|

市場調査レポート

商品コード

1721456

心血管治療薬の市場機会と促進要因、業界動向分析、2025年~2034年予測Cardiovascular Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 心血管治療薬の市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年04月02日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

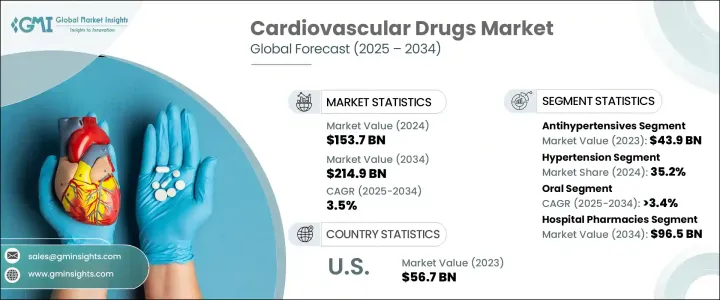

世界の心血管治療薬市場は、2024年に1,537億米ドルと評価され、CAGR 3.5%で成長し、2034年には2,149億米ドルに達すると予測されています。

心血管疾患の世界の負担が増加し続ける中、効果的で利用しやすい治療オプションに対する需要はかつてないペースで高まっています。世界中のヘルスケアシステムは、冠動脈疾患、心不全、不整脈、高血圧などの疾患を管理しなければならないという大きなプレッシャーにさらされています。心血管系の健康に対する意識の高まり、診断率の上昇、予防医療への取り組みの急増は、市場の成長に大きく寄与しています。加えて、運動不足、食生活の乱れ、ストレス、喫煙、飲酒といった生活習慣に関連する危険因子が、継続的な薬剤介入の必要性を高めています。

特に先進国では世界人口の高齢化が進んでおり、高齢者は慢性的な心臓病を発症しやすいため、心血管治療薬の必要性がさらに高まっています。技術革新の面では、ドラッグデリバリー技術の進歩や次世代治療法の導入により、治療効果と患者のコンプライアンスが向上しています。主な企業は研究開発に多額の投資を行い、より良い治療効果、副作用の軽減、さまざまな患者のニーズに合った治療を提供する医薬品を発売しています。個別化医療への傾倒の高まりも心血管治療の展望を変えつつあり、企業はより的を絞った治療を通じて、これまで満たされていなかった医療ニーズに対応できるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,537億米ドル |

| 予測金額 | 2,149億米ドル |

| CAGR | 3.5% |

市場は抗高血圧薬、抗高脂血症薬、抗凝固薬、抗不整脈薬、その他の治療薬などの薬剤クラス別に区分されます。このうち、高血圧治療薬部門は、世界の高血圧の有病率の上昇を背景に、2023年に439億米ドルを稼ぎ出しました。この薬剤クラス別には、ACE阻害薬、アンジオテンシンII受容体拮抗薬(ARB)、β遮断薬、カルシウム拮抗薬、利尿薬などが含まれ、いずれも血圧を下げ、重篤な心血管合併症のリスクを最小限に抑えるために不可欠と考えられています。高血圧分野は、世界の高血圧罹患率の増加と、脳卒中、腎不全、心臓発作などの生命を脅かす疾患との直接的な関連に牽引され、2024年には35.2%のシェアを占めました。高血圧を効果的に治療することは、医療提供者にとって依然として最優先事項であり、単剤療法と合剤療法の両方が利用可能であるため、個々のニーズに合わせて治療をカスタマイズすることができます。

北米は2024年に世界の心血管治療薬市場の41.2%のシェアを占め、2034年までのCAGRは3.2%と予測されています。同地域は、強力なヘルスケアインフラ、高い一人当たり医療費、大手製薬企業の存在などの恩恵を受けています。さらに、米国では心血管疾患の罹患率が上昇し、高齢化が急速に進んでいるため、先進的な治療法に対する需要が高まっています。ヘルスケアの革新と治療へのアクセスを促進する政府主導のイニシアチブは、地域市場の拡大をさらに後押しすると予想されます。

世界の心血管治療薬市場で事業を展開する主要企業には、ファイザー、ジョンソン・エンド・ジョンソン、ブリストル・マイヤーズスクイブ、ギリアド・サイエンシズ、バイエル、メルク、アムジェン、サノフィ、ノバルティス、アストラゼネカ、ルパン、ヴィアトリスなどがあります。これらの企業は、新薬クラスや次世代治療薬で積極的にポートフォリオを拡大しており、戦略的提携や研究開発への投資が競争優位性を維持し続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患の有病率の増加

