|

市場調査レポート

商品コード

1716612

鋼鉄筋市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Steel Rebar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 鋼鉄筋市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月21日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

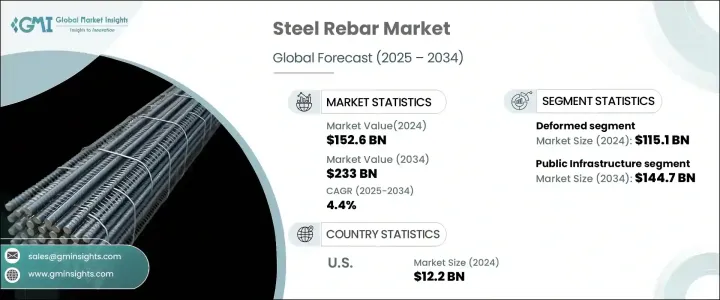

世界の鋼鉄筋市場は2024年に1,526億米ドルに達し、2025年から2034年にかけてCAGR 4.4%で成長すると予測されています。

この成長の主因は、特に新興経済諸国を中心としたインフラ開発への多額の投資です。各国が交通システムの近代化、都市部の拡大、公共事業の強化を続けているため、鉄筋のような信頼性の高い高強度材料の需要が急増し続けています。鉄筋はコンクリート構造物を補強し、その強度、安定性、寿命を向上させるために不可欠です。急速な都市化と人口増加は、住宅と商業部門の両方で建設活動の増加につながり、鉄筋の需要をさらに押し上げています。さらに、老朽化したインフラの改良と持続可能な建物の建設を目的とした政府の取り組みが、メーカーに有利な機会を生み出しています。鉄鋼製造における技術の進歩や、コンクリートとの結合を改善する革新的な鉄筋設計の導入も、耐久性があり弾力性のある構造物の建設を可能にし、市場の成長に寄与しています。

鋼鉄筋市場は、主に異形鉄筋と軟鋼鉄筋の2つに区分されます。明確な表面パターンによる優れた接着特性で知られる異形鉄筋は、2024年に1,151億米ドルを生み出し、2034年までCAGR 4.4%で成長すると予測されています。コンクリートへの接着力が強化されているため、滑りが最小限に抑えられ、構造安定性が大幅に向上します。このセグメントの優位性は、梁、柱、基礎などの鉄筋コンクリート構造物の建設に広く使用されていることに起因しています。高層ビル、橋梁、工業施設などの大規模インフラ・プロジェクトが拡大を続ける中、異形鉄筋の需要は引き続き堅調です。加えて、持続可能な建設手法の重視と耐震構造の必要性の高まりが、異形鉄筋の使用をさらに拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,526億米ドル |

| 予測金額 | 2,330億米ドル |

| CAGR | 4.4% |

用途別では、公共インフラ分野が2024年の市場シェア61.6%を占めました。数多くの国が、交通網、空港、橋梁などの大規模なインフラ・プロジェクトに投資しており、これらすべてが構造補強のために大量の鉄筋を必要としています。これらのプロジェクトは、環境ストレスに耐え、公共の安全を確保できる、長持ちし、耐久性のあるインフラを構築することを目的としています。インフラ近代化への強い焦点は、政府の支援イニシアティブと資金調達と相まって、公共インフラプロジェクトにおける高品質鉄筋の需要を煽っています。世界経済が都市景観の拡大や公共事業の改善に多額の投資を行う中、重要な構造物を強化する鉄筋への信頼は高まり続けています。

米国の鋼鉄筋市場は2024年に122億米ドルと評価され、道路、橋、公共交通システムなどの重要なインフラの建設とメンテナンスへの支出の増加によって着実な成長が予測されています。大規模な公共事業や民間建設プロジェクトに要求される厳しい品質基準を満たし、近代的なインフラの回復力と長寿命を確保するため、市場プレーヤーは製品提供の強化に注力しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 技術概要

- 規制状況

- 影響要因

- 促進要因

- 建設・不動産開発の増加

- 住宅の改築とリフォームの増加

- エネルギー効率の重視

- 都市化の進展と可処分所得の増加

- 業界の潜在的リスク&課題

- 原材料コストと価格変動

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 異形

- 軟鋼

第6章 市場推計・予測:プロセス別、2021年~2034年

- 主要動向

- ファンデーション酸素製鋼

- 電気炉

第7章 用途別市場推計・予測:用途別、2021~2034年

- 主要動向

- 住宅用建物

- 公共インフラ

- 産業

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Acerinox S.A

- ArcelorMittal

- Commercial Metals Company

- Daido Steel Co Ltd

- Gerdau S/A

- HBIS Group

- Jiangsu Shagang Group

- JSW

- NIPPON STEEL CORPORATION

- NLMK

- Nucor

- POSCO HOLDINGS INC.

