バス配車管理システムソフトウェア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Bus Dispatch Management System Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716636

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

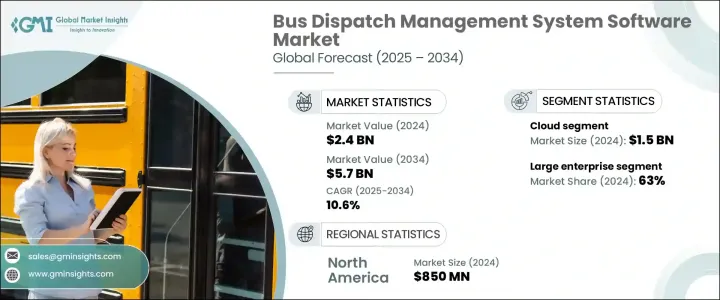

世界のバス配車管理システムソフトウェア市場は、2024年に24億米ドルと評価され、2025年から2034年にかけてCAGR 10.6%で成長すると予測されています。

同市場は、公共交通技術への投資の増加や効率的な車両管理ソリューションへのニーズの高まりを背景に、急速に拡大しています。都市人口の増加が続く中、交通機関や交通プロバイダーは、バス運行を最適化し、スケジューリングの精度を高め、車両全体の監視を合理化する先進的なソフトウェア・ソリューションに注目しています。公共交通インフラのデジタル化へのシフトは、世界中の都市がよりスマートで持続可能なモビリティ・ソリューションを優先する中で、需要をさらに加速させています。

都市化が進むにつれて、整備された信頼性の高い公共交通網の必要性が重要になっています。都市人口の急増は道路混雑と通勤者数の増加につながり、インテリジェントなバス配車管理システムの導入が必要となります。これらの先進的なプラットフォームは、リアルタイムのモニタリング、自動スケジューリング、AIを活用したルート最適化を可能にし、円滑な車両運行と通勤者の利便性向上を実現します。政府や民間交通機関は、遅延の削減、燃料効率の向上、運行コストの最小化を目指し、こうしたテクノロジーに積極的に投資しています。さらに、環境に優しくエコフレンドリーな輸送ソリューションの推進が高まっていることから、電気自動車やハイブリッド車の管理を統合したバス配車ソフトウェアの需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 57億米ドル |

| CAGR | 10.6% |

市場は主に導入モデルに基づいてセグメント化され、クラウドベースのソリューションとオンプレミスのソリューションが2大カテゴリーに分類されます。クラウドベースのソリューションがこのセグメントを支配し、2024年には15億米ドルを生み出し、2025年から2034年にかけてCAGR 11%で成長すると予測されています。クラウドベースの配車管理ソフトウェアは比類のないスケーラビリティを提供し、運送会社は規模に関係なく車両運行をシームレスに管理できます。これらのソリューションはリモートアクセスも可能で、フリートマネージャーや配車担当者はインターネット接続があればどこからでもリアルタイムのオペレーションを監視できます。クラウドベースのプラットフォームの柔軟性と費用対効果により、特に堅牢で将来性のあるソリューションを求める交通機関の間で広く採用されています。

市場を企業規模別に分析すると、大企業が圧倒的な地位を占めており、2024年の市場シェアの63%を占めています。多額の予算を持つ公共交通機関や多国籍バス事業者は、洗練されたバス配車管理ソフトウェアへの投資を続けています。これらの高度なシステムは、リアルタイム追跡、予測分析、AI主導の最適化ツールによって大規模な組織に力を与え、車両のパフォーマンスを向上させ、ダウンタイムを削減します。大規模な輸送業務における自動化ニーズの高まりは、乗客の安全性、業務効率、コスト管理の改善を求める企業の市場拡大をさらに後押ししています。

北米はバス配車管理システムソフトウェア市場を35%のシェアでリードし、2024年には8億5,000万米ドルを創出しました。同地域の市場プレゼンスが高いのは、スマートモビリティソリューションの採用が進んでいることと、運輸業務におけるAI、IoT、クラウドコンピューティングの統合が進んでいるためです。交通機関が車両管理戦略の近代化を続ける中、高度なバス配車ソフトウェアへの需要が急増し、今後数年間の市場成長をさらに促進すると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- ソフトウェア開発ベンダー

- ハードウェアプロバイダー

- システムインテグレーター

- 通信会社

- 交通機関/運行会社

- 利益率分析

- 価格動向

- 技術革新の状況

- 特許分析

- ケーススタディ

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 効率的な公共交通機関への需要の高まり

- 都市化の進展と人口増加

- 公共交通技術への投資の増加

- 自動車センサー技術の成長

- 業界の潜在的リスク&課題

- インターネット接続の制限とインフラの限界

- 従来の交通機関や利害関係者からの抵抗

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第6章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 大企業

