BOPPフィルム市場機会と促進要因、市場促進要因、産業動向分析、2025年~2034年予測

BOPP Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721438

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

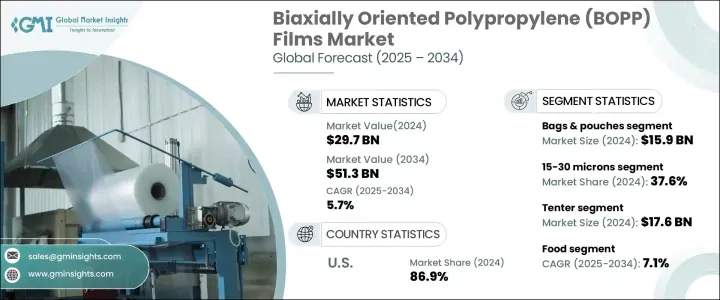

BOPPフィルムの世界市場は、2024年には297億米ドルとなり、CAGR 5.7%で成長し、2034年には513億米ドルに達すると予測されています。

包装用途におけるBOPPフィルムの優れた性能とコスト優位性が各業界で認識され、市場は力強い成長を続けています。これらのフィルムは、その手頃な価格だけでなく、卓越した強度、透明性、多用途性からも支持を集めています。飲食品、製薬、エレクトロニクス、パーソナルケアなどの各分野のメーカーは、軽量で耐久性があり、持続可能な包装材を求める消費者の嗜好の変化に対応するため、BOPPフィルムへのシフトを強めています。

効率的なサプライチェーンと商品棚へのアピールがビジネスの成功に欠かせない時代において、BOPPフィルムは機能性と美観の両方の要求を満たす理想的なソリューションを提供します。そのリサイクル性と進化する持続可能性の目標への適合性は、軟包装市場での地位をさらに強固なものにしています。パッケージング要件が複雑化し、世界の需要が増加し続ける中、BOPPフィルムの生産とコーティング技術の革新は、競争力の維持を目指すメーカーにとって、引き続き重要な焦点となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 297億米ドル |

| 予測金額 | 513億米ドル |

| CAGR | 5.7% |

この市場拡大の主な要因は、費用対効果、高い引張強度、耐湿性、優れた印刷適性により、さまざまな業界でBOPPフィルムの使用が増加していることです。逐次延伸や同時延伸などの高度な製造方法により、透明性とバリア性が大幅に改善されました。メタライゼーションは、視覚的なアピールと保存性を向上させ、これらのフィルムをプレミアムブランディングのための好ましい選択肢にしています。耐熱性を持つコーティングされたBOPPフィルムは、特に電子レンジ対応のパッケージングに適しており、機能的価値を高めています。

市場は製品別にラップ、袋・パウチ、テープ、ラベルに区分されます。2024年には、袋・パウチ分野だけで159億米ドルを占め、eコマースの急成長が大きな原動力となっています。小売業者やフルフィルメントセンターは、従来の硬質包装形式と比較して、その耐穿刺性、軽量構造、物流コスト削減能力から、BOPPバッグやパウチをますます好むようになっています。

厚さで分類すると、15~30ミクロンのセグメントが2024年に37.6%のシェアを占めました。このカテゴリーは、強度、コスト効率、材料削減の完璧なバランスを提供しており、環境に優しく効率的なパッケージング・ソリューションが重視されるようになっていることに合致する主要な特性です。これらのフィルムは、耐久性と最小限の材料使用が不可欠な食品包装に広く使用されています。

米国BOPPフィルム市場は、2024年の北米売上高の86.9%を占める。その優位性は、最終用途を拡大するためにフィルムの強度、透明性、汎用性を高めることを目的とした大手メーカーによる大規模な研究開発投資に起因します。eコマースの急増と軽量で持続可能なパッケージングへの需要により、米国市場は引き続き世界のペースを握っています。

Uflex Ltd.、Inteplast Group、Jindal Poly Filmsのような主要メーカーは、市場でのプレゼンスを拡大し、進化する業界の需要に応えるため、高度な生産システム、製品革新、持続可能性への取り組みに多額の投資を行っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 急速な技術革新と自動化

- 持続可能で環境に優しい包装ソリューションに対する需要の高まり

- 研究開発の進歩によりフィルムの品質と性能が向上

- 食品、医療、電子機器などの分野での応用拡大

- 規制の変更

- 業界の潜在的リスク&課題

- 原材料費の変動

- 激しい市場競争は価格圧力をもたらす

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021 –2034

- 主要動向

- ラップ

- バッグ&ポーチ

- テープ

- ラベル

第6章 市場推計・予測:厚さ別、2021 –2034

- 主要動向

- 15ミクロン以下

- 15~30ミクロン

- 30~45ミクロン

- 45ミクロン以上

第7章 市場推計・予測:生産工程別、2021 –2034

- 主要動向

- テンター

- 管状

第8章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 食べ物

- 飲み物

- タバコ

- パーソナルケア

- 医薬品

- 電気・電子工学

- その他

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- オーストラリア

- 韓国

- 日本

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- CCL Industries

- Cosmo Films Limited

- Gulf Packaging Industries Co.

