PEG化タンパク質の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

PEGylated Proteins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721446

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

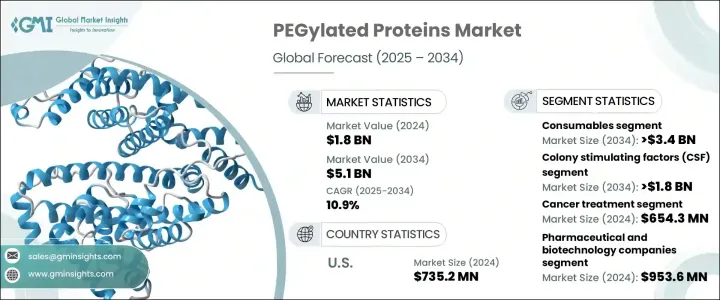

世界のPEG化タンパク質市場は、2024年には18億米ドルと評価され、CAGR 10.9%で成長し、2034年には51億米ドルに達すると推定されています。

この顕著な成長傾向は、現代医療におけるタンパク質ベースの治療薬の使用拡大を反映しています。生物製剤やバイオシミラーが世界の医薬品分野で着実に普及する中、PEG化技術の役割はますます不可欠になっています。このプロセスは、タンパク質や薬剤をポリエチレングリコール(PEG)で化学修飾し、安定性、溶解性、半減期を向上させるものです。これらの利点から、PEG化はドラッグデリバリー、特にモノクローナル抗体や組換えタンパク質のような複雑な生物学的製剤に不可欠なツールとなっています。

標的治療薬の開発に向けた研究開発が強化される中、PEG化製剤は薬物動態の改善と免疫原性の低減により、好ましい選択肢として浮上しています。生物製剤開発に対する政府支援の増加とタンパク質治療薬の臨床試験件数の増加が相まって、この分野の技術革新の限界は押し上げられ続けています。がん、自己免疫疾患、糖尿病など、慢性的で生命を脅かす疾患の増加により、より安全で長時間作用する治療オプションの必要性が著しく高まっており、市場の拡大をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 18億米ドル |

| 予測金額 | 51億米ドル |

| CAGR | 10.9% |

市場は消耗品とサービスに大別されます。消耗品分野は、特殊なPEG誘導体の需要が高まるにつれて、予測期間中にCAGR 10.9%の安定した伸びが見込まれます。これらの誘導体は、モノクローナル抗体や酵素のようなPEG化生物製剤の性能を高める鍵となります。慢性疾患の罹患率が世界的に上昇傾向にある中、有効性の持続する高度な治療薬が求められており、高級PEG試薬やポリマーへの依存度が高まっています。患者のコンプライアンスと治療効率を向上させるドラッグデリバリーシステムが重視されていることも、このカテゴリーの成長を後押ししています。

タンパク質の種類別に見ると、インターフェロン、コロニー刺激因子(CSF)、エリスロポエチン、抗体、遺伝子組換え第VIII因子、その他のタンパク質が含まれます。CSF分野は、主に貧血や白血病などの血液疾患の有病率の増加により、2025年から2034年にかけてCAGR 11%で成長すると予測されています。CSFは、化学療法やその他の集中治療を受けている患者の骨髄回復をサポートし、免疫機能を高める上で重要な役割を果たしています。CSFの用途は、幹細胞動員や慢性好中球減少症のような新しい治療分野にも広がっています。

米国のPEG化タンパク質市場は2024年に7億3,520万米ドルに達し、慢性疾患の罹患率の高さと高度なヘルスケア・インフラの存在により、大幅な成長が見込まれています。製薬企業の集積とPEG化技術における継続的な技術革新が、米国が圧倒的な市場ポジションを維持するのに役立っています。

世界市場の主要企業には、Biopharma PEG Scientific、Merck KGaA、Celares、Abcam、Biomatrik、Enzon Pharmaceuticals、JenKem Technology、Aurigene Pharmaceutical Services、Quanta BioDesign、Thermo Fisher Scientific、Laysan Bio、Iris Biotech、Profacgen、Creative PEGworks、NOF Corporationなどがあります。これらの企業は、研究開発投資、ポートフォリオの拡大、買収、共同戦略を通じて、治療効果と世界市場での存在感を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の上昇

