高電圧油絶縁開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

High Voltage Oil Insulated Switchgear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716625

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

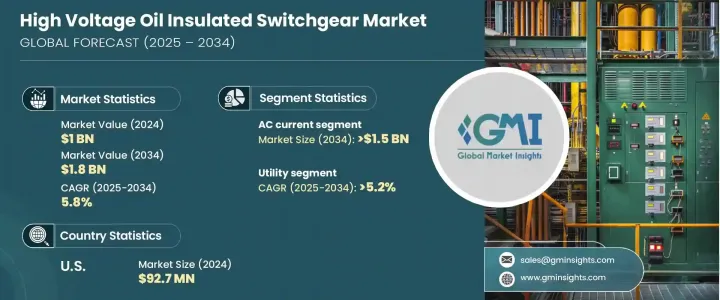

高電圧油絶縁開閉装置の世界市場は、2024年に10億米ドルと評価され、2025年から2034年にかけてCAGR 5.8%で成長すると予測されています。

この成長の原動力は、OISの優れた熱安定性、難燃性、優れた油絶縁耐力であり、特に油流出時の送配電システムの保護に重要な役割を果たしています。世界中の送電網が変貌を遂げるにつれ、信頼性の高い配電システムへの需要が高まっています。各国政府や電力会社は、送電網の信頼性を高め、送電ロスを減らし、停電を最小限に抑えるため、時代遅れの送電網インフラの改良に積極的に投資しています。さらに、特に急速な工業化と都市化を経験している新興経済国では、配電インフラを近代化する必要性が、高圧開閉器ソリューションの需要に拍車をかけています。

再生可能エネルギー源の統合が重視されるようになり、無停電電力供給への要求も高まっていることから、高圧送電網の拡大が進んでいます。油絶縁開閉装置は高圧回路の効率と安全性を維持するために不可欠であり、現代の電力システムには欠かせないものとなっています。電力会社や産業部門が送電ロスを最小限に抑え、信頼性の高い長距離送電を確保することを優先しているため、油絶縁開閉装置の採用は急増し続けています。さらに、送電網の近代化をめぐる厳しい規制や、電圧の安定性を維持する必要性が、市場の成長をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 10億米ドル |

| 予測金額 | 18億米ドル |

| CAGR | 5.8% |

AC送電システムが世界的に大電力送電に適した選択肢であり続けているため、ACセグメントの高電圧油絶縁開閉装置市場は、2034年までに15億米ドルを生み出すと予想されています。その経済的利点、簡素化された電圧調整、わかりやすい設計により、高圧用途に理想的なものとなっています。再生可能エネルギー発電施設、伝統的な発電所、その他のエネルギー生産設備など、ほとんどの発電源は交流形式で電気を供給しているため、電力フロー制御とシステムの安定性を確保する上で交流開閉装置の重要性が高まっています。世界のエネルギー消費量の増加に伴い、効率的な交流送電システムへの需要が高まり、様々な分野で油絶縁開閉装置の採用が進むと予想されます。

用途別では、さまざまな地域の公益事業者が既存の電気インフラの近代化に注力していることから、公益事業セグメントは2034年までCAGR 5.2%で成長すると予想されます。公益事業者は、送電網の信頼性を高め、送電ロスを減らすために多額の投資を行っており、油絶縁開閉装置は、その耐久性、高い絶縁耐力、高電圧を効率的に処理する能力により、依然として好ましい選択肢となっています。電力消費の増加と信頼性の高い長距離送電の必要性の高まりにより、公益事業部門による高圧システムへの投資が予測期間中の市場成長を促進すると予想されます。

米国の高電圧油絶縁開閉装置市場は、2024年に9,270万米ドルを生み出し、電力網の近代化に向けて取り組んでいることから継続的な成長が見込まれます。送電網の機能と効率を高める取り組みと、再生可能エネルギー源の統合を促進する取り組みが、旧式の開閉装置を高電圧油絶縁開閉装置に置き換える原動力となっています。米国市場の着実な成長は、進化するエネルギー需要に直面して、送電網の信頼性を向上させ、シームレスな配電を維持することにますます焦点が当てられていることを反映しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模と予測:電流別、2021年~2034年

