタ密度の向上により、高い支持を得ています。大手半導体鋳造所は、電力効率とチップ性能を高めるためにナノシートアーキテクチャを採用しており、AI、高性能コンピューティング、モバイルプラットフォームにとって重要な選択肢となっています。ナノシートGAAトランジスタが既存の製造装置と互換性があることも、大規模生産での急速な採用に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 6億米ドル |

| 予測金額 | 20億米ドル |

| CAGR | 12.8% |

シリコンベースのGAAトランジスタセグメントは、2024年に44.3%の市場シェアを占めました。シリコンのコスト効率と確立された半導体製造プロセスとの互換性が、その優位性に寄与しています。IntelやTaiwan Semiconductor Manufacturing Company(TSMC)などの大手企業は、5nm以下の技術でシリコンベースのナノシート設計を活用し、エネルギー効率を最適化し、ロジック密度を高めています。これらの進歩は、デジタルデバイスの高まる性能ニーズを満たし、トランジスタサイズの縮小という課題に対処するために極めて重要です。

ドイツでは、GAAトランジスタ市場は2034年までに1億1,260万米ドルに達すると予想されています。自動車、オートメーション、スマートマニュファクチャリングなどの産業と連携する同国の強力な半導体部門が、GAAトランジスタの採用を後押ししています。特に、GAA技術は電気自動車システムや産業オートメーションプラットフォームに組み込まれています。ドイツはまた、先端チップ技術の最前線に立ち続けるために研究に多額の投資を行っており、半導体の自立と技術主権を目指す欧州戦略における重要なプレーヤーとしての地位を確立しています。

同市場には、Intel、Samsung Electronics、Taiwan Semiconductor Manufacturing Company(TSMC)といった業界大手が大きく貢献しています。これらの主要企業は、ナノシートおよびフォークシートトランジスタアーキテクチャーの研究開発に多額の投資を行っています。さらに、設計ツールプロバイダや鋳造企業と戦略的パートナーシップを結び、市場投入までの時間を短縮するとともに、地理的範囲を拡大し、政府出資の半導体イニシアティブに参加しています。これらの努力は、急速に進化するGAAトランジスタ市場における競争力を維持するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 成長促進要因

- 高性能コンピューティング(HPC)の需要の増加

- 半導体製造技術の進歩

- 5Gとエッジコンピューティングの成長

- AIとIoTデバイスへの投資の増加

- 鋳造とIDMによる戦略的拡大

- 業界の潜在的リスク・課題

- 製造の複雑さと高コスト

- サプライチェーンと収量に関する課題

- 成長促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- ナノシートGAAトランジスタ

- ナノワイヤGAAトランジスタ

- フォークシートGAAトランジスタ

- その他

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- シリコンベースのGAAトランジスタ

- ゲルマニウムベースのGAAトランジスタ

- III-V族化合物半導体GAAトランジスタ

第7章 市場推計・予測:ノードサイズ別、2021年~2034年

- 主要動向

- 3nm以下

- 3nm以上

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 高性能コンピューティング(HPC)

- モノのインターネット(IoT)デバイス

- AI・機械学習プロセッサ

- 5G・通信インフラ

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- コンシューマーエレクトロニクス

- 自動車

- データセンター・クラウドコンピューティング

- 産業用電子機器

- ヘルスケア・医療機器

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Analog Devices

- ams-OSRAM AG

- Broadcom Inc.

- Everlight Electronics Co.、Ltd.

- Honeywell International Inc.

- Melexis NV

- Microchip Technology Inc.

- OmniVision Technologies、Inc.

- ON Semiconductor Corporation

- Panasonic Corporation

- Renesas Electronics Corporation

- ROHM Semiconductor

- Samsung Electronics Co.、Ltd.

- Sharp Corporation

- Silicon Labs

- Sony Semiconductor Solutions Corporation

- STMicroelectronics

- Texas Instruments Incorporated

- Vishay Intertechnology

The Global Gate-All-Around Transistor Market was valued at USD 600 million in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 2 billion by 2034. This growth is driven by the increasing demand for high-performance processors, the expansion of 5G networks, and the rise of edge computing technologies. GAA transistors are poised to play a critical role in next-generation chipsets used across mobile processors, network hardware, and AI-driven platforms. Their enhanced energy efficiency, faster switching capabilities, and superior electrostatic control compared to traditional FinFET designs make them an ideal solution for addressing the performance demands of modern computing applications. As data-intensive industries like cloud computing, telecom, and automotive evolve, GAA transistors are emerging as a cornerstone for future technology.

