|

市場調査レポート

商品コード

1721442

MEMSセンサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測MEMS Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| MEMSセンサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月03日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

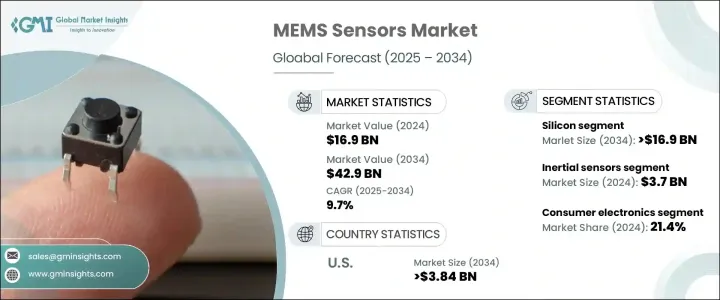

MEMSセンサーの世界市場規模は2024年に169億米ドルとなり、CAGR 9.7%で成長し、2034年には429億米ドルに達すると予測されています。

同市場は、各業界でコネクテッド・テクノロジーの採用が加速していることを背景に、力強い勢いを見せています。次世代スマートフォンやスマートウォッチから、自律走行車や産業用オートメーションシステムまで、インテリジェントで小型化されたセンサーの需要はかつてないほど高まっています。MEMS(微小電気機械システム)センサーは、低消費電力とコンパクトなフォームファクターを維持しながら、正確なデータを収集する能力で脚光を浴びています。

よりスマートで応答性の高いデバイスに対する消費者の期待が高まり続ける中、メーカーはMEMS技術を統合してユーザー体験を向上させ、リアルタイムの分析を可能にしています。さらに、インダストリー4.0の急速な進化、電気自動車への投資の増加、モノのインターネット(IoT)エコシステムの拡大により、技術インフラの再構築におけるMEMSセンサーの役割が強化されています。また、世界のOEMは、デバイスの効率を高め、コンポーネントの冗長性を最小限に抑えるため、多機能センサーの統合に注力しており、市場の成長をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 169億米ドル |

| 予測金額 | 429億米ドル |

| CAGR | 9.7% |

MEMSセンサーは、民生用電子機器と自動車用アプリケーションの両方で、ますます重要な役割を果たしています。自動車分野では、ADAS(先進運転支援システム)や安全技術への需要の高まりが、MEMSセンサーの統合に拍車をかけています。これらのシステムは正確でリアルタイムのデータに依存しており、MEMSセンサーは自動車の安全性に関する世界の規制が強化される中、正確性と応答性を保証します。エレクトロニクス分野では、MEMSセンサーがジェスチャー認識、モーショントラッキング、環境モニタリングなどの機能を実現することで、デバイスのパフォーマンスを向上させ、インテリジェントで多機能なガジェットに対する消費者の期待に応えます。

MEMSセンサーの製造に使用される材料には、シリコン、ポリマー、セラミック、金属などがあります。このうち、シリコンは引き続き優位を占めており、2034年までに169億米ドルを生み出すと予測されています。シリコンは、その優れた機械的・熱的安定性と共にCMOS製造プロセスとの互換性により、高性能アプリケーションで好まれる材料となっています。シリコンの採用は、軽量で耐久性のあるコンポーネントの需要が高まるにつれて、ヘルスケア、ウェアラブル、家電で急速に拡大しています。

市場は、慣性センサー、圧力センサー、マイクロフォン、環境センサー、光学センサー、超音波センサーなど、センサーの種類によって区分されます。慣性センサだけでも2024年には37億米ドルを占め、その用途は産業オートメーション、ロボット工学、ドローン、自動運転車を含む自動車システムに及ぶ。これらのセンサーは、動き検出、方向、安定化に不可欠であり、新たなスマート技術にとって重要な要件です。

米国のMEMSセンサー市場は上昇基調にあり、2034年には38億4,000万米ドルに達すると予測されています。米国の成長は、航空宇宙、防衛、ヘルスケア、自律システムなどにおける展開の増加に起因しています。AI、ロボット工学、医療技術革新の進展が需要をさらに強化しています。Robert Bosch GmbH、STMicroelectronics、Broadcom Inc.、Texas Instruments、Qorvo Inc.などの大手企業は、製品ラインの拡大、研究開発の推進、戦略的提携の形成に注力し、世界市場での存在感を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 家電製品の需要増加

- 自動車用途の進歩

- 産業オートメーションとIoTの拡大

- ヘルスケアおよびバイオメディカルアプリケーションの成長

- 小型化とエネルギー効率の革新

- 業界の潜在的リスク&課題

- 製造の複雑さとコストが高め

- 統合と標準化の課題

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:センサータイプ別、2021-2034

- 慣性センサー

- 圧力センサー

- マイク

- 環境センサー

- 光学センサー

- 超音波センサー

- その他

第6章 市場推計・予測:材料別、2021-2034

- シリコン

- ポリマー

- セラミックス

- 金属材料

第7章 市場推計・予測:最終用途別、2021-2034

- 家電

- 自動車

- ヘルスケア

- 産業

- 航空宇宙および防衛

- 通信

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Robert Bosch GmbH

- STMicroelectronics

- Broadcom Inc.

- Texas Instruments

- Qorvo Inc.

- Goertek Inc.

- Hewlett Packard Enterprise Development LP

- TDK Corporation

- Knowles Electronics LLC

- Infineon Technologies AG

- Honeywell International

- Analog Devices Inc.

- Murata Manufacturing Co. Ltd.

