|

市場調査レポート

商品コード

1716600

産業用ギアボックス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Industrial Gearbox Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用ギアボックス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

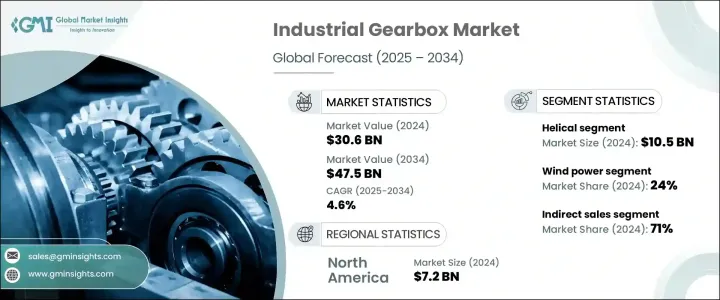

世界の産業用ギアボックス市場は2024年に306億米ドルに達し、2025年から2034年にかけてCAGR 4.6%で成長すると予測されています。

この成長は、多様なセクターで産業オートメーションの採用が増加していることと、ギアボックス技術の継続的な進歩が原動力となっています。産業用ギアボックスは、CNCマシン、ロボット、コンベアシステム、組立ラインなどの自動化アプリケーションで重要な役割を果たしています。これらのシステムでは、正確な動力伝達を確保するためにコンパクトな設計を維持しながら、高トルクを実現するギアボックスが必要です。産業界全体における大型機械の需要の高まりが、市場の拡大をさらに加速させています。インフラ、公共事業、建設のニーズが世界的に高まっていることも、建設機械における産業用ギアボックスドライブの需要を促進しています。ギアボックスは、クレーン、リフト、ホイスト、マテリアルハンドリング機器に不可欠であり、要求の厳しい用途で高い信頼性と耐久性を提供します。

2024年、産業用ギアボックス市場のヘリカルセグメントは105億米ドルを占めました。プラネタリーセグメントは、2025年から2034年にかけて約5%のCAGRで成長すると予測されています。ヘリカルギアは、滑らかな動作、耐久性、高負荷への対応能力で知られ、自動車、航空宇宙、産業機械、ロボットなどの産業で広く利用されています。自動車産業は、特にオートマチックトランスミッション車の生産が増加し、電気自動車(EV)へのシフトが進んでいることから、ヘリカルギアの重要な需要源となっています。航空宇宙産業も、過酷な条件下でも効果的に機能するヘリカルギアに依存しており、飛行、ドローン、宇宙アプリケーションでの使用に理想的です。アジア太平洋地域は、中国、日本、インドといった国々が主要なサプライヤーとなっており、自動車製造の基盤が強固であることから、ヘリカルギアの需要をリードしています。欧州も、代替動力と高度な自動車技術に重点を置いているため、極めて重要な役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 306億米ドル |

| 予測金額 | 475億米ドル |

| CAGR | 4.6% |

風力発電分野は、クリーンで再生可能なエネルギー源に対する需要の増加に牽引され、2024年には産業用ギアボックス市場の約24%を占めました。過酷な環境条件に耐えられる高容量で効率的なギアボックスを必要とする洋上風力発電所が、この成長に拍車をかけています。倉庫業や物流業などの産業における自動化の採用は、コンベヤシステムや自動機械における安全で効率的なギアボックスの需要をさらに押し上げています。電気自動車の人気の高まりもギアボックスの需要を変化させており、EVは高トルクに対応し、エネルギーを効率的に伝達する特殊なギアボックスを必要としています。

2024年には、間接販売が流通チャネルの大半を占め、市場シェアの71%以上を占める。企業は通常、カスタマイズや大量購入が不可欠な大規模な産業用アプリケーションでは、直接販売チャネルを好みます。一方、中小企業は、さまざまなブランドの多種多様なギアボックスを在庫している産業機器販売業者からの購入を好みます。装置や機械に特殊なギアボックスが必要な場合は、OEMからギアボックスを調達する企業もあります。

北米では、米国が2024年の産業用ギアボックス市場をリードし、地域別市場シェアの約80%を占め、推定72億米ドルの収益を上げました。米国市場の拡大には、ギアボックス技術の進歩、複数の産業からの需要の高まり、特殊ギアボックスへの関心の高まりが寄与しています。製造業やエネルギー産業などにおける自動化の進展が効率的なギアボックスの需要を促進し、再生可能エネルギー、特に風力発電への投資が市場成長の機会を生み出し続けています。自動車分野でのEVの台頭は、ドライブラインやステアリングシステムにおける小型で高トルクのギアボックスのニーズの増加にさらに貢献しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 流通業者

- サプライヤーの情勢

- 技術的展望

- 主要ニュース&イニシアティブ

- 規制状況

- 影響要因

- 促進要因

- 様々な分野における産業オートメーションの台頭

- ギアボックス技術全般の進歩

- 業界の潜在的リスク&課題

- 高いメンテナンス要件

- ギアの摩耗と故障

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ヘリカル

- ベベル

- ウォーム

- プラネタリ

- その他(スパー、スパイラルなど)

