小型言語モデルの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Small Language Models (SLM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721401

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

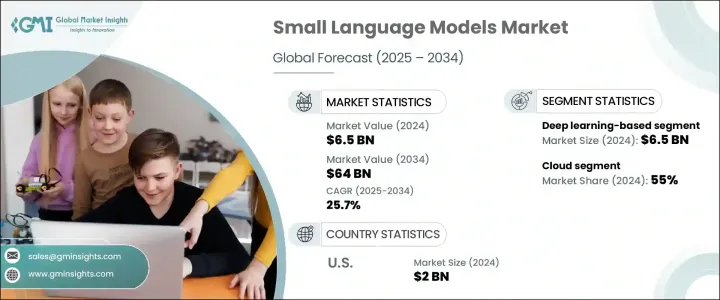

世界の小規模言語モデル市場は、2024年に65億米ドルと評価され、CAGR 25.7%で成長し、2034年には640億米ドルに達すると推定されています。

人工知能が企業オペレーションの未来を形成し続ける中、SLMは進化するAIランドスケープの中で明確なニッチを切り開きつつあります。世界中の企業は現在、インテリジェントな自動化、リアルタイムのコミュニケーション、超パーソナライズされたユーザー体験を優先しています。

このシフトは、特に迅速な意思決定、効率的な言語処理、データに敏感なオペレーションを必要とする分野において、SLMの需要が急増するきっかけとなりました。世界企業が生産性向上のためにAI主導のツールにますます傾倒する中、限られたリソースで高いパフォーマンスを発揮するコンパクトで俊敏なモデルの採用が着実に進んでいます。組織が分散型AIソリューションに移行する中、SLMはオンデバイス・アプリケーションに最適なものとして登場し、精度、効率、コストのシームレスなバランスを提供しています。データ・プライバシーに対する懸念の高まりとエッジ・コンピューティング導入の急増は、技術先進国である今日の世界におけるSLMの関連性をさらに高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 65億米ドル |

| 予測金額 | 640億米ドル |

| CAGR | 25.7% |

企業は、従来のLLMのような計算量や経済的な負担をかけずに人工知能の可能性を引き出すために、小規模言語モデルを積極的に活用しています。このようなモデルは、リアルタイムのテキスト生成、音声認識、文脈理解が重要な役割を果たすヘルスケア、金融、教育、顧客サービスなどの分野で注目されています。インテリジェントなチャットボット、音声アシスタントの強化、ダイナミックなコンテンツ作成の実現など、SLMは現代の企業にとって不可欠なツールになりつつあります。その軽量アーキテクチャは、モバイルデバイス、エッジシステム、組み込みプラットフォームで効率的に実行する必要がある低レイテンシのアプリケーションに最適です。

ディープラーニングベースの小型言語モデル分野だけでも、2024年には65億米ドルの売上があり、ニューラルネットワークとトランスフォーマーベースのアーキテクチャへの依存が高まっていることを裏付けています。これらのモデルは、要約、自然会話、翻訳などの高精度タスクに最適化されています。企業がデジタルトランスフォーメーションを加速させる中、こうしたAIを活用したソリューションに対する需要は、業界を問わず急速に拡大しています。

2024年のSLM市場は、クラウドベースの展開が55%のシェアを占めました。組織は、拡張性、手頃な価格、統合の容易さから、クラウドネイティブなソリューションを好んでいます。この動向は、企業が複雑なオンプレミス設定に投資することなく、進化する業務ニーズにAIツールを迅速に適応させることができる、柔軟な展開モデルへの幅広い動きを反映しています。

米国の小規模言語モデル市場だけでも、2024年には20億米ドルを占める。この成長を後押ししているのは、イノベーション主導の技術エコシステム、クラウドの普及、ヘルスケア、eコマース、金融などの業界におけるNLPベースの自動化利用の増加です。

この市場を牽引する主要企業には、Amazon AWS AI、Apple AI、Cerebras Systems、Cohere、Databricks、Google、IBM Watson AI、Meta、Microsoft、Nvidiaなどがあります。これらの企業は、戦略的パートナーシップ、クラウドプラットフォームの拡大、モデルの拡張性とドメイン固有の適応性を強化するための研究開発への的を絞った投資を通じて存在感を強めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- コスト効率の高いAIソリューションの需要の高まり

- エッジコンピューティングとデバイス内処理におけるAIの採用拡大

- プライバシー中心のAIモデルへの注目が高まる

- AIを活用した顧客サポートとコンテンツ生成の拡大

- 業界の潜在的リスク&課題

- 限られたトレーニングデータとモデルパフォーマンスの制約

- 偏見、AIの倫理、コンプライアンス問題への懸念

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:技術別、2021-2034

- 主要動向

- ディープラーニングベース

- 機械学習ベース

- ルールベースのシステム

第6章 市場推計・予測:モデル別、2021-2034

- 主要動向

- 事前トレーニング済み

- 微調整

- オープンソース

第7章 市場推計・予測:展開別、2021-2034

- 主要動向

- クラウド

- ハイブリッド

- オンプレミス

第8章 市場推計・予測:最終用途別2021-2034

- 主要動向

- カスタマーサポートとチャットボット

- 金融サービスと銀行

- ヘルスケアと医療AI

- メディアとコンテンツの生成

- 小売・Eコマース

- 教育とEラーニング

- 法務およびコンプライアンス

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AI21 Labs

- Aleph Alpha

- Amazon AWS AI

- Anthropic

- Apple AI

- Cerebras Systems

- Cohere

- Databricks(MosaicML)

