|

市場調査レポート

商品コード

1716674

産業用ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Industrial Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月26日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

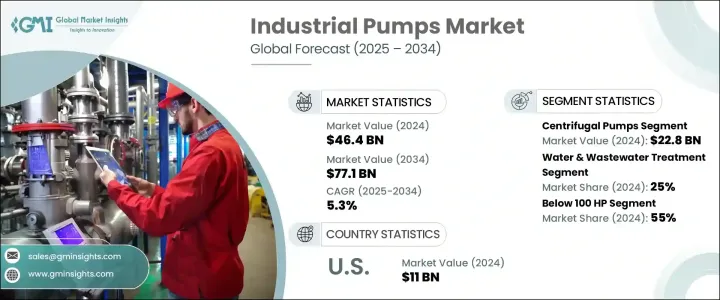

世界の産業用ポンプ市場は、2024年に464億米ドルと評価され、2025年から2034年にかけてCAGR 5.3%で成長すると予測されています。

この成長の主な要因は、様々な産業における需要の増加、ポンプシステムの技術進歩、世界の急速な工業化です。経済が拡大し、製造業が盛んになるにつれ、効率的で耐久性があり、高性能な産業用ポンプのニーズは高まり続けています。石油・ガス、水・廃水処理、鉱業、化学などの分野での用途が増加していることが、市場の成長に拍車をかけています。さらに、環境規制の高まりと相まって、持続可能な水管理手法への移行が、近代的でエネルギー効率の高いポンプへのニーズをさらに高めています。新興国市場、特にアジア太平洋とラテンアメリカでは、急速な都市化とインフラ開発への投資の増加により、産業用ポンプの需要が急増しています。スマートポンプ技術とIoT対応システムの採用が業界情勢を再構築しており、産業界は業務効率の向上とエネルギー消費の削減を実現しています。

市場は、遠心ポンプ、容積式ポンプ、ダイヤフラムポンプ、ギアポンプ、スクリューポンプ、その他を含むポンプタイプ別に区分されます。2024年、遠心ポンプ分野は、石油・ガス、水管理、化学処理などの産業で広く応用されているため、228億米ドルを生み出しました。容積式ポンプは、粘性の高い流体を効率的に処理することで知られており、水圧破砕における使用の増加や老朽化したインフラの更新によって、着実な成長が見込まれています。この動向は、特にエネルギー部門に多額の投資を行っている国々で顕著であり、高性能ポンプは採掘、精製、輸送プロセスの最適化に不可欠です。産業界が生産性の向上とダウンタイムの最小化に注力する中、信頼性と運転効率を提供する高度なポンプシステムに対する需要は高まり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 464億米ドル |

| 予測金額 | 771億米ドル |

| CAGR | 5.3% |

産業用ポンプ市場はさらに、上下水道処理、化学、石油化学、鉱業、食品・飲食品、建設、石油・ガス、医薬品、海洋、パルプ・製紙、その他など、最終用途産業別に区分されます。2024年の市場シェアは上下水道処理が25%を占めたが、これは急速な都市化と産業成長の中で清潔な水管理に対するニーズが高まっていることを反映しています。特に開発途上地域で人口が増加するにつれて、効率的な水処理と廃水管理ソリューションの必要性はますます高まっています。ポンプは鉱業でも重要な役割を果たしており、脱水ポンプは鉱山から余分な水を除去して安全性と操業効率を確保します。さらに、飲食品分野では、衛生的な処理と製品の完全性を維持するために、特殊なポンプに大きく依存しています。

米国の産業用ポンプ市場は80%のシェアを占め、2024年には110億米ドルを生み出します。この優位性は、技術の進歩、産業活動の拡大、持続可能な水管理への注目の高まりに起因します。米国の石油・ガス産業、特にシェールオイルの生産は、採掘、精製、輸送などのプロセスで幅広く使用される産業用ポンプの需要を大きく牽引しています。さらに、鉱業セクターの米国経済への貢献は、建設、自動車、航空宇宙などの産業に不可欠な材料を供給する重要な役割と相まって、産業用ポンプの堅調な需要をさらに支えています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因。

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 流通業者

- サプライヤーの情勢

- 技術的展望

- 主要ニュース&イニシアティブ

- 規制状況

- 影響要因

- 促進要因

- 最終用途産業からの需要の増加

- 世界の工業化と製造業の拡大

- 業界の潜在的リスク&課題

- 高い設備投資

- 高いエネルギー消費

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ポンプタイプ別、2021年~2034年

- 主要動向

- 渦巻きポンプ

- 容積式ポンプ

- ダイヤフラムポンプ

- 歯車ポンプ

- スクリューポンプ

- その他(ピストンポンプ、スネークポンプなど)

第6章 市場推計・予測:動力源別、2021年~2034年

- 主要動向

- 電気・ソーラーポンプ

- ディーゼルポンプ

- その他(ガソリンソーラーなど)

第7章 市場推計・予測:流量別、2021年~2034年

- 主要動向

- 100m³/h未満

- 100-500 m³/h

- 500m³/h以上

第8章 市場推計・予測:動力別、2021年~2034年

- 主要動向

- 100HP未満

- 100-500 HP

- 500HP以上

第9章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 従来型

- スマート

第10章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 上下水道処理

- 化学・石油化学

- 鉱業

- 飲食品

- 建設

- 石油・ガス

- 製薬

- 海洋

- パルプ・製紙

- その他(農業、繊維など)