- SAIL

- Steel Dynamics, Inc

- Tata Steel

The Global Steel Rebar Market reached USD 152.6 billion in 2024 and is projected to grow at a CAGR of 4.4% from 2025 to 2034. This growth is primarily driven by substantial investments in infrastructure development, particularly across emerging economies. As countries continue to modernize their transportation systems, expand urban areas, and enhance public utilities, the demand for reliable, high-strength materials such as steel rebar continues to surge. Steel rebar is essential for reinforcing concrete structures and improving their strength, stability, and longevity. Rapid urbanization and population growth have led to increased construction activities in both residential and commercial sectors, further boosting the demand for steel rebar. Moreover, government initiatives aimed at upgrading aging infrastructure and constructing sustainable buildings are creating lucrative opportunities for manufacturers. Technological advancements in steel manufacturing and the introduction of innovative rebar designs that improve bonding with concrete have also contributed to the market's growth, enabling the construction of durable and resilient structures.

The steel rebar market is segmented into two primary categories: deformed and mild steel rebar. Deformed steel rebar, known for its superior bonding properties due to its distinct surface patterns, generated USD 115.1 billion in 2024 and is projected to grow at a CAGR of 4.4% through 2034. Its enhanced adhesion to concrete minimizes slippage and significantly improves structural stability, making it the preferred choice in high-stress applications. This segment's dominance is attributed to its extensive use in the construction of reinforced concrete structures such as beams, columns, and foundations. As large-scale infrastructure projects, including high-rise buildings, bridges, and industrial facilities, continue to expand, the demand for deformed steel rebar remains robust. Additionally, the growing emphasis on sustainable construction practices and the need for earthquake-resistant structures are further amplifying the use of deformed steel rebar.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $152.6 Billion |

| Forecast Value | $233 Billion |

| CAGR | 4.4% |

In terms of application, the public infrastructure segment accounted for a 61.6% share of the market in 2024. Numerous countries are channeling investments into large-scale infrastructure projects such as transportation networks, airports, and bridges, all of which require significant quantities of steel rebar for structural reinforcement. These projects aim to create long-lasting, durable infrastructure that can withstand environmental stress and ensure public safety. The strong focus on infrastructure modernization, coupled with government-backed initiatives and funding, is fueling the demand for high-quality steel rebar in public infrastructure projects. As global economies invest heavily in expanding their urban landscapes and improving public utilities, the reliance on steel rebar to fortify critical structures continues to grow.

The U.S. steel rebar market was valued at USD 12.2 billion in 2024, with projections indicating steady growth driven by increased spending on the construction and maintenance of essential infrastructure, including roads, bridges, and public transportation systems. Government initiatives aimed at revitalizing the nation's infrastructure, combined with increased investments in building materials, are propelling the demand for steel rebar in the U.S. Market players are focusing on enhancing product offerings to meet the stringent quality standards required for large-scale public works and private construction projects, ensuring the resilience and longevity of modern infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technological overview

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising construction and real estate development

- 3.6.1.2 Increasing home renovation and remodeling

- 3.6.1.3 Focus on energy efficiency

- 3.6.1.4 Rising urbanization and rising disposable income

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Raw material costs and price volatility

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Million) (Million Tones)

- 5.1 Key trends

- 5.2 Deformed

- 5.3 Mild

Chapter 6 Market Estimates & Forecast, By Process, 2021-2034 (USD Million) (Million Tones)

- 6.1 Key trends

- 6.2 Basic oxygen steelmaking

- 6.3 Electric arc furnace

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Million Tones)

- 7.1 Key trends

- 7.2 Residential buildings

- 7.3 Public infrastructure

- 7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Million Tones)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Acerinox S.A

- 9.2 ArcelorMittal

- 9.3 Commercial Metals Company

- 9.4 Daido Steel Co Ltd

- 9.5 Gerdau S/A

- 9.6 HBIS Group

- 9.7 Jiangsu Shagang Group

- 9.8 JSW

- 9.9 NIPPON STEEL CORPORATION

- 9.10 NLMK

- 9.11 Nucor

- 9.12 POSCO HOLDINGS INC.

- 9.13 SAIL

- 9.14 Steel Dynamics, Inc

- 9.15 Tata Steel