次世代空モビリティ(AAM)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Advanced Air Mobility Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716659

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

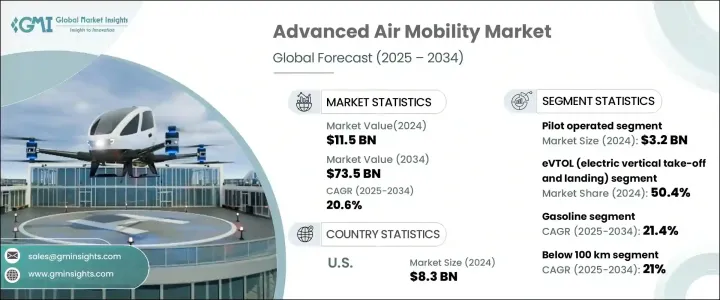

世界の次世代空モビリティ(AAM)市場は2024年に115億米ドルを生み出し、2025年から2034年にかけてCAGR 20.6%で成長すると予測されています。

世界が二酸化炭素排出量の削減と気候変動対策への取り組みを強化する中、輸送部門はよりクリーンなソリューションへの変革期を迎えています。次世代空モビリティ(AAM)は、交通渋滞を緩和し、輸送効率を高め、環境への影響を最小限に抑える持続可能な航空輸送オプションを提供する、ゲームチェンジャーとして台頭しつつあります。電気推進システム、自律走行技術、革新的な車両設計の統合が進み、AAMソリューションの採用が加速しています。

世界中の政府や規制当局は、有利な政策や投資を通じてこうした進歩を支援しており、AAM技術の迅速な認証と商業化を可能にしています。さらに、スマートシティの枠組みにAAMシステムを組み込むことに対する都市計画者や交通当局の関心の高まりが、市場の成長を促進しています。都市化が進み、より迅速で効率的な移動ソリューションへの需要が高まる中、AAMはシームレスなポイント・ツー・ポイントの輸送を提供することで、地域および都市のモビリティに革命を起こすと期待されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 115億米ドル |

| 予測金額 | 735億米ドル |

| CAGR | 20.6% |

2024年に32億米ドルと評価されるパイロットによる高度な航空モビリティ分野は、安全で信頼性の高い都市航空輸送を実現するために、人間の専門知識と技術革新を融合させることで、力強い成長を目の当たりにしています。パイロット付きAAM車両は、経験豊富なパイロットのスキルを活用することで安全性を高め、複雑な環境や人口密度の高い環境でもスムーズな運航を保証します。さらに、既存の航空インフラとの統合や、有利な規制枠組みの導入により、認証プロセスが迅速化され、これらの技術の迅速な展開と幅広い受け入れへの道が開かれつつあります。業界が自律的ソリューションに向かうなか、試験的なAAM車両は、社会的信頼を築き、運用プロセスを洗練させる橋渡し役を果たしています。

AAM市場は、電動垂直離着陸(eVTOL)機、短距離離着陸(STOL)機、従来の固定翼機など、車両タイプ別に分類されます。2024年には、電気およびハイブリッド推進システムの採用拡大により、eVTOL分野が市場シェアの50.4%を占めました。eVTOL航空機は、厳しい安全基準や運用基準を遵守しながら旅客輸送の要件を満たすことができるため、人気を集めています。eVTOL技術の開発は、次世代空モビリティ(AAM)の未来を形作る上で極めて重要な役割を果たすと予想されます。なぜなら、これらの航空機は、拡張可能でコスト効率が高く、環境的に持続可能な輸送ソリューションの可能性を提供するからです。

2024年に83億米ドルと評価される米国の先進的エアモビリティ市場は、強力な技術革新エコシステムと著名な航空宇宙企業の存在に後押しされた世界的リーダーとして位置づけられています。研究開発への多額の投資と、新技術を試験・展開するための確立されたインフラにより、米国はAAMソリューションの進歩と採用を推進しています。同国の積極的な規制環境は、官民の利害関係者間の継続的な協力と相まって、次世代空モビリティ(AAM)技術の商業化を加速させ、米国を世界のAAMランドスケープにおけるフロントランナーとして位置づけています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 都市化と交通渋滞

- 消費者の嗜好の変化

- 投資と政府支援

- 戦略的パートナーシップと提携

- 使用事例とアプリケーションの拡大

- 業界の潜在的リスク&課題

- 規制と安全性の課題

- 一般大衆の受容と認識

- 促進要因

- 成長の可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:運転モード別、2021年~2034年

- 主要動向

- パイロット操縦

- 自律/遠隔操作

第6章 市場推計・予測:車両タイプ別、2021年~2034年

- 主要動向

- eVTOL(電動垂直離着陸)機

- STOL(短距離離着陸)機

- 従来型固定翼機

第7章 市場推計・予測:推進タイプ別、2021年~2034年

- 主要動向

- ガソリンエンジン

- タービンエンジン(ターボ)

- 往復動(ピストン)エンジン

- 電気推進

- ハイブリッド推進

第8章 市場推計・予測:距離別、2021年~2034年

- 主要動向

- 100km未満

- 100 km-250 km

- 250 km-500 km

- 500km以上

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 貨物輸送

- 旅客輸送

- 地図作成・測量

- 特殊任務

- 監視・モニタリング

- その他

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 商業

- 政府・軍需

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- Airbus S.A.S.

