|

市場調査レポート

商品コード

1716685

ハイドロニックポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Hydronic Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ハイドロニックポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月17日

発行: Global Market Insights Inc.

ページ情報: 英文 487 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

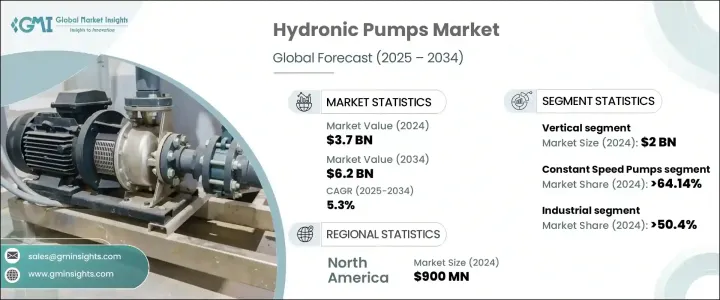

ハイドロニックポンプの世界市場は、2024年に37億米ドルと評価され、2025年から2034年にかけてCAGR 5.3%で成長すると予測されています。

エネルギー効率と持続可能性に対する需要の高まりが、特に暖房、換気、空調(HVAC)システムにおいて、ハイドロニックポンプの採用を促進しています。米国ではエネルギースター、欧州連合(EU)では同様の指令など、政府や規制機関が厳しい環境基準を施行する中、エネルギー効率の高い技術を求める動きは強まり続けています。二酸化炭素排出量と運用コストの削減が重視されるようになったことで、産業界は住宅と商業施設の両方のインフラにハイドロニックポンプシステムを統合することを奨励しています。

これらのポンプは、効率的な熱と流体の循環を確保することで、エネルギー消費を最適化する上で重要な役割を果たし、現代の建築システムにおいて不可欠なコンポーネントとなっています。さらに、IoT機能を備えたスマートポンプなど、ポンプ設計の技術的進歩は、システム効率を高め、ダウンタイムを削減するリアルタイムの監視と予知保全を提供することで、状況を一変させています。世界中でグリーンビルディング構想の採用が増加していることが、市場の成長をさらに促進しています。不動産開発業者がエネルギーを意識した設計に注力する中、ハイドロニックポンプは持続可能性の目標を達成する上で不可欠なものとなりつつあります。気候変動に対する意識の高まりと、省エネソリューションを導入する必要性が、市場の長期的展望を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 37億米ドル |

| 予測金額 | 62億米ドル |

| CAGR | 5.3% |

縦型ハイドロニックポンプセグメントは、2024年に20億米ドルを占め、2034年までCAGR 5.4%で成長する見込みです。縦型ポンプは、少ないスペースで高圧システムを処理する能力により、人気を集めています。コンパクトな設計のため、スペースの制約が懸念される商業、工業、HVAC環境での用途に最適です。これらのポンプは、限られた環境で冷暖房用の水やその他の流体を循環させるのに非常に効率的であるため、信頼性の高い高圧性能を必要とするさまざまな業界で好まれています。都市化が加速し、建物の設計がスペースの最適化を優先するようになるにつれて、縦型水熱式ポンプの需要は大幅に増加するものと思われます。

定速ポンプは2024年に64%の市場シェアを占め、2034年まで5%の安定した成長率を維持すると予想されます。これらのポンプは、住宅や商業用冷暖房システムなど、一定の流量を必要とするシステムで一般的に使用されています。一定速度で作動するように設計された定速ポンプは、予測可能で信頼性の高い流体循環を提供し、低需要環境に最適です。特に、信頼性の高いHVACシステムに対するニーズが住宅・商業の両分野で高まる中、その運転安定性と効率性が引き続き採用の原動力となっています。

北米のハイドロニックポンプ市場は26.4%のシェアを占め、2024年には9億米ドルを生み出しました。同地域ではエネルギー効率規制が強化されており、建設部門が高性能水熱式ポンプを含む省エネ技術を採用する原動力となっています。建築プロジェクトでは持続可能性が重視され続けているため、進化するエネルギー基準への適合を確実にするこれらのポンプへの需要が引き続き高まっています。さらに、アジア太平洋地域では、特に農業分野で顕著な成長が見られ、農法の近代化と機械化によって水熱式ポンプの使用が増加しています。多様な産業におけるハイドロニックポンプの応用範囲の拡大は、今後数年間の世界市場の成長軌道を後押しすると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 価格分析

- テクノロジーとイノベーションの展望

- 主要ニュース&イニシアティブ

- 規制状況

- メーカー

- 販売業者

- 小売業者

- 影響要因

- 促進要因

- エネルギー効率に関する規制と基準

- 建設活動の拡大

- 再生可能エネルギーの統合

- 都市化とインフラ開発

- 業界の潜在的リスク&課題

- 市場の飽和と激しい競合

- 高額な初期投資

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 縦型

- 横型

第6章 市場推計・予測:速度別、2021年~2034年

- 主要動向

- 定速ポンプ

- 可変速ポンプ

第7章 市場推計・予測:GPM流量別、2021年~2034年

- 主要動向

- 1GPM未満

- 1~2GPM未満

- 2~5GPM

- 5~10GPM

- 10-15 GPM

- 15GPM以上

第8章 市場推計・予測:電力別、2021年~2034年

- 主要動向

- 100W未満

- 100-500W

- 500W以上

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 温水

- 冷水

- 蒸気

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- 産業用

第11章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接販売

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- Armstrong Fluid Technology

- Biral AG

- DAB Pumps

- Danfoss

- Flowserve Corporation

- Franklin Electric

- Grundfos

- ITT Inc.

