フロントガラスヒーター市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Heated Windshield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721406

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

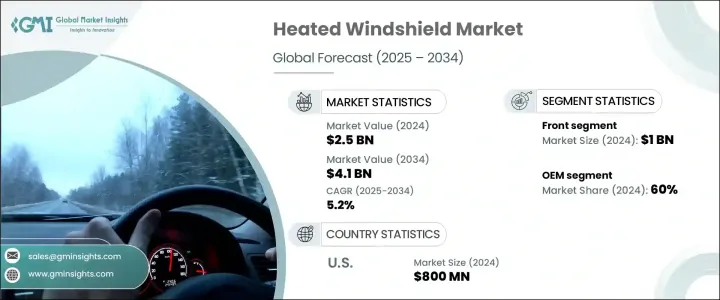

フロントガラスヒーターの世界市場規模は、2024年に25億米ドルとなり、CAGR 5.2%で成長し、2034年には41億米ドルに達すると予測されています。

この成長の主な要因は、視認性の向上、安全機能の強化、極端な気象条件下での適応性の向上に対する消費者の需要の高まりです。特に寒冷地では天候の予測が難しくなっており、自動車購入者はドライバーの安全性と快適性を確保する技術を重視するようになっています。特にフロントガラスのヒーターは、HVACシステムに過度の負担をかけることなく、氷、霜、霧を素早く除去する能力により、大きな注目を集めています。電気自動車や高級車へのシフトが進む自動車業界では、エネルギー効率やADAS(先進運転支援システム)をサポートするフロントガラスヒーターシステムが標準装備となりつつあります。

スマート機能の統合が進み、車両性能の向上が推し進められる中、自動車メーカーはより信頼性が高く、耐久性に優れ、エネルギー効率の高いフロントガラス技術への投資を促しています。さらに、導電性コーティングと内蔵発熱体の進歩が競合情勢を再構築し、OEMとアフターマーケットの両チャネルにおける購入決定に影響を与えています。メーカーは、安全性、効率性、持続可能性に対する進化する規制基準や消費者の期待に沿うことで対応しており、予測期間を通じて採用と技術革新がさらに促進されると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 25億米ドル |

| 予測金額 | 41億米ドル |

| CAGR | 5.2% |

フロントガラスヒーターは、霜、霧、氷の堆積を除去することで安全性を高め、悪天候でもクリアな視界を提供するよう特別に設計されています。これらのソリューションは、高速霜取りがドライバーの快適性をサポートするだけでなく、ADASのシームレスな機能を保証する電気自動車や高級車において特に重要です。埋め込みワイヤーや透明導電層などの高度な加熱技術を取り入れることで、より迅速な除霜、耐摩耗性の向上、従来の空調制御システムへの依存度の低減が可能になり、フロントガラス加熱は最新の自動車における貴重な資産となっています。

市場はフロントガラスとリアガラスに分類され、フロントガラスは2024年に10億米ドルを創出します。このセグメントが突出しているのは、ドライバーの視界を維持し、遮られない視界を必要とするADASコンポーネントをサポートする役割によるところが大きいです。リア・ヒーテッド・ウィンドシールドもまた、特に後方視界が後退時に重要であるフリート車や商用車において、普及が進んでいます。しかし、リア・ウインドシールドの採用率は、フロント・セグメントのそれをまだ下回っています。

販売チャネルに関しては、市場は相手先商標製品メーカー(OEM)とアフターマーケットに分かれています。OEMは2024年の市場シェアの60%を占めているが、これは主に電気自動車や高級車における工場装着型ソリューションの需要増によるものです。これらのフロントガラスはADASや自動運転システムとシームレスに統合され、過酷な条件下でも最高レベルの性能を保証します。

米国フロントガラスヒーター市場は2024年に8億米ドルに達し、電気自動車や高級車の普及が進み、先進安全技術への需要が高まっています。米国の自動車メーカーは、省エネと優れた視認性を求める消費者ニーズに対応するため、フロントガラスヒーターシステムを積極的に導入しています。これらのシステムは、空調負荷を低減し、最適な霜取り性能を確保することで、EVのバッテリー効率を維持する上で極めて重要な役割を果たしています。

世界のフロントガラスヒーター分野をリードする主要企業には、日本板硝子、AGC、福耀ガラス、ガーディアン・ガラス、フォルクスワーゲン、ピルキントン、マグナ、サンゴバン・セキュリット、テスラ、トヨタ自動車などがあります。これらの企業は、次世代のヒーティング技術を開発するために研究開発に多額の投資を行っており、高級車や高性能車セグメントにおける需要の高まりに対応するためにOEMと戦略的パートナーシップを結んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 電気自動車の普及拡大