- Teledyne DALSA

- Sony Semiconductor

- X-FAB Silicon Foundries

- Tower Semiconductor

- TSMC(Taiwan Semiconductor Manufacturing Company)

- United Microelectronics Corporation(UMC)

- Safran Sensing Technologies Norway AS

- MEMS Engineering Limited

- Redbud Labs

- USound

- Windfall Bio

- ZERO POINT MOTION LTD.

The Global MEMS Sensors Market was valued at USD 16.9 billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 42.9 billion by 2034. The market is witnessing robust momentum, driven by the accelerating adoption of connected technologies across industries. From next-gen smartphones and smartwatches to autonomous vehicles and industrial automation systems, the demand for intelligent, miniaturized sensors has never been higher. MEMS (Micro-Electro-Mechanical Systems) sensors are gaining prominence for their ability to collect precise data while maintaining low power consumption and compact form factors.

As consumer expectations for smarter, more responsive devices continue to rise, manufacturers are integrating MEMS technology to elevate user experiences and enable real-time analytics. Additionally, the rapid evolution of Industry 4.0, growing investments in electric vehicles, and the expanding footprint of the Internet of Things (IoT) ecosystem are reinforcing the role of MEMS sensors in reshaping technological infrastructures. Global OEMs are also focusing on multi-functional sensor integration to enhance device efficiency and minimize component redundancy, further boosting market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.9 Billion |

| Forecast Value | $42.9 Billion |

| CAGR | 9.7% |

MEMS sensors play an increasingly critical role in both consumer electronics and automotive applications. In the automotive sector, the growing demand for advanced driver-assistance systems (ADAS) and safety technologies is fueling the integration of MEMS sensors. These systems rely on precise and real-time data, and MEMS sensors ensure accuracy and responsiveness as global regulations around automotive safety tighten. In electronics, MEMS sensors enhance device performance by enabling features like gesture recognition, motion tracking, and environmental monitoring, thus aligning with consumer expectations for intelligent, multifunctional gadgets.

The materials used in manufacturing MEMS sensors include silicon, polymers, ceramics, and metals. Among these, silicon continues to dominate, with the segment projected to generate USD 16.9 billion by 2034. Silicon's compatibility with CMOS fabrication processes, along with its superior mechanical and thermal stability, makes it a preferred material across high-performance applications. Its adoption is expanding rapidly in healthcare, wearables, and consumer electronics as demand for lightweight, durable components increases.

The market is segmented by sensor types such as inertial sensors, pressure sensors, microphones, environmental sensors, optical sensors, and ultrasonic sensors. Inertial sensors alone accounted for USD 3.7 billion in 2024, with applications spanning industrial automation, robotics, drones, and automotive systems, including self-driving vehicles. These sensors are vital for motion detection, orientation, and stabilization, key requirements for emerging smart technologies.

The U.S. MEMS sensors market is on an upward trajectory, projected to reach USD 3.84 billion by 2034. Growth in the U.S. is attributed to increasing deployment across aerospace, defense, healthcare, and autonomous systems. Progress in AI, robotics, and medical innovations further reinforces demand. Leading players such as Robert Bosch GmbH, STMicroelectronics, Broadcom Inc., Texas Instruments, and Qorvo Inc. are focusing on expanding product lines, advancing R&D, and forming strategic alliances to strengthen their global market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for consumer electronics

- 3.2.1.2 Advancements in automotive applications

- 3.2.1.3 Expansion of industrial automation and iot

- 3.2.1.4 Growth in healthcare and biomedical applications

- 3.2.1.5 Miniaturization and energy efficiency innovations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing complexity and costs

- 3.2.2.2 Integration and standardization challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Sensor Type, 2021 - 2034 (USD Million and Units)

- 5.1 Inertial sensors

- 5.2 Pressure sensors

- 5.3 Microphones

- 5.4 Environmental sensors

- 5.5 Optical sensors

- 5.6 Ultrasonic sensors

- 5.7 Others

Chapter 6 Market estimates & forecast, By Material, 2021 - 2034 (USD Million and Units)

- 6.1 Silicon

- 6.2 Polymers

- 6.3 Ceramics

- 6.4 Metallic materials

Chapter 7 Market estimates & forecast, By End Use, 2021 - 2034 (USD Million and Units)

- 7.1 Consumer electronics

- 7.2 Automotive

- 7.3 Healthcare

- 7.4 Industrial

- 7.5 Aerospace & defense

- 7.6 Telecommunications

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million and Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Robert Bosch GmbH

- 9.2 STMicroelectronics

- 9.3 Broadcom Inc.

- 9.4 Texas Instruments

- 9.5 Qorvo Inc.

- 9.6 Goertek Inc.

- 9.7 Hewlett Packard Enterprise Development LP

- 9.8 TDK Corporation

- 9.9 Knowles Electronics LLC

- 9.10 Infineon Technologies AG

- 9.11 Honeywell International

- 9.12 Analog Devices Inc.

- 9.13 Murata Manufacturing Co. Ltd.

- 9.14 Teledyne DALSA

- 9.15 Sony Semiconductor

- 9.16 X-FAB Silicon Foundries

- 9.17 Tower Semiconductor

- 9.18 TSMC (Taiwan Semiconductor Manufacturing Company)

- 9.19 United Microelectronics Corporation (UMC)

- 9.20 Safran Sensing Technologies Norway AS

- 9.21 MEMS Engineering Limited

- 9.22 Redbud Labs

- 9.23 USound

- 9.24 Windfall Bio

- 9.25 ZERO POINT MOTION LTD.