- KSB Group

- Pentair plc

- Sulzer Ltd.

- Taco Comfort Solutions

- Uponor Corporation

- Wilo

- Xylem Inc.

The Global Hydronic Pumps Market was valued at USD 3.7 billion in 2024 and is projected to grow at a CAGR of 5.3% between 2025 and 2034. Increasing demand for energy efficiency and sustainability is driving the adoption of hydronic pumps, particularly in heating, ventilation, and air conditioning (HVAC) systems. As governments and regulatory bodies enforce stringent environmental standards, such as Energy Star in the United States and similar directives in the European Union, the push for energy-efficient technologies continues to intensify. The growing emphasis on reducing carbon emissions and operational costs is encouraging industries to integrate hydronic pump systems into both residential and commercial infrastructure.

These pumps play a crucial role in optimizing energy consumption by ensuring efficient heat and fluid circulation, making them a vital component in modern building systems. Additionally, technological advancements in pump designs, such as smart pumps with IoT capabilities, are transforming the landscape by offering real-time monitoring and predictive maintenance, which enhances system efficiency and reduces downtime. The rising adoption of green building initiatives across the globe is further propelling market growth. As property developers focus on energy-conscious designs, hydronic pumps are becoming essential in meeting sustainability goals. The growing awareness about climate change and the need to implement energy-saving solutions is boosting the market's long-term prospects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 5.3% |

The vertical hydronic pump segment accounted for USD 2 billion in 2024 and is expected to grow at a CAGR of 5.4% through 2034. Vertical pumps are gaining traction due to their ability to handle high-pressure systems while occupying less space. Their compact design makes them ideal for applications in commercial, industrial, and HVAC settings where space constraints are a concern. These pumps are highly efficient in circulating water or other fluids for heating and cooling in confined environments, which makes them a preferred choice in various industries that require reliable, high-pressure performance. As urbanization accelerates and building designs prioritize space optimization, the demand for vertical hydronic pumps is set to increase significantly.

Constant speed pumps held a 64% market share in 2024 and are expected to maintain a steady growth rate of 5% through 2034. These pumps are commonly used in systems requiring a consistent flow rate, such as residential and commercial heating and cooling systems. Designed to operate at a fixed speed, constant-speed pumps provide predictable and reliable fluid circulation, making them ideal for low-demand environments. Their operational stability and efficiency continue to drive their adoption, particularly as the need for reliable HVAC systems grows in both residential and commercial sectors.

North America hydronic pumps market accounted for a 26.4% share and generated USD 900 million in 2024. Stricter energy efficiency regulations in the region are driving the construction sector to adopt energy-saving technologies, including high-performance hydronic pumps. The ongoing emphasis on sustainability in building projects continues to fuel demand for these pumps, ensuring compliance with evolving energy standards. In addition, the Asia Pacific region has witnessed remarkable growth, particularly in the agricultural sector, where modernization and mechanization of farming practices have increased the use of hydronic pumps. The expanding scope of hydronic pump applications in diverse industries is expected to bolster the global market's growth trajectory over the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.4.2.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.3 Pricing analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Manufacturers

- 3.8 Distributors

- 3.9 Retailers

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Energy efficiency regulations and standards

- 3.10.1.2 Growing construction activities

- 3.10.1.3 Renewable energy integration

- 3.10.1.4 Urbanization and infrastructure development

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Market saturation and intense competition

- 3.10.2.2 High initial investment

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Vertical

- 5.3 Horizontal

Chapter 6 Market Estimates & Forecast, By Speed, 2021-2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Constant speed pumps

- 6.3 Variable speed pumps

Chapter 7 Market Estimates & Forecast, By GPM Flow, 2021-2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Below 1GPM

- 7.3 1-2 GPM

- 7.4 2-5 GPM

- 7.5 5-10 GPM

- 7.6 10-15 GPM

- 7.7 Above 15 GPM

Chapter 8 Market Estimates & Forecast, By Power, 2021-2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Upto 100W

- 8.3 100-500W

- 8.4 Above 500W

Chapter 9 Market Estimates & Forecast, By Usage, 2021-2034 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Heated water

- 9.3 Chilled water

- 9.4 Steam

Chapter 10 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

- 10.4 Industrial

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Direct

- 11.3 Indirect

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Armstrong Fluid Technology

- 13.2 Biral AG

- 13.3 DAB Pumps

- 13.4 Danfoss

- 13.5 Flowserve Corporation

- 13.6 Franklin Electric

- 13.7 Grundfos

- 13.8 ITT Inc.

- 13.9 KSB Group

- 13.10 Pentair plc

- 13.11 Sulzer Ltd.

- 13.12 Taco Comfort Solutions

- 13.13 Uponor Corporation

- 13.14 Wilo

- 13.15 Xylem Inc.