|

市場調査レポート

商品コード

1721462

サトウキビ包装の市場機会、成長促進要因、産業動向分析と2025年~2034年予測Sugarcane Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| サトウキビ包装の市場機会、成長促進要因、産業動向分析と2025年~2034年予測 |

|

出版日: 2025年04月08日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

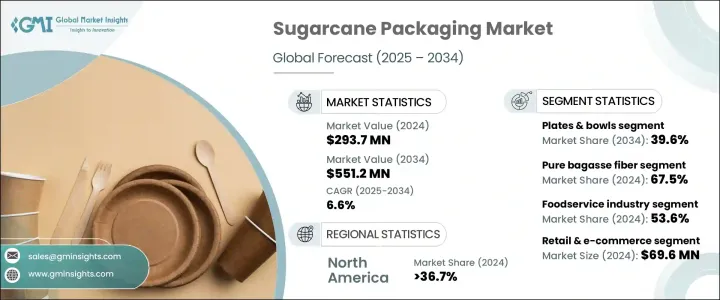

世界のサトウキビ包装市場は、2024年に2億9,370万米ドルと評価され、CAGR 6.6%で成長し、2034年には5億5,120万米ドルに達すると推定されています。

この成長軌道は、規制の変更、消費者行動の変化、企業の環境戦略によって、包装における持続可能で環境に配慮した代替品への世界のシフトを反映しています。気候変動と環境への懸念が依然として前面に出ているため、企業は石油ベースの包装を再生可能で堆肥化可能なオプションに積極的に置き換えています。サトウキビバガスを原料とする素材が各業界で台頭する中、市場は力強い勢いを見せています。消費者は現在、環境に配慮した価値観に沿った製品を支持する傾向にあり、企業はESGへのコミットメントを強化するパッケージング・ソリューションを優先することで対応しています。世界各国が使い捨てプラスチックの規制を導入し、産業界に廃棄物削減の圧力をかけている中、サトウキビ包装は、性能と持続可能性の両方の目標に合致する、革新的で費用対効果の高いソリューションとして登場しました。

バガスは、サトウキビからジュースを抽出した後に残る繊維状の製品別で、この環境に優しいパッケージングシフトの中核をなすものです。セルロース、リグニン、ヘミセルロースからなるこの素材は、自然に生分解され、堆肥化可能です。セルロースナノファイバーとバイオ複合材料に関する研究が進化を続ける中、メーカーは耐久性が向上し、幅広い用途が期待できる先進パッケージングを開発しています。構造的完全性、多用途性、環境的利点が改善されたことで、外食産業から小売業に至るまで、幅広い業界から関心が寄せられています。これらの技術革新は、環境への影響を最小限に抑えるだけでなく、企業が持続可能性のベンチマークや消費者の期待の高まりに準拠するのにも役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2億9,370万米ドル |

| 予測金額 | 5億5,120万米ドル |

| CAGR | 6.6% |

フードサービス分野では、プレートとボウルが2024年に最大の収益シェアを占め、1億1,640万米ドルを生み出しました。これらの製品は、堆肥化可能性を損なうことなく耐湿性、耐油性を提供するため、レストラン、ケータリングサービス、フードデリバリープロバイダーに広く支持されています。便利で環境に優しい包装への需要が伸び続けているため、この分野は一貫した拡大が見込まれています。消費者も企業も同様に、品質を犠牲にすることなく、日常使用で持続可能な性能を発揮する代替品を求めています。

カップと蓋の分野は、ファストフードチェーン、コーヒーショップ、イベントサービスプロバイダによる堆肥化可能飲料容器の急速な普及を反映して、2024年には6,680万米ドルと評価されました。サトウキビベースのカップは耐熱性が強く、漏れにくいため、温かい飲料にも冷たい飲料にも適しています。プラスチック廃棄物をなくそうという動きが強まる中、ホスピタリティセクターの各企業は生分解性ドリンクウェアへの移行を進めており、予測期間中の同分野の成長を後押ししています。

