|

市場調査レポート

商品コード

1721428

非MEMSセンサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Non-MEMS Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 非MEMSセンサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月01日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

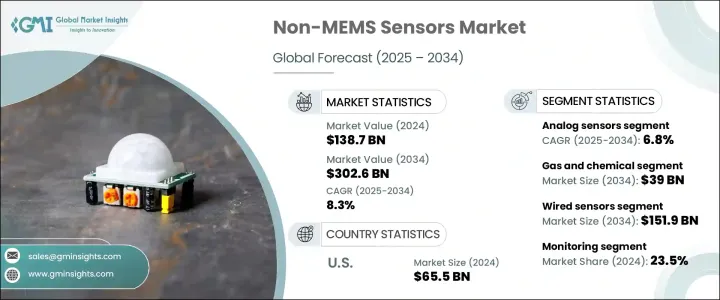

世界の非MEMSセンサー市場は、2024年には1,387億米ドルとなり、CAGR 8.3%で成長し、2034年には3,026億米ドルに達すると予測されています。

同市場は、自動車、ヘルスケア、産業、環境モニタリングなどの主要セクターにおける高精度センサへの幅広い需要に牽引され、上昇基調にあります。自動化、電動化、デジタルヘルスへの世界のシフトが激化する中、次世代技術を可能にする非MEMSセンサーの役割はますます重要になっています。これらのセンサーは現在、自動運転車からインテリジェント医療機器に至るまで、変革的イノベーションの中核を担っており、リアルタイムのデータ処理、安全性向上、業務効率化を可能にしています。企業は競争上の優位性を獲得するために高度なセンシング能力を優先しており、メーカー各社は研究開発に多額の投資を行い、生産能力を拡大しています。インダストリー4.0、スマートシティ、持続可能なエネルギーインフラの台頭は、堅牢で信頼性が高く、用途に特化したセンサー技術への需要をさらに強めています。エンドユーザー向けアプリケーションの範囲が拡大し続けていることから、世界の非MEMSセンサー市場は、今後10年間で大幅な技術進化と事業拡大が見込まれています。

この成長の主な原動力は、拡大する自動車分野と、医療用ウェアラブルやデジタルヘルスケア技術の採用拡大です。ADAS(先進運転支援システム)、自律走行車、電気自動車の需要の増加は、自動車の安全性とナビゲーションを強化するLiDAR、レーダー、光学、圧力センサーなどの非MEMSセンサーのニーズを大幅に押し上げています。ヘルスケア分野では、遠隔患者モニタリングの急増と慢性疾患の蔓延が、非侵襲的健康モニタリング装置に使用されるバイオセンサ、赤外線センサ、光学センサの需要を押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,387億米ドル |

| 予測金額 | 3,026億米ドル |

| CAGR | 8.3% |

市場は技術別にアナログセンサーとデジタルセンサーに区分されます。アナログセンサーは、精密なデータ収集が必要な用途で引き続き重要であるため、2034年までにCAGR 6.8%で成長すると予測されます。アナログセンサーは、複雑な信号処理を必要とせず、過酷な条件下でも安定性と信頼性が高いため、産業オートメーション、温度制御、圧力測定などに広く使用されています。センサーの種類としては、音響センサー、ガス・化学センサー、モーション・位置センサー、光学センサー、圧力センサー、温度センサーがあります。ガス・化学センサは、産業安全、環境モニタリング、ヘルスケアにおいて重要な役割を果たすことから、2034年までに390億米ドルに達すると予想されています。厳しい環境規制と職場の安全重視が、これらの分野における高度なセンシング技術を後押ししています。

米国非MEMSセンサー2024年の市場規模は655億米ドルで、ヘルスケア分野の成長と医療技術の進歩による旺盛な需要を反映しています。遠隔患者モニタリング、デジタルヘルスソリューション、ウェアラブルデバイスの採用が増加しており、これらのイノベーションをサポートする高精度センサのニーズが高まっています。

世界非MEMSセンサー市場の主要企業は、テキサス・インスツルメンツ、ハネウェル、アナログ・デバイセズ、TEコネクティビティ、インフィニオンなどです。各社が採用している主な戦略には、高度なセンサソリューションを開発するための技術革新への注力、センサ性能向上のための研究開発への投資、多様な産業ニーズに対応するための製品ポートフォリオの拡大などがあります。また、各社は戦略的パートナーシップや提携を結び、市場での存在感を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 家電製品におけるスマートセンサーの需要増加