- 主要動向

- 交流

- 直流

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 住宅

- 商業・工業

- ユーティリティ

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- Bharat Heavy Electricals

- CG Power and Industrial Solutions

- CHINT Group

- Eaton

- Fuji Electric

- General Electric

- HD Hyundai Electric

- Hitachi

- Hyosung Heavy Industries

- Lucy Group

- Mitsubishi Electric

- Ormazabal

- Schneider Electric

- Siemens

- Skema

- Toshiba

目次

The Global High Voltage Oil Insulated Switchgear Market was valued at USD 1 billion in 2024 and is projected to grow at a CAGR of 5.8% between 2025 and 2034. This growth is driven by the superior thermal stability, flame-resistant properties, and excellent oil dielectric strength of OIS, which play a crucial role in safeguarding transmission and distribution systems, especially during oil spills. As power grids worldwide undergo transformation, the demand for reliable power distribution systems is increasing. Governments and utility companies are actively investing in upgrading outdated grid infrastructure to enhance grid reliability, reduce transmission losses, and minimize power outages. Additionally, the need to modernize the power distribution infrastructure, particularly in emerging economies experiencing rapid industrialization and urbanization, is fueling demand for high-voltage switchgear solutions.

The rising emphasis on integrating renewable energy sources, along with the increasing requirement for uninterrupted power supply, has led to the expansion of high-voltage transmission networks. Oil-insulated switchgear is essential for maintaining the efficiency and safety of high-voltage circuits, making it indispensable in modern power systems. As utilities and industrial sectors prioritize minimizing transmission losses and ensuring reliable long-distance power delivery, the adoption of oil-insulated switchgear continues to surge. Furthermore, stringent regulations surrounding grid modernization and the need for maintaining voltage stability further propel market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $1.8 Billion |

| CAGR | 5.8% |

The high voltage oil insulated switchgear market from the AC segment is expected to generate USD 1.5 billion by 2034 as AC transmission systems remain the preferred choice for high-power transmission worldwide. Their economic advantages, simplified voltage regulation, and straightforward design make them ideal for high-voltage applications. Since most power generation sources, including renewable energy facilities, traditional power plants, and other energy production setups, provide electricity in AC form, the significance of AC switchgear in ensuring power flow control and system stability is heightened. As global energy consumption rises, the demand for efficient AC transmission systems is expected to boost the adoption of oil-insulated switchgear across various sectors.

Based on application, the utility segment is anticipated to grow at a CAGR of 5.2% through 2034 as utilities across various regions focus on modernizing their existing electrical infrastructure. Utilities are making substantial investments to enhance grid reliability and reduce transmission losses, and oil-insulated switchgear remains a preferred choice due to its durability, high dielectric strength, and ability to handle high voltages efficiently. With the rising consumption of electricity and the growing necessity for reliable long-distance power transmission, the utility sector's investment in high-voltage systems is expected to drive market growth over the forecast period.

The U.S. high voltage oil insulated switchgear market generated USD 92.7 million in 2024, with continued growth anticipated as the country works toward modernizing its power grids. Efforts to enhance grid functionality and efficiency, coupled with initiatives to encourage the integration of renewable energy sources, are driving the replacement of outdated switchgear with high-voltage oil-insulated alternatives. The steady growth of the U.S. market reflects an increasing focus on improving grid reliability and maintaining seamless power distribution in the face of evolving energy demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Current 2021 - 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 AC

- 5.3 DC

Chapter 6 Market Size and Forecast, By Application 2021 - 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial & industrial

- 6.4 Utility

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Bharat Heavy Electricals

- 8.3 CG Power and Industrial Solutions

- 8.4 CHINT Group

- 8.5 Eaton

- 8.6 Fuji Electric

- 8.7 General Electric

- 8.8 HD Hyundai Electric

- 8.9 Hitachi

- 8.10 Hyosung Heavy Industries

- 8.11 Lucy Group

- 8.12 Mitsubishi Electric

- 8.13 Ormazabal

- 8.14 Schneider Electric

- 8.15 Siemens

- 8.16 Skema

- 8.17 Toshiba

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日