- Google DeepMind

- Hugging Face

- IBM Watson AI

- Meta(FAIR)

- Microsoft

- Mistral AI

- NVIDIA AI

- OpenAI

- Rasa AI

- Salesforce AI Research

- SAP AI

- Stability AI

目次

The Global Small Language Models Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 25.7% to reach USD 64 billion by 2034. As artificial intelligence continues to shape the future of enterprise operations, SLMs are carving a distinct niche in the evolving AI landscape. Businesses worldwide are now prioritizing intelligent automation, real-time communication, and hyper-personalized user experiences-all without incurring the massive infrastructure costs typically associated with large language models (LLMs).

This shift has triggered a sharp rise in the demand for SLMs, particularly in sectors that require quick decision-making, efficient language processing, and data-sensitive operations. With global enterprises increasingly leaning on AI-driven tools to enhance productivity, the adoption of compact, agile models that offer high performance on limited resources is steadily climbing. As organizations move toward decentralized AI solutions, SLMs emerge as the perfect fit for on-device applications, offering a seamless balance between accuracy, efficiency, and cost. Growing concerns over data privacy and the surge in edge computing deployment further amplify the relevance of SLMs in today's tech-forward world.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $64 Billion |

| CAGR | 25.7% |

Businesses are actively turning to small language models to unlock the potential of artificial intelligence without the heavy computational and financial load of traditional LLMs. These models have gained notable traction in healthcare, finance, education, and customer service, where real-time text generation, voice recognition, and contextual understanding play critical roles. Whether powering intelligent chatbots, enhancing voice assistants, or enabling dynamic content creation, SLMs are becoming essential tools for modern enterprises. Their lightweight architecture makes them ideal for low-latency applications that must run efficiently on mobile devices, edge systems, or embedded platforms.

The deep learning-based small language models segment alone generated USD 6.5 billion in 2024, underscoring the growing reliance on neural networks and transformer-based architectures. These models are optimized for high-precision tasks such as summarization, natural conversation, translation, and more. As companies accelerate digital transformation, demand for these AI-powered solutions is rapidly expanding across verticals.

Cloud-based deployment dominated the SLM market in 2024, holding a 55% share. Organizations prefer cloud-native solutions for their scalability, affordability, and ease of integration. This trend reflects a broader movement toward flexible deployment models, where businesses can quickly adapt their AI tools to evolving operational needs without investing in complex on-premise setups.

The United States Small Language Models Market alone accounted for USD 2 billion in 2024. This growth is fueled by the nation's innovation-driven tech ecosystem, widespread cloud adoption, and increasing use of NLP-based automation across industries such as healthcare, e-commerce, and finance.

Key players driving this market include Amazon AWS AI, Apple AI, Cerebras Systems, Cohere, Databricks, Google, IBM Watson AI, Meta, Microsoft, and Nvidia. These companies are strengthening their presence through strategic partnerships, cloud platform expansions, and targeted investments in R&D to enhance model scalability and domain-specific adaptability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for cost-efficient AI solutions

- 3.7.1.2 Growing adoption of AI in edge computing & on-device processing

- 3.7.1.3 Increasing focus on privacy-centric AI models

- 3.7.1.4 Expansion of AI-powered customer support & content generation

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Limited training data & model performance constraints

- 3.7.2.2 Concerns over bias, ethical ai, and compliance issues

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Deep learning based

- 5.3 Machine learning based

- 5.4 Rule based system

Chapter 6 Market Estimates & Forecast, By Model Type, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Pre-trained

- 6.3 Fine-tuned

- 6.4 Open source

Chapter 7 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 Hybrid

- 7.4 On-premises

Chapter 8 Market Estimates & Forecast, By End Use 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Customer support & chatbots

- 8.3 Financial services & banking

- 8.4 Healthcare & medical AI

- 8.5 Media & content generation

- 8.6 Retail & E-commerce

- 8.7 Education & E-learning

- 8.8 Legal & compliance

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AI21 Labs

- 10.2 Aleph Alpha

- 10.3 Amazon AWS AI

- 10.4 Anthropic

- 10.5 Apple AI

- 10.6 Cerebras Systems

- 10.7 Cohere

- 10.8 Databricks (MosaicML)

- 10.9 Google DeepMind

- 10.10 Hugging Face

- 10.11 IBM Watson AI

- 10.12 Meta (FAIR)

- 10.13 Microsoft

- 10.14 Mistral AI

- 10.15 NVIDIA AI

- 10.16 OpenAI

- 10.17 Rasa AI

- 10.18 Salesforce AI Research

- 10.19 SAP AI

- 10.20 Stability AI

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日