- Inteplast Group

- Jindal Poly Films

- Oben Group

- Polibak

- Polinas

- Sibur Holdings

- Taghleef Industries

- TOPPAN Group

- Toray Industries

- Uflex Ltd.

- Zhejiang Kinlead Innovative Materials

目次

The Global BOPP Films Market was valued at USD 29.7 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 51.3 billion by 2034. The market continues to witness robust growth as industries across the board recognize the superior performance and cost advantages of BOPP films in packaging applications. These films are gaining traction not only due to their affordability but also because of their exceptional strength, clarity, and versatility. Manufacturers across food and beverage, pharmaceutical, electronics, and personal care sectors are increasingly shifting toward BOPP films to meet changing consumer preferences for lightweight, durable, and sustainable packaging materials.

In an era where efficient supply chains and product shelf appeal are critical to business success, BOPP films offer an ideal solution that meets both functional and aesthetic demands. Their recyclability and compatibility with evolving sustainability goals have further strengthened their position in the flexible packaging market. As packaging requirements become more complex and global demand continues to rise, innovation in BOPP film production and coating technologies remains a key focus for manufacturers aiming to stay competitive.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.7 Billion |

| Forecast Value | $51.3 Billion |

| CAGR | 5.7% |

The primary driver of this market expansion is the increasing use of BOPP films across diverse industries due to their cost-effectiveness, high tensile strength, moisture resistance, and excellent printability. Advanced production methods like sequential and simultaneous stretching have significantly improved clarity and barrier properties. Metallization enhances visual appeal and shelf life, making these films a preferred choice for premium branding. Coated BOPP films, with heat-resistant capabilities, are especially suitable for microwaveable packaging, adding to their functional value.

The market is segmented by product into wraps, bags and pouches, tapes, and labels. In 2024, the bags and pouches segment alone accounted for USD 15.9 billion, driven largely by the exponential growth of e-commerce. Retailers and fulfillment centers increasingly prefer BOPP bags and pouches for their puncture resistance, lightweight structure, and ability to reduce logistics costs when compared to traditional rigid packaging formats.

When classified by thickness, the 15-30 microns segment commanded a 37.6% share in 2024. This category offers a perfect balance of strength, cost-efficiency, and material reduction-key attributes that align with the growing emphasis on eco-friendly and efficient packaging solutions. These films are widely used in food packaging, where durability and minimal material usage are essential.

The U.S. BOPP Films Market accounted for 86.9% of North American revenue in 2024. Its dominance stems from significant R&D investments by leading manufacturers aiming to enhance film strength, clarity, and versatility for broadening end-use applications. With the surge in e-commerce and demand for lightweight, sustainable packaging, the U.S. market continues to set the pace globally.

Key players like Uflex Ltd., Inteplast Group, and Jindal Poly Films are investing heavily in advanced production systems, product innovation, and sustainability initiatives to expand their market presence and cater to evolving industry demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research Approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid technological innovation and automation

- 3.2.1.2 Growing demand for sustainable and eco-friendly packaging solutions

- 3.2.1.3 Advancements in R&D enhance film quality and performance

- 3.2.1.4 Expanding applications in sectors like food, medical, and electronics

- 3.2.1.5 Regulatory changes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material costs

- 3.2.2.2 Intense market competition results in pricing pressures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn & Kilo Tons)

- 5.1 Key trends

- 5.2 Wraps

- 5.3 Bags & pouches

- 5.4 Tapes

- 5.5 Labels

Chapter 6 Market Estimates and Forecast, By Thickness, 2021 – 2034 ($ Mn & Kilo Tons)

- 6.1 Key trends

- 6.2 Below 15 microns

- 6.3 15-30 microns

- 6.4 30-45 microns

- 6.5 More than 45 microns

Chapter 7 Market Estimates and Forecast, By Production Process, 2021 – 2034 ($ Mn & Kilo Tons)

- 7.1 Key trends

- 7.2 Tenter

- 7.3 Tubular

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn & Kilo Tons)

- 8.1 Key trends

- 8.2 Food

- 8.3 Beverage

- 8.4 Tobacco

- 8.5 Personal care

- 8.6 Pharmaceutical

- 8.7 Electrical & electronics

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Australia

- 9.4.4 South Korea

- 9.4.5 Japan

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 U.A.E.

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 CCL Industries

- 10.2 Cosmo Films Limited

- 10.3 Gulf Packaging Industries Co.

- 10.4 Inteplast Group

- 10.5 Jindal Poly Films

- 10.6 Oben Group

- 10.7 Polibak

- 10.8 Polinas

- 10.9 Sibur Holdings

- 10.10 Taghleef Industries

- 10.11 TOPPAN Group

- 10.12 Toray Industries

- 10.13 Uflex Ltd.

- 10.14 Zhejiang Kinlead Innovative Materials

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日