- 中小企業

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ルート最適化

- リアルタイム追跡

- 車両管理

- 配車・通信

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 公共交通機関

- 民間バス事業者

- 教育機関

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- BusHive

- Cubic Transportation Systems

- Driver Schedule

- GIRO

- Goal Systems

- GPS Insight

- Hudson Software

- IBI Group

- INIT Innovations in Transportation

- Optibus

- Reveal Management Services

- Ride Systems

- Routematch Software

- Samsara Networks

- Syncromatics

- TransLoc

- Trapeze Group

- TripSpark Technologies

- Verizon Connect Reveal

- Zonar Systems

目次

The Global Bus Dispatch Management System Software Market was valued at USD 2.4 billion in 2024 and is projected to grow at a CAGR of 10.6% from 2025 to 2034. The market is experiencing rapid expansion, driven by increasing investments in public transport technology and the rising need for efficient fleet management solutions. With urban populations continuing to grow, transit agencies and transportation providers are turning to advanced software solutions that optimize bus operations, enhance scheduling accuracy, and streamline overall fleet monitoring. The shift toward digitized public transportation infrastructure is further accelerating demand as cities worldwide prioritize smarter, more sustainable mobility solutions.

As urbanization intensifies, the need for well-structured and reliable public transportation networks becomes critical. The surge in urban population results in increased road congestion and higher commuter volumes, necessitating the adoption of intelligent bus dispatch management systems. These advanced platforms enable real-time monitoring, automated scheduling, and AI-powered route optimization, ensuring smooth fleet operations and enhanced commuter experience. Governments and private transit agencies are actively investing in these technologies to reduce delays, improve fuel efficiency, and minimize operational costs. Additionally, the growing push for green and eco-friendly transit solutions is leading to an increased demand for bus dispatch software that integrates electric and hybrid vehicle management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 10.6% |

The market is primarily segmented based on deployment models, with cloud-based and on-premises solutions being the two major categories. Cloud-based solutions dominated the segment, generating USD 1.5 billion in 2024, and are expected to grow at a CAGR of 11% between 2025 and 2034. Cloud-based dispatch management software offers unparalleled scalability, allowing transportation agencies to seamlessly manage fleet operations regardless of size. These solutions also enable remote access, giving fleet managers and dispatchers the ability to monitor real-time operations from any location with internet connectivity. The flexibility and cost-effectiveness of cloud-based platforms have led to widespread adoption, particularly among transit agencies looking for robust and future-ready solutions.

When analyzing the market by enterprise size, large enterprises held a dominant position, accounting for 63% of the market share in 2024. Public transportation authorities and multinational bus operators with substantial budgets continue to invest in sophisticated bus dispatch management software. These advanced systems empower large organizations with real-time tracking, predictive analytics, and AI-driven optimization tools that enhance fleet performance and reduce downtime. The rising need for automation in large-scale transit operations further fuels market expansion as enterprises seek to improve passenger safety, operational efficiency, and cost management.

North America led the bus dispatch management system software market with a 35% share, generating USD 850 million in 2024. The region's strong market presence is attributed to the growing adoption of smart mobility solutions and the integration of AI, IoT, and cloud computing in transit operations. As transportation agencies continue to modernize their fleet management strategies, demand for advanced bus dispatch software is expected to surge, further driving market growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Software developers/vendors

- 3.2.2 Hardware providers

- 3.2.3 System integrators

- 3.2.4 Telecommunications companies

- 3.2.5 Transit agencies/operators

- 3.3 Profit margin analysis

- 3.4 Price trends

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Case study

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for efficient public transportation

- 3.10.1.2 Growing urbanization and population growth

- 3.10.1.3 Increasing investments in public transport technology

- 3.10.1.4 Rising growth of automotive sensor technology

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Limited internet connectivity and infrastructure limitations

- 3.10.2.2 Resistance from traditional transit agencies or stakeholders

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 On-premises

- 5.3 Cloud

Chapter 6 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Large enterprises

- 6.3 SME

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Route optimization

- 7.3 Real-time tracking

- 7.4 Fleet management

- 7.5 Dispatch and communication

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Public transit agencies

- 8.3 Private bus operators

- 8.4 Educational institutions

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 BusHive

- 10.2 Cubic Transportation Systems

- 10.3 Driver Schedule

- 10.4 GIRO

- 10.5 Goal Systems

- 10.6 GPS Insight

- 10.7 Hudson Software

- 10.8 IBI Group

- 10.9 INIT Innovations in Transportation

- 10.10 Optibus

- 10.11 Reveal Management Services

- 10.12 Ride Systems

- 10.13 Routematch Software

- 10.14 Samsara Networks

- 10.15 Syncromatics

- 10.16 TransLoc

- 10.17 Trapeze Group

- 10.18 TripSpark Technologies

- 10.19 Verizon Connect Reveal

- 10.20 Zonar Systems

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日