第6章 市場推計・予測:動力別、2021年~2034年

- 主要動向

- 小型(500kW未満)

- 中型(500kW~10MW)

- 大型(10MW以上)

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 風力発電

- マテリアルハンドリング

- 建設

- 海洋

- エネルギー

- 輸送

- その他(農業、鉱業など)

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Abex Corporation

- Bonfiglioli

- Davall Gears

- Elecon Engineering

- Flender

- HJ Corporation

- Ishibashi Manufacturing

- Kissling

- Nippon Gear

- Premium Transmission

- Schaeffler

- Stober Antriebstechnik

- Sumitomo Heavy Industries

- WM Berg

- ZF Friedrichshafen

The Global Industrial Gearbox Market reached USD 30.6 billion in 2024 and is projected to grow at a CAGR of 4.6% from 2025 to 2034. This growth is driven by the increasing adoption of industrial automation across diverse sectors and the continuous advancement in gearbox technology. Industrial gearboxes play a crucial role in automated applications such as CNC machines, robots, conveyor systems, and assembly lines. These systems require gearboxes that deliver high torque while maintaining compact designs to ensure accurate power transmission. The rising demand for heavy-duty machinery across industries further accelerates market expansion. The growing need for infrastructure, public works, and construction globally has also fueled the demand for industrial gearbox drives in construction machinery. Gearboxes are essential in cranes, lifts, hoists, and material-handling equipment, providing high reliability and durability in demanding applications.

In 2024, the helical segment of the industrial gearbox market accounted for USD 10.5 billion. The planetary segment is anticipated to grow at a CAGR of approximately 5% from 2025 to 2034. Helical gears, known for their smooth operation, durability, and capacity to handle high loads, are widely utilized in industries such as automotive, aerospace, industrial machinery, and robotics. The automotive industry, particularly with the growing production of automatic transmission vehicles and the increasing shift toward electric vehicles (EVs), is a significant source of demand for helical gears. The aerospace industry also relies on helical gears for their ability to function effectively in harsh conditions, making them ideal for use in flights, drones, and space applications. Asia Pacific leads the demand for helical gears, driven by its strong automobile manufacturing base, with countries like China, Japan, and India serving as major suppliers. Europe also plays a pivotal role due to its focus on alternative power and advanced automotive technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.6 Billion |

| Forecast Value | $47.5 Billion |

| CAGR | 4.6% |

The wind power segment accounted for approximately 24% of the industrial gearbox market in 2024, driven by increasing demand for clean and renewable energy sources. Offshore wind farms, which require high-capacity and efficient gearboxes capable of withstanding harsh environmental conditions, have fueled this growth. The adoption of automation in industries such as warehousing and logistics has further boosted the demand for secure and effective gearboxes in conveyor systems and automated machinery. The growing popularity of electric cars has also transformed gearbox demand, as EVs require specialized gearboxes that support high torque and transmit energy efficiently.

In 2024, indirect sales dominated the distribution channel, accounting for over 71% of the market share. Companies typically prefer direct distribution channels for large-scale industrial applications where customization and bulk purchases are essential. Meanwhile, small and medium-sized enterprises prefer purchasing from industrial equipment distributors who stock a wide variety of gearboxes from different brands. Some companies source gearboxes from OEMs when specialized gearboxes are needed for equipment or machinery.

In North America, the United States led the industrial gearbox market in 2024, holding around 80% of the regional market share and generating an estimated USD 7.2 billion in revenue. The US market's expansion is fueled by advancements in gearbox technology, rising demand from multiple industries, and growing interest in specialized gearboxes. Increasing automation in industries like manufacturing and energy has driven demand for efficient gearboxes, while investments in renewable energy, particularly wind power, continue to create opportunities for market growth. The rise of EVs in the automotive sector further contributes to the increasing need for compact, high-torque gearboxes in driveline and steering systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Technological landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rise of industrial automation across various sectors

- 3.6.1.2 Advancement in overall gearbox technology

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High maintenance requirement

- 3.6.2.2 Gear wear and failure

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Helical

- 5.3 Bevel

- 5.4 Worm

- 5.5 Planetary

- 5.6 Others (spur, spiral, etc.)

Chapter 6 Market Estimates & Forecast, By Power, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Small (up to 500 kW)

- 6.3 Medium (500 kW to 10 MW)

- 6.4 Large (above 10 MW)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Wind power

- 7.3 Material handling

- 7.4 Construction

- 7.5 Marine

- 7.6 Energy

- 7.7 Transportation

- 7.8 Others (agriculture, mining etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Abex Corporation

- 10.2 Bonfiglioli

- 10.3 Davall Gears

- 10.4 Elecon Engineering

- 10.5 Flender

- 10.6 HJ Corporation

- 10.7 Ishibashi Manufacturing

- 10.8 Kissling

- 10.9 Nippon Gear

- 10.10 Premium Transmission

- 10.11 Schaeffler

- 10.12 Stober Antriebstechnik

- 10.13 Sumitomo Heavy Industries

- 10.14 WM Berg

- 10.15 ZF Friedrichshafen