米国のサトウキビ包装市場は2024年に8,820万米ドルを生み出し、2034年までCAGR 6.3%で拡大し、大きな牽引力となっています。カリフォルニア州やニューヨーク州など、使い捨てプラスチックの禁止を実施した州における規制開発が、堆肥化可能な代替品の採用を加速させています。持続可能な調達がビジネスの中核となるにつれ、米国はサトウキビを原料とする包装の有望市場としての地位を固めつつあります。

世界市場の成長を牽引する主要企業には、エコレーツ、フタマキ、Pactiv Evergreen、Dart Container Corporation、Detmold Group、Berry Global Inc.などがあります。これらの企業は、堆肥化可能な製品ポートフォリオの拡大、流通網の強化、ファーストフードチェーンや小売ブランドとの長期契約獲得に多額の投資を行っています。また、効率的に生産規模を拡大し、多様な規制や顧客の需要に応えるため、現地生産に注力し、生分解性材料の研究を進めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- ベンダーマトリックス

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 業界への影響要因

- 促進要因

- ESG(環境、社会、ガバナンス)の優先事項の拡大

- 政府の取り組みとインセンティブ

- 消費者の環境意識の高まり

- ブランドイメージと市場差別化の強化

- 研究開発と持続可能な製造への投資の増加

- 業界の潜在的リスク&課題

- 高い生産コスト

- サプライチェーンとスケーラビリティの問題

- 促進要因

- ポーターの分析

- PESTEL分析

- 将来の市場動向

- 規制情勢

第4章 市場推計・予測:製品タイプ別、2021 –2034

- 主要動向

- バッグ&ポーチ

- 皿とボウル

- カップと蓋

- クラムシェル/コンテナ

- その他

第5章 市場推計・予測:材質別、2021 –2034

- 主要動向

- 純粋なバガス繊維

- ブレンドバガス

第6章 市場推計・予測:最終用途産業別、2021 –2034

- 主要動向

- 食品サービス業界

- 小売・Eコマース

- ヘルスケア部門

- 消費財

- 産業用途

第7章 市場推計・予測:地域別、2021–2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 日本

- 中国

- インド

- 韓国

- オーストラリア・ニュージーランド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東・アフリカ地域

第8章 企業プロファイル

- Berry Global Inc.

- BioPak

- Dart Container Corporation

- Detmold Group

- ECO Guardian

- Ecolates

- good natured Products Inc.

- Good Start Packaging

- GreenLine Paper Co.

- Huhtamaki

- Material Motion、Inc.

- Packman

- Pactiv Evergreen

- PAKKA

- Pappco Greenware

- TedPack Company Limited

- Vegware Ltd

The Global Sugarcane Packaging Market was valued at USD 293.7 million in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 551.2 million by 2034. This growth trajectory reflects a global shift toward sustainable and eco-conscious alternatives in packaging, driven by regulatory changes, changing consumer behavior, and corporate environmental strategies. As climate change and environmental concerns remain front and center, businesses are actively replacing petroleum-based packaging with renewable, compostable options. The market is seeing robust momentum as sugarcane bagasse-based materials gain ground across industries. Consumers are now more inclined to support products that align with green values, and enterprises are responding by prioritizing packaging solutions that reinforce their ESG commitments. With countries around the world adopting restrictions on single-use plastics and putting pressure on industries to cut down waste, sugarcane packaging has emerged as an innovative, cost-effective solution that aligns with both performance and sustainability goals.

