|

市場調査レポート

商品コード

1721441

獣医心臓病学の市場機会と促進要因、業界動向分析、2025年~2034年予測Veterinary Cardiology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 獣医心臓病学の市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年04月01日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

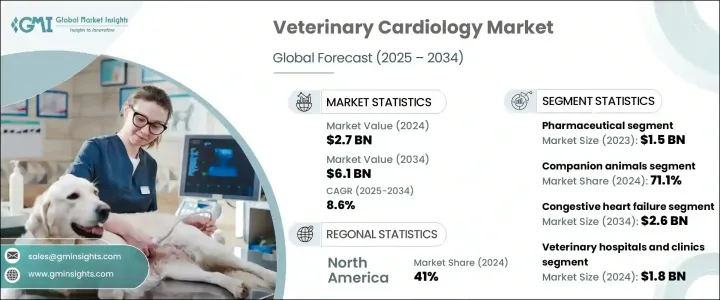

世界の獣医心臓病学市場は、2024年には27億米ドルと評価され、CAGR 8.6%で成長し、2034年には61億米ドルに達すると推定されています。

ペット飼育の増加と動物の健康に対する意識の高まりが、この拡大に極めて重要な役割を果たしています。ペットがますます不可欠な家族の一員となるにつれ、飼い主は心血管系疾患などの慢性疾患に対してタイムリーで専門的な治療を積極的に求めるようになっています。獣医師は、特に高齢化した犬や猫の心臓関連の症例が顕著に急増していることを目の当たりにしており、心臓病学サービスに対する投資の増加を促しています。

さらに、ペット保険の適用範囲が徐々に拡大し、高度な診断検査や治療が含まれるようになり、飼い主が専門的な治療を選択する傾向がさらに強まっています。市場はまた、獣医専門家の存在感の増大、動物ヘルスケアにおけるインフラの拡大、コンパニオンアニマルの心臓病学的転帰の改善を目指した研究開発投資の増加によって勢いを増しています。獣医学とテクノロジーの融合により、この業界は、動物の心臓疾患の診断、モニター、治療方法を再定義する急速な変革期を迎えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 27億米ドル |

| 予測金額 | 61億米ドル |

| CAGR | 8.6% |

この成長の原動力となっているのは、心臓病を患うペットの増加と診断・治療法の進歩です。バルーン弁形成術やペースメーカー植え込み術などの低侵襲手術は、リスクの軽減と回復時間の短縮により人気を集めています。ピモベンダン、ACE阻害薬、β遮断薬などの新しい薬も、心臓病と診断されたペットの寿命を延ばすのに役立っています。

市場は医薬品と診断薬に分けられます。医薬品セグメントは、2023年に15億米ドルを生み出しました。この顕著な実績は主に、治療プロトコルの継続的な革新とシニアペットにおける心血管疾患の発生率の増加に起因します。動物の心臓機能を調整し、体液の蓄積を管理し、血圧をコントロールできる医薬品に対する需要が高まっており、この分野への投資と製品開発が増加しています。

獣医心臓病学市場のコンパニオンアニマル・セグメントは、2024年に71.1%のシェアを占めました。犬、猫、その他の家庭用ペットを含むこのカテゴリーは、飼育率の上昇と、ペットが高齢になるにつれて心臓の問題を発症する可能性が高くなることから、引き続き優位を占めています。今日、ペットの飼い主は病気の早期発見をより強く意識するようになり、専門的な心臓病学サービスを求めるようになっています。心エコー図や心電図(ECG)などの高度な診断の需要が高まっています。

北米獣医心臓病学 2024年のシェアは41%。この地域の優位性は、コンパニオンアニマルの人口の多さ、診断ツールの進歩、専門動物病院の拡大によって支えられています。特に米国市場では、人工知能とウェアラブル心臓モニターの統合が進んでおり、ペットの心臓の健康状態をモニターする方法が変わりつつあります。

獣医心臓病学市場に参入している主な企業は、TriviumVet、ESAOTE、Bionet America、Medtronic、Jurox、Siemens Healthineers、富士フイルム、Zoetis、Antech Diagnostics、General Electric Company、IDEXX、Merck、Boehringer Ingelheim International、Ceva、GSKなどです。各社は革新的な製品開発に注力しており、心エコーやカテーテルを用いた治療法などの先進的な診断ツールを導入しています。動物病院、調査機関、ハイテク企業との戦略的提携は、世界市場でのリーチと影響力の拡大に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ペットの飼育数の増加と動物ヘルスケア費の増加

- 獣医心臓病学診断および治療技術の進歩

- ペットにおける心血管疾患の罹患率の増加

- 業界の潜在的リスク&課題

- 高度な獣医心臓病学治療と機器の高コスト

- 専門の獣医心臓専門医の数が限られている

- 促進要因

- 成長可能性分析

- 規制情勢

- 将来の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 医薬品

- ピモベンダン

- スピロノラクトンと塩酸ベナゼプリル

- その他の医薬品

- 診断

- 身体検査

- 胸部X線検査

- 心電図(ECG)