- 医薬品製剤における技術の進歩

- 予防ヘルスケアへの意識の高まり

- 業界の潜在的リスク&課題

- 厳格な規制枠組み

- 医薬品開発の高コスト

- 促進要因

- 成長可能性分析

- 規制情勢

- 将来の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021-2034

- 主要動向

- 降圧剤

- 抗高脂血症薬

- 抗凝固薬

- 抗不整脈薬

- その他の薬物クラス

第6章 市場推計・予測:適応症別、2021-2034

- 主要動向

- 高血圧

- 高脂血症

- 冠動脈疾患

- 不整脈

- その他の適応症

第7章 市場推計・予測:投与経路別、2021-2034

- 主要動向

- オーラル

- 非経口

- その他の投与経路

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 病院薬局

- オンライン薬局

- 小売薬局

- その他の流通チャネル

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amgen

- AstraZeneca

- Baxter

- Bayer

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Gilead Sciences

- Johnson &Johnson

- Lupin

- Merck

- Novartis

- Pfizer

- Sanofi

- Viatris

The Global Cardiovascular Drugs Market was valued at USD 153.7 billion in 2024 and is projected to grow at a CAGR of 3.5% to reach USD 214.9 billion by 2034. As the global burden of cardiovascular diseases continues to rise, the demand for effective and accessible treatment options is growing at an unprecedented pace. Healthcare systems around the world are under immense pressure to manage conditions such as coronary artery disease, heart failure, arrhythmias, and hypertension, which remain the leading causes of mortality across all regions. Increasing awareness of cardiovascular health, growing diagnosis rates, and a surge in preventive care initiatives are contributing significantly to market growth. In addition, lifestyle-related risk factors like physical inactivity, poor dietary habits, stress, smoking, and alcohol consumption are amplifying the need for ongoing pharmaceutical intervention.

The aging global population, particularly in developed nations, is further fueling the need for cardiovascular drugs as elderly individuals are more prone to developing chronic heart-related ailments. On the innovation front, advancements in drug delivery technologies and the introduction of next-generation treatment modalities are enhancing both therapeutic efficacy and patient compliance. Key players are investing heavily in research and development to launch drugs that offer better outcomes, reduced side effects, and tailored treatments suited for a variety of patient needs. The growing inclination toward personalized medicine is also reshaping the cardiovascular treatment landscape, allowing companies to address previously unmet medical needs through more targeted therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $153.7 Billion |

| Forecast Value | $214.9 Billion |

| CAGR | 3.5% |

The market is segmented based on drug classes such as antihypertensives, antihyperlipidemic agents, anticoagulants, antiarrhythmics, and other therapies. Among these, the antihypertensives segment alone generated USD 43.9 billion in 2023, fueled by the increasing prevalence of high blood pressure worldwide. This drug class includes ACE inhibitors, angiotensin II receptor blockers (ARBs), beta-blockers, calcium channel blockers, and diuretics-all considered essential in lowering blood pressure and minimizing the risk of severe cardiovascular complications. The hypertension segment accounted for a 35.2% share in 2024, driven by the growing global incidence of high blood pressure and its direct link to life-threatening conditions such as strokes, kidney failure, and heart attacks. Managing hypertension effectively remains a top priority for healthcare providers, and the availability of both monotherapies and fixed-dose combination therapies ensures treatment can be customized to individual needs.

North America held a 41.2% share of the global cardiovascular drugs market in 2024 and is projected to grow at a 3.2% CAGR through 2034. The region benefits from strong healthcare infrastructure, high per capita health expenditure, and the presence of leading pharmaceutical firms. Additionally, the rising incidence of cardiovascular conditions and a rapidly aging population in the U.S. are boosting demand for advanced therapies. Government-driven initiatives promoting healthcare innovation and treatment accessibility are expected to further support regional market expansion.

Key players operating in the Global Cardiovascular Drugs Market include Pfizer, Johnson & Johnson, Bristol-Myers Squibb, Gilead Sciences, Bayer, Merck, Amgen, Sanofi, Novartis, AstraZeneca, Lupin, and Viatris. These companies are actively expanding their portfolios with novel drug classes and next-gen therapies, while strategic collaborations and investments in R&D continue to drive competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cardiovascular diseases

- 3.2.1.2 Technological advancements in drug formulation

- 3.2.1.3 Growing awareness of preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory frameworks

- 3.2.2.2 High costs of drug development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antihypertensives

- 5.3 Antihyperlipidemic

- 5.4 Anticoagulants

- 5.5 Antiarrhythmics

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hypertension

- 6.3 Hyperlipidemia

- 6.4 Coronary artery disease

- 6.5 Arrhythmia

- 6.6 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

- 7.4 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Online pharmacies

- 8.4 Retail pharmacies

- 8.5 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amgen

- 10.2 AstraZeneca

- 10.3 Baxter

- 10.4 Bayer

- 10.5 Boehringer Ingelheim

- 10.6 Bristol-Myers Squibb

- 10.7 Gilead Sciences

- 10.8 Johnson & Johnson

- 10.9 Lupin

- 10.10 Merck

- 10.11 Novartis

- 10.12 Pfizer

- 10.13 Sanofi

- 10.14 Viatris