- スマートガラスと導電性コーティングの進歩

- より厳しい安全性と視認性規制

- 商用車セグメントの拡大

- 業界の潜在的リスク&課題

- 製造コストと交換コストが高め

- ADASとスマート機能との複雑な統合

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:ポジション別、2021-2034

- 主要動向

- フロント

- 後方

第6章 市場推計・予測:ガラス製、2021-2034

- 主要動向

- ラミネート加工

- 導電性コーティングガラス

- 鍛えられた

- その他

第7章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車

- MCV

- HCV

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- アフターマーケット

- OEM

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AGC

- BMW

- Corning

- Ford Motor

- Fuyao Glass

- General Motors

- Guardian Glass

- Hyundai Motor

- Magna

- Mercedes-Benz

- Nippon Sheet Glass

- Pilkington

- Saint-Gobain Sekurit

- Stellantis

- Tesla

- Toyota

- Volkswagen

- Volvo

- Webasto

- Xinyi Glass

目次

The Global Heated Windshield Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 4.1 billion by 2034. This growth is primarily driven by rising consumer demand for improved visibility, enhanced safety features, and increased adaptability in extreme weather conditions. As weather unpredictability intensifies, especially in colder regions, automotive buyers are placing greater importance on technologies that ensure driver safety and comfort. Heated windshields, in particular, are gaining significant attention due to their ability to rapidly clear ice, frost, and fog without overburdening the HVAC system. With the automotive industry witnessing a strong shift toward electric and luxury vehicles, heated windshield systems are becoming standard features that support energy efficiency and advanced driver assistance systems (ADAS).

The growing integration of smart features and the push for higher vehicle performance have prompted automakers to invest in more reliable, durable, and energy-efficient windshield technologies. Additionally, advancements in conductive coatings and embedded heating elements are reshaping the competitive landscape and influencing purchase decisions across both OEM and aftermarket channels. Manufacturers are responding by aligning with evolving regulatory standards and consumer expectations for safety, efficiency, and sustainability, which is expected to further drive adoption and technological innovation throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.2% |

Heated windshields are specifically designed to boost safety by eliminating the accumulation of frost, fog, and ice, thereby offering clear visibility in adverse weather. These solutions are especially important in electric and premium vehicles where fast defrosting supports not only driver comfort but also ensures the seamless functioning of ADAS. The incorporation of advanced heating technologies, such as embedded wires and transparent conductive layers, allows for faster defogging, greater resistance to wear, and reduced reliance on traditional climate control systems-making heated windshields a valuable asset in modern vehicles.

The market is categorized into front and rear windshields, with the front segment generating USD 1 billion in 2024. The prominence of this segment is largely attributed to its role in maintaining driver visibility and supporting ADAS components that require an unobstructed view. Rear heated windshields are also experiencing increased traction, especially in fleet and commercial vehicles, where rear visibility is critical during reversing. However, the adoption rate of rear windshields still trails that of the front segment.

In terms of sales channels, the market is divided between original equipment manufacturers (OEMs) and the aftermarket. OEMs accounted for 60% of the market share in 2024, largely due to the rising demand for factory-installed solutions in electric and high-end vehicles. These windshields are seamlessly integrated with ADAS and self-driving systems, ensuring top-tier performance even in harsh conditions.

The U.S. Heated Windshield Market reached USD 800 million in 2024, propelled by the growing adoption of electric and luxury vehicles, along with the demand for advanced safety technologies. U.S. automakers are actively implementing heated windshield systems to address consumer needs for energy savings and superior visibility. These systems play a pivotal role in preserving battery efficiency in EVs by reducing the HVAC load and ensuring optimal defrosting performance.

Key companies leading the global heated windshield space include Nippon Sheet Glass, AGC, Fuyao Glass, Guardian Glass, Volkswagen, Pilkington, Magna, Saint-Gobain Sekurit, Tesla, and Toyota Motor. These players are heavily investing in R&D to develop next-generation heating technologies and are forging strategic partnerships with OEMs to cater to the rising demand in luxury and high-performance vehicle segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing adoption in electric vehicles

- 3.7.1.2 Advancements in smart glass & conductive coatings

- 3.7.1.3 Stricter safety & visibility regulations

- 3.7.1.4 Expansion in the commercial vehicle segment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High manufacturing & replacement costs

- 3.7.2.2 Complex integration with ADAS & smart features

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Position, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Front

- 5.3 Rear

Chapter 6 Market Estimates & Forecast, By Glass, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Laminated

- 6.3 Conductive coated glass

- 6.4 Tempered

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Aftermarket

- 8.3 OEM

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AGC

- 10.2 BMW

- 10.3 Corning

- 10.4 Ford Motor

- 10.5 Fuyao Glass

- 10.6 General Motors

- 10.7 Guardian Glass

- 10.8 Hyundai Motor

- 10.9 Magna

- 10.10 Mercedes-Benz

- 10.11 Nippon Sheet Glass

- 10.12 Pilkington

- 10.13 Saint-Gobain Sekurit

- 10.14 Stellantis

- 10.15 Tesla

- 10.16 Toyota

- 10.17 Volkswagen

- 10.18 Volvo

- 10.19 Webasto

- 10.20 Xinyi Glass

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日