- その他の診断

第6章 市場推計・予測:動物の種類別、2021-2034

- 主要動向

- コンパニオンアニマル

- 犬

- 猫

- その他のペット

- 家畜

- 牛

- 家禽

- その他の家畜

第7章 市場推計・予測:適応症別、2021-2034

- 主要動向

- うっ血性心不全

- 心筋疾患

- 不整脈

- その他の適応症

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 動物病院および診療所

- 学術調査機関

- その他のエンドユーザー

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Antech Diagnostics

- Boehringer Ingelheim International

- Jurox

- Ceva

- Merck

- IDEXX

- General Electric Company

- FUJIFILM

- ESAOTE

- Medtronic

- Siemens Healthineers

- TriviumVet

- Zoetis

- Bionet America

The Global Veterinary Cardiology Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 6.1 billion by 2034. The rise in pet ownership and heightened awareness of animal health are playing a pivotal role in this expansion. As pets increasingly become integral family members, owners are more proactive in seeking timely and specialized care for chronic conditions, including cardiovascular diseases. Veterinarians are witnessing a notable surge in heart-related cases, especially among aging dogs and cats, prompting increased investments in cardiology services.

Moreover, pet insurance coverage is gradually expanding to include advanced diagnostic tests and treatments, which is further encouraging owners to opt for specialized care. The market is also gaining momentum with the growing presence of veterinary specialists, expanding infrastructure in animal healthcare, and rising R&D investments aimed at improving cardiology outcomes in companion animals. With the convergence of veterinary medicine and technology, the industry is undergoing a rapid transformation that is redefining how heart conditions in animals are diagnosed, monitored, and treated.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 8.6% |

This growth is driven by a rising number of pets with heart disease and advancements in diagnostic and treatment methods. Minimally invasive procedures, such as balloon valvuloplasty and pacemaker implantation, are gaining popularity due to reduced risks and quicker recovery times. Newer medications like pimobendan, ACE inhibitors, and beta-blockers are also helping extend the lifespan of pets diagnosed with heart conditions.

The market is divided into pharmaceuticals and diagnostics. The pharmaceuticals segment generated USD 1.5 billion in 2023. This notable performance is mainly attributed to ongoing innovation in treatment protocols and a growing incidence of cardiovascular conditions in senior pets. There is a rising demand for medications that can regulate heart function, manage fluid buildup, and control blood pressure in animals, leading to increased investments and product development in this space.

The companion animal segment in the veterinary cardiology market held a 71.1% share in 2024. This category, which includes dogs, cats, and other domestic pets, continues to dominate due to increasing adoption rates and the higher likelihood of pets developing heart issues as they age. Pet owners today are far more conscious about the early detection of diseases, prompting them to pursue specialized cardiology services. Advanced diagnostics such as echocardiograms and electrocardiograms (ECGs) are seeing growing demand.

North America Veterinary Cardiology Market held a 41% share in 2024. The region's dominance is supported by a large population of companion animals, advancements in diagnostic tools, and the expansion of specialty veterinary hospitals. The U.S. market, in particular, is seeing growing integration of artificial intelligence and wearable heart monitors, which are changing how cardiac health is monitored in pets.

Major players involved in the veterinary cardiology market include TriviumVet, ESAOTE, Bionet America, Medtronic, Jurox, Siemens Healthineers, Fujifilm, Zoetis, Antech Diagnostics, General Electric Company, IDEXX, Merck, Boehringer Ingelheim International, Ceva, and GSK among others. Companies are focusing on innovative product development, introducing advanced diagnostic tools like echocardiograms and catheter-based therapies. Strategic collaborations with veterinary clinics, research bodies, and tech firms are helping them expand their reach and influence across global markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet adoption and increasing expenditure on animal healthcare

- 3.2.1.2 Advancements in veterinary cardiology diagnostics and treatment technologies

- 3.2.1.3 Increasing prevalence of cardiovascular diseases in companion animals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced veterinary cardiology treatments and devices

- 3.2.2.2 Limited availability of specialized veterinary cardiologists

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmaceuticals

- 5.2.1 Pimobendan

- 5.2.2 Spironolactone and benazepril hydrochloride

- 5.2.3 Other pharmaceuticals

- 5.3 Diagnostics

- 5.3.1 Physical exam

- 5.3.2 Chest X-rays

- 5.3.3 Electrocardiogram (ECG)

- 5.3.4 Other diagnostics

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Other companion animals

- 6.3 Livestock animals

- 6.3.1 Cattle

- 6.3.2 Poultry

- 6.3.3 Other livestock animals

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Congestive heart failure

- 7.3 Myocardial (heart muscle) disease

- 7.4 Arrhythmias

- 7.5 Other indications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 Academic and research institutions

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Antech Diagnostics

- 10.2 Boehringer Ingelheim International

- 10.3 Jurox

- 10.4 Ceva

- 10.5 Merck

- 10.6 IDEXX

- 10.7 General Electric Company

- 10.8 FUJIFILM

- 10.9 ESAOTE

- 10.10 Medtronic

- 10.11 Siemens Healthineers

- 10.12 TriviumVet

- 10.13 Zoetis

- 10.14 Bionet America