第11章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第12章 地域別市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第13章 企業プロファイル

- Atlas Copco

- Ebara

- Flowserve

- Gardner Denver

- Gorman-Rupp

- Grundfos

- ITT

- Kirloskar

- KSB

- SPX Flow

- Sulzer

- Tsurumi

- Weir

- Wilo

- Xylem

The Global Industrial Pumps Market, valued at USD 46.4 billion in 2024, is projected to grow at a CAGR of 5.3% from 2025 to 2034. This growth is primarily driven by rising demand across various industries, technological advancements in pumping systems, and rapid industrialization worldwide. As economies expand and manufacturing sectors thrive, the need for efficient, durable, and high-performance industrial pumps continues to escalate. Increasing applications in sectors such as oil and gas, water and wastewater treatment, mining, and chemicals are fueling market growth. Moreover, the transition toward sustainable water management practices, coupled with rising environmental regulations, has further elevated the need for modern and energy-efficient pumps. Emerging markets, especially in Asia Pacific and Latin America, are witnessing surging demand for industrial pumps due to rapid urbanization and increasing investments in infrastructure development. The adoption of smart pump technologies and IoT-enabled systems is reshaping the landscape, allowing industries to improve operational efficiency and reduce energy consumption.

The market is segmented by pump type, including centrifugal pumps, positive displacement pumps, diaphragm pumps, gear pumps, screw pumps, and others. In 2024, the centrifugal pumps segment generated USD 22.8 billion, owing to its widespread application in industries such as oil and gas, water management, and chemical processing. Positive displacement pumps, known for their efficiency in handling viscous fluids, are expected to witness steady growth, driven by increasing use in hydraulic fracturing and the replacement of aging infrastructure. This trend is particularly noticeable in countries investing heavily in their energy sectors, where high-performance pumps are essential for optimizing extraction, refining, and transportation processes. As industries focus on enhancing productivity and minimizing downtime, the demand for advanced pumping systems that offer reliability and operational efficiency continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46.4 Billion |

| Forecast Value | $77.1 Billion |

| CAGR | 5.3% |

The industrial pumps market is further segmented by end-use industries, including water and wastewater treatment, chemicals, petrochemicals, mining, food and beverages, construction, oil and gas, pharmaceuticals, marine, pulp and paper, and others. Water and wastewater treatment accounted for a 25% market share in 2024, reflecting the growing need for clean water management amid rapid urbanization and industrial growth. As population increases, especially in developing regions, the need for efficient water treatment and wastewater management solutions continues to intensify. Pumps also play a critical role in the mining industry, where dewatering pumps remove excess water from mines to ensure safety and operational efficiency. Additionally, the food and beverage sector relies heavily on specialized pumps for hygienic processing and maintaining product integrity.

The United States Industrial Pumps Market commanded an 80% share, generating USD 11 billion in 2024. This dominance is attributed to technological advancements, growing industrial activity, and an increasing focus on sustainable water management. The U.S. oil and gas industry, particularly shale oil production, remains a significant driver of demand for industrial pumps, which are used extensively in processes such as extraction, refining, and transportation. Additionally, the mining sector's contributions to the U.S. economy, coupled with its critical role in supplying essential materials to industries like construction, automotive, and aerospace, further support the robust demand for industrial pumps.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Technological landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand from end use industries

- 3.6.1.2 Global industrialization and manufacturing expansion

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High capital investment

- 3.6.2.2 High energy consumption

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Pump Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Centrifugal pumps

- 5.3 Positive displacement pumps

- 5.4 Diaphragm pumps

- 5.5 Gear pumps

- 5.6 Screw pumps

- 5.7 Others (piston pumps, progressive cavity pumps, etc.)

Chapter 6 Market Estimates & Forecast, By Power Source, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Electric & solar pumps

- 6.3 Diesel pumps

- 6.4 Others (gasoline solar etc.)

Chapter 7 Market Estimates & Forecast, By Flow Rate, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Below 100 m³/h

- 7.3 100 - 500 m³/h

- 7.4 Above 500 m³/h

Chapter 8 Market Estimates & Forecast, By Power, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Below 100 HP

- 8.3 100 - 500 HP

- 8.4 Above 500 HP

Chapter 9 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Conventional

- 9.3 Smart

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Water & wastewater treatment

- 10.3 Chemicals and petrochemicals

- 10.4 Mining

- 10.5 Food and beverages

- 10.6 Construction

- 10.7 Oil & gas

- 10.8 Pharmaceutical

- 10.9 Marine

- 10.10 Pulp & paper

- 10.11 Others (agricultural, textile etc.)

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Indirect sales

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Atlas Copco

- 13.2 Ebara

- 13.3 Flowserve

- 13.4 Gardner Denver

- 13.5 Gorman-Rupp

- 13.6 Grundfos

- 13.7 ITT

- 13.8 Kirloskar

- 13.9 KSB

- 13.10 SPX Flow

- 13.11 Sulzer

- 13.12 Tsurumi

- 13.13 Weir

- 13.14 Wilo

- 13.15 Xylem