|

市場調査レポート

商品コード

1721457

血漿プロテアーゼC1阻害剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Plasma Protease C1-inhibitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 血漿プロテアーゼC1阻害剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月02日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

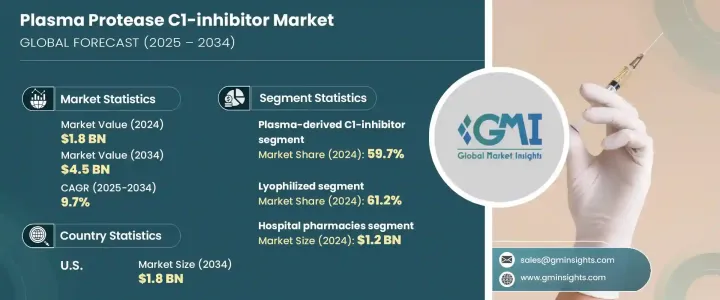

世界の血漿プロテアーゼC1阻害剤市場は、2024年に18億米ドルと評価され、CAGR 9.7%で成長し、2034年には45億米ドルに達すると推定されています。

血漿プロテアーゼC1阻害剤は、人体内の補体系と接触系の活性化を制御する上で重要な役割を果たしています。血漿に由来するこれらのタンパク質は、遺伝性血管性浮腫(HAE)のような稀な遺伝性疾患の治療において極めて重要です。ヘルスケアシステムが進化し続ける中、希少疾患の管理に対する意識が高まっており、C1阻害剤のような効果的で専門的な治療薬に対する需要に大きく寄与しています。

血漿分画および採取法の技術的進歩は、血漿由来の治療薬の収量と純度を高めることにより、生物学的製剤の状況を再構築しています。その結果、これらの開発により、ヘルスケアプロバイダーにとっても患者にとっても、治療がより利用しやすく、手頃な価格で、スケーラブルなものになりつつあります。臨床的関心の高まりと個別化医療の台頭により、市場は炎症性疾患や自己免疫疾患などの新たな治療応用分野への浸透が進むものと思われます。先進国、新興経済諸国ともに、規制当局の支援やヘルスケアインフラの整備が進んでいることも、市場開拓をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 18億米ドル |

| 予測金額 | 45億米ドル |

| CAGR | 9.7% |

薬剤クラス別では、血漿由来のC1阻害薬セグメントが市場を独占し、2024年の世界シェアの59.7%を占めました。選択的ブラジキニンB2受容体拮抗薬やカリクレイン阻害薬のような代替選択肢もあるが、現在のところ市場内では小規模なセグメントにとどまっています。血漿由来の製剤は、その確立された安全性プロファイルと、HAEの急性治療および予防治療における実証された有効性により、依然として好ましい選択肢です。

剤形を見ると、凍結乾燥C1阻害剤が2024年のシェア61.2%で引き続き市場をリードしています。これらの凍結乾燥製剤は保存期間が長く、冷蔵を必要としないため、信頼できるコールドチェーンインフラへのアクセスが限られている地域での使用に理想的です。この利点は、一貫した保存条件が困難な農村部のヘルスケア環境や低・中所得国において特に重要です。

米国市場は力強い成長を遂げています。2024年には7億2,940万米ドルと評価され、2034年には18億米ドルに達すると予測されています。この市場拡大の背景には、HAEの有病率の上昇、遺伝子スクリーニングの改善、早期診断に対する意識の高まり、希少疾患治療への幅広いアクセスがあります。米国FDAの希少疾病治療薬、特にHAEのような疾患に対する継続的な支援は、製品承認を加速させ、この分野での技術革新を促しています。

同市場の主要企業には、BioCryst Pharmaceuticals、武田薬品工業、KalVista、Ionis Pharmaceuticals、CSL Behring、Fresenius Kabi、Pharming、Pharvaris、Astriaなどがあります。これらの企業は、特に免疫学と炎症の分野において、C1阻害剤の新たな適応症を発見するために研究開発に多額の投資を行っています。戦略的提携もまた、製品パイプラインを拡大し、次世代治療を迅速に進めることで成長を後押ししています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 遺伝性血管性浮腫(HAE)および補体系疾患の有病率の上昇