- Aurora Flight Sciences

- Bell Textron Inc.

- Embraer S.A.

- Garmin Aviation

- GE Aviation

- GKN Aerospace

- Guangzhou EHang Intelligent Technology Co. Ltd.

- Honywell

- Joby Aviation

- Lilium GmbH

- Opener, Inc.

- Safran

- Siemens

- Thales Group

- The Boeing Company

目次

The Global Advanced Air Mobility Market generated USD 11.5 billion in 2024 and is projected to grow at a CAGR of 20.6% between 2025 and 2034. As the world intensifies its efforts to reduce carbon emissions and combat climate change, the transportation sector is undergoing a transformative shift toward cleaner solutions. Advanced air mobility is emerging as a game-changer, offering sustainable air transport options that reduce traffic congestion, enhance transportation efficiency, and minimize environmental impacts. The increasing integration of electric propulsion systems, autonomous technologies, and innovative vehicle designs is accelerating the adoption of AAM solutions.

Governments and regulatory authorities across the globe are supporting these advancements through favorable policies and investments, enabling rapid certification and commercialization of AAM technologies. Furthermore, the growing interest from urban planners and transportation authorities in incorporating AAM systems into smart city frameworks is driving market growth. With the rise of urbanization and increasing demand for faster and more efficient travel solutions, AAM is expected to revolutionize regional and urban mobility by offering seamless, point-to-point transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.5 Billion |

| Forecast Value | $73.5 Billion |

| CAGR | 20.6% |

The piloted advanced air mobility segment, valued at USD 3.2 billion in 2024, is witnessing robust growth as it blends human expertise with technological innovations to deliver safe and reliable urban air transportation. Piloted AAM vehicles offer an added layer of safety by leveraging the skills of experienced pilots, ensuring smooth operations even in complex or densely populated environments. Additionally, the integration of existing aviation infrastructure and the implementation of favorable regulatory frameworks are expediting the certification process, paving the way for faster deployment and wider acceptance of these technologies. As the industry moves toward autonomous solutions, piloted AAM vehicles are serving as a bridge to build public trust and refine operational processes.

The AAM market is categorized by vehicle types, including electric vertical take-off and landing (eVTOL) aircraft, short take-off and landing (STOL) aircraft, and conventional fixed-wing aircraft. In 2024, the eVTOL segment accounted for 50.4% of the market share, driven by the growing adoption of electric and hybrid propulsion systems. eVTOL aircraft are gaining traction due to their ability to meet passenger transportation requirements while adhering to stringent safety and operational standards. The development of eVTOL technology is expected to play a pivotal role in shaping the future of advanced air mobility, as these vehicles offer the potential for scalable, cost-effective, and environmentally sustainable transportation solutions.

The U.S. advanced air mobility market, valued at USD 8.3 billion in 2024, is positioned as a global leader fueled by a strong technological innovation ecosystem and the presence of prominent aerospace companies. With significant investments in research and development and a well-established infrastructure for testing and deploying new technologies, the U.S. is driving the advancement and adoption of AAM solutions. The country's proactive regulatory environment, combined with continuous collaboration between public and private sector stakeholders, is accelerating the commercialization of advanced air mobility technologies and positioning the U.S. as a frontrunner in the global AAM landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urbanization and traffic congestion

- 3.2.1.2 Changing consumer preferences

- 3.2.1.3 Investment and government support

- 3.2.1.4 Strategic partnerships and collaborations

- 3.2.1.5 Expansion of use cases and applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory and safety challenges

- 3.2.2.2 Public acceptance and perception

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Mode of Operation, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pilot operated

- 5.3 Autonomous/Remotely operated

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 eVTOL (Electric Vertical Takeoff and Landing) aircraft

- 6.3 STOL (Short Takeoff and Landing) aircraft

- 6.4 Conventional fixed-wing aircraft

Chapter 7 Market Estimates and Forecast, By Propulsion Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Gasoline

- 7.2.1 Turbine engines (Turbo)

- 7.2.2 Reciprocating (Piston) engines

- 7.3 Electric propulsion

- 7.4 Hybrid propulsion

Chapter 8 Market Estimates and Forecast, By Range, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Below 100 km

- 8.3 100 km – 250 km

- 8.4 250 km – 500 km

- 8.5 More than 500 km

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Cargo transport

- 9.3 Passenger transport

- 9.4 Mapping & surveying

- 9.5 Special mission

- 9.6 Surveillance & monitoring

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Commercial

- 10.3 Government & military

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Airbus S.A.S.

- 12.2 Aurora Flight Sciences

- 12.3 Bell Textron Inc.

- 12.4 Embraer S.A.

- 12.5 Garmin Aviation

- 12.6 GE Aviation

- 12.7 GKN Aerospace

- 12.8 Guangzhou EHang Intelligent Technology Co. Ltd.

- 12.9 Honywell

- 12.10 Joby Aviation

- 12.11 Lilium GmbH

- 12.12 Opener, Inc.

- 12.13 Safran

- 12.14 Siemens

- 12.15 Thales Group

- 12.16 The Boeing Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日