|

市場調査レポート

商品コード

1716678

エッジAI市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Edge AI Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| エッジAI市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月10日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

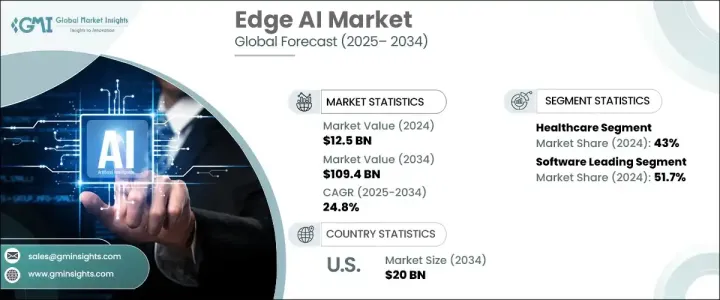

世界のエッジAI市場は、2024年に125億米ドルと評価され、インテリジェントな分散型コンピューティング・ソリューションに対する需要の急速な急増に牽引され、2025年から2034年にかけて24.8%の堅調なCAGRで拡大すると予測されています。

産業界がデジタルトランスフォーメーションを受け入れ続ける中、エッジAIは、企業がデータをソースで直接処理・分析することを可能にし、待ち時間の短縮、セキュリティの向上、クラウドインフラへの依存の最小化を実現する、ゲームを変えるテクノロジーとして台頭しています。IoTデバイスの普及が進み、5GやAIチップセットへの投資が拡大していることも相まって、ヘルスケア、製造、小売、自動車、通信など重要な分野でのエッジAIの導入がさらに加速しています。

特に産業がインダストリー4.0やAI主導のエコシステムへとシフトする中、企業はリアルタイムの意思決定や自動化を支援するソリューションを優先しています。エッジAIソリューションは、より迅速な洞察を可能にし、オペレーションのボトルネックを軽減し、パーソナライズされた体験を提供する上で重要な役割を果たしています。また、エッジデバイスから生成される大量のデータを効率的かつ安全に処理する必要性が高まっていることから、企業は継続的なクラウド接続に依存せずにデバイス上で実行できるAIアルゴリズムに多額の投資を行うようになっています。さらに、AIプロセッサーとエッジAI専用ハードウェアの進歩により、あらゆる規模の企業にとって、これらのソリューションがより利用しやすく、コスト効率に優れ、スケーラブルになりつつあります。データプライバシーに関する懸念が高まるにつれ、企業はデータの安全な取り扱いと規制遵守のためにエッジAIを利用するようになっており、市場の成長はさらに強まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 125億米ドル |

| 予測金額 | 1,094億米ドル |

| CAGR | 24.8% |

エッジAI市場は、ヘルスケア、製造、銀行・金融サービス、政府、小売、通信、輸送、物流など、複数の最終用途産業にまたがっています。なかでもヘルスケアは、エッジにおけるAIが患者ケアに革命をもたらし続けていることから、2024年には43%のシェアで世界市場を席巻しました。ヘルスケアプロバイダーは、AIを搭載したウェアラブル、遠隔モニタリングシステム、高度診断ツールを使用して、リアルタイムでの患者追跡、自動医療画像分析、迅速な臨床意思決定を可能にしています。こうした技術革新は、患者の転帰を改善するだけでなく、業務の効率化と医療費の削減にもつながります。

コンポーネントに基づき、市場はソフトウェア、ハードウェア、サービスに区分され、2024年の市場シェアはソフトウェアが51.7%を占める。ソフトウェアソリューションの台頭は、AIモデルの展開、リアルタイム分析の促進、エッジにおけるデータセキュリティの確保において重要な役割を果たすことに起因しています。AIソフトウェアフレームワークは、エッジデバイスが独立してデータを処理・分析し、AIモデルの更新をサポートし、クラウドに依存せずにシステムパフォーマンスを最適化できるようにするために不可欠であり、インスタントでインテリジェントな洞察に対するニーズの高まりに対応しています。

米国のエッジAI市場は、ヘルスケア、スマートシティ、産業オートメーションへのAIの普及を背景に、2034年までに200億米ドルに達すると予測されています。AIチップとエッジプラットフォームを開発する主要ハイテク企業や半導体企業の存在感が強く、AIイノベーションとインフラ近代化を推進する政府のイニシアティブと相まって、成長が加速しています。5G、IoT、クラウドとエッジの統合における急速な進歩は、米国におけるエッジAI展開のためのダイナミックなエコシステムを形成し続けています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- ハードウェアプロバイダー

- ソフトウェアプロバイダー

- クラウドサービスプロバイダー

- マネージド・サービス・プロバイダー

- エンドユース

- サプライヤーの状況

- 利益率分析

- テクノロジー&イノベーション・情勢

- 特許分析

- 主要ニュースと取り組み

- ケーススタディ

- 規制状況

- 影響要因

- 促進要因

- 様々なエンドユース分野でのエッジデバイスの採用拡大

- AI技術への投資の増加

- 5Gネットワークの採用拡大

- クラウドコンピューティング技術の採用急増

- 業界の潜在的リスク&課題

- プライバシーとセキュリティに関する懸念

- 相互運用性の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- グラフィックス・プロセッシング・ユニット(GPU)