- 自動車産業の拡大

- インダストリー4.0とスマート製造の拡大

- 医療用ウェアラブルとデジタルヘルスケアの導入の増加

- 航空宇宙および防衛分野における先進センサーの利用増加

- 業界の潜在的リスク&課題

- 高度なセンサーの高コスト

- レガシーシステムとの複雑な統合

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:センサータイプ別、2021-2034

- 主要動向

- 音響センサー

- ガス・化学センサー

- モーション&位置センサー

- 光学センサー

- 圧力センサー

- 温度センサー

- その他

第6章 市場推計・予測:技術別、2021-2034

- 主要動向

- アナログセンサー

- デジタルセンサー

第7章 市場推計・予測:接続性別、2021-2034

- 主要動向

- 有線センサー

- ワイヤレスセンサー

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 監視

- ナビゲーションとポジショニング

- 安全とセキュリティ

- 監視と検出

- 追跡と資産管理

- その他

第9章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 航空宇宙および防衛

- 自動車・輸送

- 家電

- エネルギー・公益事業

- ヘルスケア

- 工業および製造業

- その他

第10章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Allegro Microsystems

- AMS-Osram

- Analog Devices

- Honeywell International

- Infineon Technologies

- Keyence

- Murata Manufacturing

- OmniVision Technologies

- Omron

- Panasonic

- Sensirion

- SICK

- TE Connectivity

- Texas Instruments

- XJCSensor

The Global Non-MEMS Sensors Market was valued at USD 138.7 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 302.6 billion by 2034. The market is on an upward trajectory, driven by the widespread demand for high-precision sensors across key sectors such as automotive, healthcare, industrial, and environmental monitoring. As the global shift toward automation, electrification, and digital health intensifies, the role of non-MEMS sensors in enabling next-gen technologies has become increasingly critical. These sensors are now at the core of transformative innovations, from self-driving cars to intelligent medical devices, enabling real-time data processing, safety enhancement, and operational efficiency. Businesses are prioritizing advanced sensing capabilities to gain competitive advantages, prompting manufacturers to invest heavily in R&D and scale their production capabilities. The rise of Industry 4.0, smart cities, and sustainable energy infrastructure further reinforces the demand for robust, reliable, and application-specific sensor technologies. With an ever-expanding scope of end-user applications, the global non-MEMS sensors market is expected to witness significant technological evolution and business expansion over the coming decade.

This growth is primarily fueled by the expanding automotive sector and the rising adoption of medical wearables and digital healthcare technologies. The increasing demand for advanced driver-assistance systems (ADAS), autonomous vehicles, and electric cars has significantly boosted the need for non-MEMS sensors like LiDAR, radar, optical, and pressure sensors, which enhance vehicle safety and navigation. In the healthcare sector, the surge in remote patient monitoring and the growing prevalence of chronic diseases has driven the demand for biosensors, infrared sensors, and optical sensors used in non-invasive health monitoring devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $138.7 Billion |

| Forecast Value | $302.6 Billion |

| CAGR | 8.3% |

The market is segmented by technology into analog and digital sensors. Analog sensors are projected to grow at a CAGR of 6.8% by 2034, as they remain crucial in applications requiring precise data collection. They are widely used in industrial automation, temperature control, and pressure measurement due to their stability and reliability in harsh conditions without complex signal processing. In terms of sensor types, the market includes acoustic, gas and chemical, motion and position, optical, pressure, and temperature sensors. Gas and chemical sensors are expected to reach USD 39 billion by 2034, driven by their critical role in industrial safety, environmental monitoring, and healthcare. The stringent environmental regulations and the focus on workplace safety are pushing for advanced sensing technologies in these areas.

U.S. Non-MEMS Sensors Market generated USD 65.5 billion in 2024, reflecting strong demand driven by the healthcare sector's growth and advancements in medical technology. The increasing adoption of remote patient monitoring, digital health solutions, and wearable devices has escalated the need for high-precision sensors to support these innovations.

Key players in the Global Non-MEMS Sensors Market include Texas Instruments, Honeywell, Analog Devices, TE Connectivity, and Infineon. Key strategies adopted by companies include focusing on technological innovation to develop advanced sensor solutions, investing in research and development for enhanced sensor performance, and expanding their product portfolios to meet diverse industry needs. Companies are also forming strategic partnerships and collaborations to strengthen their market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for smart sensors in consumer electronics

- 3.2.1.2 Expansion of automotive industry

- 3.2.1.3 Expansion of industry 4.0 and smart manufacturing

- 3.2.1.4 Growth in medical wearables and digital healthcare adoption

- 3.2.1.5 Increasing use of advanced sensors in aerospace & defense

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced sensors

- 3.2.2.2 Complex integration with legacy systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Sensor Type, 2021-2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Acoustic sensor

- 5.3 Gas & chemical sensor

- 5.4 Motion & position sensor

- 5.5 Optical sensor

- 5.6 Pressure sensor

- 5.7 Temperature sensor

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Analog sensors

- 6.3 Digital sensors

Chapter 7 Market Estimates & Forecast, By Connectivity, 2021-2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Wired sensors

- 7.3 Wireless sensors

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Units)

- 8.1 Key trends

- 8.2 Monitoring

- 8.3 Navigation & positioning

- 8.4 Safety & security

- 8.5 Surveillance & detection

- 8.6 Tracking & asset management

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 Aerospace & defense

- 9.3 Automotive & transportation

- 9.4 Consumer electronics

- 9.5 Energy & utilities

- 9.6 Healthcare

- 9.7 Industrial & manufacturing

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 ANZ

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Allegro Microsystems

- 11.2 AMS-Osram

- 11.3 Analog Devices

- 11.4 Honeywell International

- 11.5 Infineon Technologies

- 11.6 Keyence

- 11.7 Murata Manufacturing

- 11.8 OmniVision Technologies

- 11.9 Omron

- 11.10 Panasonic

- 11.11 Sensirion

- 11.12 SICK

- 11.13 TE Connectivity

- 11.14 Texas Instruments

- 11.15 XJCSensor