- バイオテクノロジーと医薬品開発の進歩

- 有利な政府規制と償還政策

- 希少疾患の研究開発への投資増加

- 業界の潜在的リスク&課題

- C1インヒビター療法の高コスト

- 供給不足とサプライチェーンの制約

- 促進要因

- 成長可能性分析

- 規制情勢

- ギャップ分析

- 特許分析

- パイプライン分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021 –2034

- 主要動向

- 血漿由来C1インヒビター

- 選択的ブラジキニンB2受容体拮抗薬

- カリクレイン阻害剤

第6章 市場推計・予測:剤形別、2021 –2034

- 主要動向

- 凍結乾燥

- 注射剤

第7章 市場推計・予測:流通チャネル別、2021 –2034

- 主要動向

- 病院薬局

- 小売薬局

- eコマース

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Astria

- BioCryst Pharmaceuticals

- CSL Behring

- Fresenius Kabi

- Ionis Pharmaceuticals

- KalVista

- Pharming

- Pharvaris

- Takeda Pharmaceutical Company

The Global Plasma Protease C1-Inhibitor Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 4.5 billion by 2034. Plasma protease C1-inhibitors serve a vital role in controlling the activation of the complement and contact systems within the human body. These proteins, derived from blood plasma, are crucial in the treatment of rare genetic disorders such as Hereditary Angioedema (HAE). As healthcare systems continue to evolve, there is increasing awareness surrounding rare disease management, which is significantly contributing to the demand for effective and specialized therapies like C1-inhibitors.

Technological progress in plasma fractionation and collection methods is reshaping the landscape of biologics by enhancing the yield and purity of plasma-derived therapies. In turn, these developments are making treatments more accessible, affordable, and scalable for healthcare providers and patients alike. With growing clinical interest and the emergence of personalized medicine, the market is poised to witness greater penetration across new therapeutic applications, such as inflammatory and autoimmune diseases. Regulatory support and increasing healthcare infrastructure in both developed and emerging economies are further bolstering market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 9.7% |

In terms of drug classes, the plasma-derived C1-inhibitor segment dominated the market, accounting for 59.7% of the global share in 2024. While alternative options like selective bradykinin B2 receptor antagonists and Kallikrein inhibitors are also available, they currently serve as smaller segments within the market. Plasma-derived formulations remain the preferred option due to their established safety profiles and proven efficacy in managing acute and prophylactic treatment for HAE.

When looking at dosage forms, lyophilized C1-inhibitors continue to lead the market with a 61.2% share in 2024. These freeze-dried formulations are favored for their extended shelf life and do not require refrigeration, making them ideal for use in regions with limited access to reliable cold chain infrastructure. This advantage is particularly critical in rural healthcare settings and low-to-middle-income countries where consistent storage conditions can be a challenge.

The U.S. Plasma Protease C1-Inhibitor Market is experiencing robust growth. Valued at USD 729.4 million in 2024, it is projected to reach USD 1.8 billion by 2034. The expansion is driven by the rising prevalence of HAE, improvements in genetic screening, increased awareness of early diagnosis, and broader access to rare disease treatments. The U.S. FDA's continued support for orphan drugs, particularly for conditions like HAE, is accelerating product approvals and encouraging more innovation in this space.

Key players in the market include BioCryst Pharmaceuticals, Takeda Pharmaceutical Company, KalVista, Ionis Pharmaceuticals, CSL Behring, Fresenius Kabi, Pharming, Pharvaris, and Astria. These companies are heavily investing in R&D to discover new indications for C1-inhibitors, especially in the fields of immunology and inflammation. Strategic collaborations are also fueling growth by expanding product pipelines and fast-tracking next-generation therapies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of hereditary angioedema (HAE) and complement system disorders

- 3.2.1.2 Advancements in biotechnology and drug development

- 3.2.1.3 Favorable government regulations and reimbursement policies

- 3.2.1.4 Growing investment in rare disease research and development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of C1-inhibitor therapies

- 3.2.2.2 Limited availability and supply chain constraints

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Plasma-derived C1-inhibitor

- 5.3 Selective bradykinin B2 receptor antagonist

- 5.4 Kallikrein inhibitor

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Lyophilized

- 6.3 Injectables

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Astria

- 9.2 BioCryst Pharmaceuticals

- 9.3 CSL Behring

- 9.4 Fresenius Kabi

- 9.5 Ionis Pharmaceuticals

- 9.6 KalVista

- 9.7 Pharming

- 9.8 Pharvaris

- 9.9 Takeda Pharmaceutical Company