Nanosheet GAA transistors have become the most prominent segment in the market, generating USD 178.9 million in 2023. These transistors are highly favored due to their advanced control over short-channel effects, improved scalability for sub-3nm process nodes, and higher transistor density. Leading semiconductor foundries are adopting nanosheet architecture to enhance power efficiency and chip performance, making them a critical choice for AI, high-performance computing, and mobile platforms. The compatibility of nanosheet GAA transistors with existing manufacturing equipment is also contributing to their rapid adoption in large-scale production.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $600 Million |

| Forecast Value | $2 Billion |

| CAGR | 12.8% |

The silicon-based GAA transistor segment held a 44.3% market share in 2024. Silicon's cost-effectiveness and compatibility with established semiconductor fabrication processes contribute to its dominance. Major players like Intel and Taiwan Semiconductor Manufacturing Company (TSMC) are leveraging silicon-based nanosheet designs in their sub-5nm technologies, optimizing energy efficiency, and boosting logic density. These advancements are crucial for meeting the growing performance needs of digital devices and addressing the challenges of shrinking transistor sizes.

In Germany, the GAA transistor market is set to reach USD 112.6 million by 2034. The country's strong semiconductor sector, aligned with industries like automotive, automation, and smart manufacturing, is driving the adoption of GAA transistors. Notably, GAA technology is being integrated into electric vehicle systems and industrial automation platforms. Germany is also investing heavily in research to stay at the forefront of advanced chip technologies, positioning itself as a key player in Europe's strategy for semiconductor self-reliance and technological sovereignty.

The market is witnessing significant contributions from industry giants such as Intel, Samsung Electronics, and Taiwan Semiconductor Manufacturing Company (TSMC). These leading companies are investing heavily in research and development for nanosheet and forksheet transistor architectures. Additionally, they are forming strategic partnerships with design tool providers and foundries to speed up time-to-market, while expanding their geographic reach and participating in government-funded semiconductor initiatives. These efforts help maintain their competitive edge in the rapidly evolving GAA transistor market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for High-Performance Computing (HPC)

- 3.6.1.2 Advancements in semiconductor fabrication technology

- 3.6.1.3 Growth in 5G and edge computing

- 3.6.1.4 Rising investments in AI and IoT devices

- 3.6.1.5 Strategic expansion by foundries and IDMs

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High manufacturing complexity and costs

- 3.6.2.2 Supply chain and yield challenges

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Nanosheet GAA transistors

- 5.3 Nanowire GAA transistors

- 5.4 Forksheet GAA transistors

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Material, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Silicon-based GAA transistors

- 6.3 Germanium-based GAA transistors

- 6.4 III-V compound semiconductor GAA transistors

Chapter 7 Market Estimates & Forecast, By Node Size, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 3nm and below

- 7.3 Above 3nm

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 High-Performance Computing (HPC)

- 8.3 Internet of Things (IoT) devices

- 8.4 AI & machine learning processors

- 8.5 5G & communication infrastructure

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Consumer electronics

- 9.3 Automotive

- 9.4 Data centers & cloud computing

- 9.5 Industrial electronics

- 9.6 Healthcare & medical devices

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Analog Devices

- 11.2 ams-OSRAM AG

- 11.3 Broadcom Inc.

- 11.4 Everlight Electronics Co., Ltd.

- 11.5 Honeywell International Inc.

- 11.6 Melexis NV

- 11.7 Microchip Technology Inc.

- 11.8 OmniVision Technologies, Inc.

- 11.9 ON Semiconductor Corporation

- 11.10 Panasonic Corporation

- 11.11 Renesas Electronics Corporation

- 11.12 ROHM Semiconductor

- 11.13 Samsung Electronics Co., Ltd.

- 11.14 Sharp Corporation

- 11.15 Silicon Labs

- 11.16 Sony Semiconductor Solutions Corporation

- 11.17 STMicroelectronics

- 11.18 Texas Instruments Incorporated

- 11.19 Vishay Intertechnology