- 特定用途向け集積回路(ASIC)、

- 中央演算処理装置(CPU)

- フィールドプログラマブルゲートアレイ(FPGA)

- ソフトウェア

- サービス

- トレーニング&コンサルティング

- サポート&メンテナンス

- システムインテグレーションとテスト

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ビデオ監視

- 遠隔監視

- 予知保全

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製造業

- ヘルスケア

- BSFI市場

- 政府機関

- 小売・eコマース

- 通信

- 運輸・物流

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Anagog

- Amazon

- ADLINK

- Clearblade

- Cloudera

- Dell

- Gorilla Technology

- Huawei

- IBM

- Intel

- Microsoft

- MediaTek

- Mavenir System

- Nutanix

- Nvidia

- Synaptics

- Qualcomm

- Veea

- Xilinx

The Global Edge AI Market, valued at USD 12.5 billion in 2024, is projected to expand at a robust CAGR of 24.8% from 2025 to 2034, driven by the rapid surge in demand for intelligent, decentralized computing solutions. As industries continue to embrace digital transformation, edge AI is emerging as a game-changing technology that enables businesses to process and analyze data directly at the source - reducing latency, improving security, and minimizing dependency on cloud infrastructures. The increasing penetration of IoT devices, coupled with growing investments in 5G and AI chipsets, is further fueling the adoption of edge AI across critical sectors, including healthcare, manufacturing, retail, automotive, and telecommunications.

Companies are prioritizing solutions that empower real-time decision-making and automation, particularly as industries shift toward Industry 4.0 and AI-driven ecosystems. Edge AI solutions are playing a crucial role in enabling faster insights, reducing operational bottlenecks, and delivering personalized experiences. The growing need to handle massive amounts of data generated by edge devices efficiently and securely has also prompted enterprises to invest heavily in AI algorithms that can run on-device without relying on continuous cloud connectivity. Moreover, advancements in AI processors and dedicated edge AI hardware are making these solutions more accessible, cost-effective, and scalable for businesses of all sizes. As data privacy concerns escalate, organizations are increasingly turning to edge AI for secure data handling and regulatory compliance, further strengthening market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.5 Billion |

| Forecast Value | $109.4 Billion |

| CAGR | 24.8% |

The edge AI market spans several end-use industries, including healthcare, manufacturing, banking and financial services, government, retail, telecommunications, transportation, and logistics. Among these, healthcare dominated the global market with a 43% share in 2024, as AI at the edge continues to revolutionize patient care. Healthcare providers are using AI-powered wearables, remote monitoring systems, and advanced diagnostics tools to enable real-time patient tracking, automated medical image analysis, and faster clinical decision-making. These innovations not only improve patient outcomes but also streamline operations and reduce healthcare costs.

Based on components, the market is segmented into software, hardware, and services, with software accounting for 51.7% of the total market share in 2024. The rising prominence of software solutions is attributed to their critical role in deploying AI models, facilitating real-time analytics, and ensuring data security at the edge. AI software frameworks are essential for enabling edge devices to process and analyze data independently, support AI model updates, and optimize system performance without cloud reliance, addressing the growing need for instant, intelligent insights.

The U.S. edge AI market is anticipated to reach USD 20 billion by 2034, backed by the country's widespread adoption of AI across healthcare, smart cities, and industrial automation. The strong presence of leading tech giants and semiconductor companies developing AI chips and edge platforms, coupled with government initiatives promoting AI innovation and infrastructure modernization, is accelerating growth. Rapid advancements in 5G, IoT, and cloud-edge integration continue to shape a dynamic ecosystem for edge AI deployment in the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Hardware providers

- 3.1.2 Software providers

- 3.1.3 Cloud service providers

- 3.1.4 Managed service provider

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Case studies

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of edge devices across various end use verticals

- 3.9.1.2 Growing investment in AI technology

- 3.9.1.3 Growing adoption of 5G network

- 3.9.1.4 Surging adoption of cloud computing technology

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Privacy and security concerns

- 3.9.2.2 Interoperability issues

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Graphics Processing Unit (GPU)

- 5.2.2 Application Specific Integrated Circuit (ASIC),

- 5.2.3 Central Processing Unit (CPU)

- 5.2.4 Field-Programmable Gate Array (FPGA)

- 5.3 Software

- 5.4 Service

- 5.4.1 Training & consulting

- 5.4.2 Support & maintenance

- 5.4.3 System integration and testing

Chapter 6 Market Estimates & Forecast, By Application, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Video surveillance

- 6.3 Remote monitoring

- 6.4 Predictive maintenance

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Manufacturing

- 7.3 Healthcare

- 7.4 BSFI

- 7.5 Government

- 7.6 Retail & e-commerce

- 7.7 Telecommunication

- 7.8 Transport & logistics

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Anagog

- 9.2 Amazon

- 9.3 ADLINK

- 9.4 Clearblade

- 9.5 Cloudera

- 9.6 Dell

- 9.7 Google

- 9.8 Gorilla Technology

- 9.9 Huawei

- 9.10 IBM

- 9.11 Intel

- 9.12 Microsoft

- 9.13 MediaTek

- 9.14 Mavenir System

- 9.15 Nutanix

- 9.16 Nvidia

- 9.17 Synaptics

- 9.18 Qualcomm

- 9.19 Veea

- 9.20 Xilinx