Bagasse, the fibrous byproduct left after juice extraction from sugarcane, is at the core of this eco-friendly packaging shift. Comprising cellulose, lignin, and hemicellulose, this material is naturally biodegradable and compostable. As research continues to evolve around cellulose nanofibers and bio-composite materials, manufacturers are developing advanced packaging options with enhanced durability and broader application potential. The improved structural integrity, versatility, and environmental benefits are attracting interest from industries ranging from food service to retail. These innovations are not only minimizing environmental impact but also helping companies comply with rising sustainability benchmarks and consumer expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $293.7 Million |

| Forecast Value | $551.2 Million |

| CAGR | 6.6% |

In the food service sector, plates and bowls accounted for the largest revenue share in 2024, generating USD 116.4 million. These products are widely favored by restaurants, catering services, and food delivery providers because they offer moisture and grease resistance without compromising compostability. As the demand for convenient, eco-friendly packaging continues to grow, this segment is expected to witness consistent expansion. Consumers and businesses alike are looking for alternatives that do not sacrifice quality while delivering sustainable performance for everyday use.

The cups and lids segment was valued at USD 66.8 million in 2024, reflecting a rapid uptake of compostable beverage containers by fast food chains, coffee shops, and event service providers. The strong heat resistance and leak-proof capabilities of sugarcane-based cups make them suitable for both hot and cold beverages. With a growing push to eliminate plastic waste, businesses across the hospitality sector are transitioning to biodegradable drinkware, fueling segment growth over the forecast period.

The United States Sugarcane Packaging Market generated USD 88.2 million in 2024 and is gaining significant traction, expanding at a CAGR of 6.3% through 2034. Regulatory developments in states like California and New York, which have implemented bans on single-use plastics, are accelerating the adoption of compostable alternatives. As sustainable procurement becomes a core business focus, the U.S. is solidifying its position as a high-potential market for sugarcane-based packaging.

Key players driving growth in the global market include Ecolates, Huhtamaki, Pactiv Evergreen, Dart Container Corporation, Detmold Group, and Berry Global Inc. These companies are heavily investing in expanding their compostable product portfolios, strengthening distribution networks, and partnering with fast-food chains and retail brands to secure long-term contracts. They're also focusing on localized manufacturing and advancing biodegradable material research to scale production efficiently and meet diverse regulatory and customer demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Vendor matrix

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Industry impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growing ESG (Environmental, Social, and Governance) Priorities

- 3.7.1.2 Government Initiatives and Incentives

- 3.7.1.3 Growing Consumer Environmental Awareness

- 3.7.1.4 Enhanced Brand Image and Market Differentiation

- 3.7.1.5 Increased Investment in R&D and Sustainable Manufacturing

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High production Costs

- 3.7.2.2 Supply Chain and Scalability Issues

- 3.7.1 Growth drivers

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Regulatory landscape

Chapter 4 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Mn & kilotons)

- 4.1 Key trends

- 4.2 Bags & Pouches

- 4.3 Plates & Bowls

- 4.4 Cups & Lids

- 4.5 Clamshells/Containers

- 4.6 Others

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Mn & kilotons)

- 5.1 Key trends

- 5.2 Pure bagasse fiber

- 5.3 Blended bagasse

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Mn & kilotons)

- 6.1 Key trends

- 6.2 Foodservice industry

- 6.3 Retail & E-Commerce

- 6.4 Healthcare sector

- 6.5 Consumer goods

- 6.6 Industrial applications

Chapter 7 Market Estimates and Forecast, By Region, 2021– 2034 (USD Mn & kilotons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 ANZ

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 UAE

- 7.6.3 Saudi Arabia

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Berry Global Inc.

- 8.2 BioPak

- 8.3 Dart Container Corporation

- 8.4 Detmold Group

- 8.5 ECO Guardian

- 8.6 Ecolates

- 8.7 good natured Products Inc.

- 8.8 Good Start Packaging

- 8.9 GreenLine Paper Co.

- 8.10 Huhtamaki

- 8.11 Material Motion, Inc.

- 8.12 Packman

- 8.13 Pactiv Evergreen

- 8.14 PAKKA

- 8.15 Pappco Greenware

- 8.16 TedPack Company Limited

- 8.17 Vegware Ltd