- ドラッグデリバリーにおけるPEG化の利点

- 成長するバイオ医薬品およびバイオテクノロジー産業

- PEG化薬剤の採用増加

- 業界の潜在的リスク&課題

- PEG化とタンパク質ベースの薬剤の高コスト

- 規制上の課題と厳格な承認プロセス

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 消耗品

- サービス

第6章 市場推計・予測:タンパク質の種類別、2021-2034

- 主要動向

- コロニー刺激因子

- インターフェロン

- エリスロポエチン

- 組換え第VIII因子

- 抗体

- その他のタンパク質の種類

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- がん治療

- 自己免疫疾患

- 血液疾患

- 肝炎

- 慢性腎臓病

- 胃腸障害

- その他の用途

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 製薬およびバイオテクノロジー企業

- CROとCMO

- 学術研究機関

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abcam

- Aurigene Pharmaceutical Services

- Biomatrik

- Biopharma PEG Scientific

- Celares

- Creative PEGworks

- Enzon Pharmaceuticals

- Iris Biotech

- JenKem Technology

- Laysan Bio

- Merck KGaA

- NOF Corporation

- Profacgen

- Quanta BioDesign

- Thermo Fisher Scientific

目次

The Global Pegylated Proteins Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 10.9% to reach USD 5.1 billion by 2034. This notable growth trend reflects the expanding use of protein-based therapeutics in modern medicine. With biologics and biosimilars steadily gaining traction in the global pharmaceutical space, the role of PEGylation technology is becoming increasingly indispensable. This process involves the chemical modification of proteins or drugs with polyethylene glycol (PEG), enhancing their stability, solubility, and half-life. These benefits make PEGylation an essential tool in drug delivery, especially for complex biologics like monoclonal antibodies and recombinant proteins.

As research efforts intensify to develop targeted therapies, PEGylated formulations are emerging as a preferred choice due to their improved pharmacokinetics and reduced immunogenicity. Increasing government support for biologics development, combined with a higher volume of clinical trials in protein therapeutics, continues to push the boundaries of innovation within this sector. The growing incidence of chronic and life-threatening diseases, including cancer, autoimmune disorders, and diabetes, has significantly escalated the need for safer, long-acting treatment options-further reinforcing market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 10.9% |

The market is broadly segmented into consumables and services. The consumables segment is poised to witness a steady CAGR of 10.9% during the forecast period as the demand for specialized PEG derivatives rises. These derivatives are key to enhancing the performance of PEGylated biologics, such as monoclonal antibodies and enzymes. With chronic disease rates on the rise globally, the requirement for advanced therapeutics that offer prolonged efficacy is prompting greater reliance on premium-grade PEG reagents and polymers. The emphasis on drug delivery systems that provide better patient compliance and therapeutic efficiency is also bolstering growth within this category.

Based on protein type, the PEGylated proteins market includes interferons, colony-stimulating factors (CSF), erythropoietin, antibodies, recombinant factor VIII, and other protein categories. The CSF segment is projected to grow at a CAGR of 11% from 2025 to 2034, primarily due to the increasing prevalence of hematological disorders such as anemia and leukemia. CSFs play a critical role in supporting bone marrow recovery and enhancing immune function in patients undergoing chemotherapy and other intensive treatments. Their applications are also expanding into newer therapeutic areas like stem cell mobilization and chronic neutropenia.

The U.S. PEGylated Proteins Market reached USD 735.2 million in 2024 and is expected to grow substantially, driven by the high incidence of chronic illnesses and the presence of advanced healthcare infrastructure. A strong concentration of pharmaceutical companies and ongoing innovation in PEGylation technologies are helping the U.S. maintain a dominant market position.

Key players in the global market include Biopharma PEG Scientific, Merck KGaA, Celares, Abcam, Biomatrik, Enzon Pharmaceuticals, JenKem Technology, Aurigene Pharmaceutical Services, Quanta BioDesign, Thermo Fisher Scientific, Laysan Bio, Iris Biotech, Profacgen, Creative PEGworks, and NOF Corporation. These companies are advancing through R&D investments, portfolio expansion, acquisitions, and collaborative strategies to enhance therapeutic efficacy and global market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Advantages of PEGylation in drug delivery

- 3.2.1.3 Growing biopharmaceutical and biotechnology industry

- 3.2.1.4 Increasing adoption of PEGylated drugs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of PEGylation and protein-based drugs

- 3.2.2.2 Regulatory challenges and stringent approval processes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Services

Chapter 6 Market Estimates and Forecast, By Protein Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Colony stimulating factors

- 6.3 Interferons

- 6.4 Erythropoietin

- 6.5 Recombinant factor VIII

- 6.6 Antibodies

- 6.7 Other protein types

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cancer treatment

- 7.3 Autoimmune diseases

- 7.4 Hematological disorders

- 7.5 Hepatitis

- 7.6 Chronic kidney diseases

- 7.7 Gastrointestinal disorders

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 CROs and CMOs

- 8.4 Academic and research institutes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abcam

- 10.2 Aurigene Pharmaceutical Services

- 10.3 Biomatrik

- 10.4 Biopharma PEG Scientific

- 10.5 Celares

- 10.6 Creative PEGworks

- 10.7 Enzon Pharmaceuticals

- 10.8 Iris Biotech

- 10.9 JenKem Technology

- 10.10 Laysan Bio

- 10.11 Merck KGaA

- 10.12 NOF Corporation

- 10.13 Profacgen

- 10.14 Quanta BioDesign

- 10.15 Thermo Fisher Scientific

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日