前立腺がん治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Prostate Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716597

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

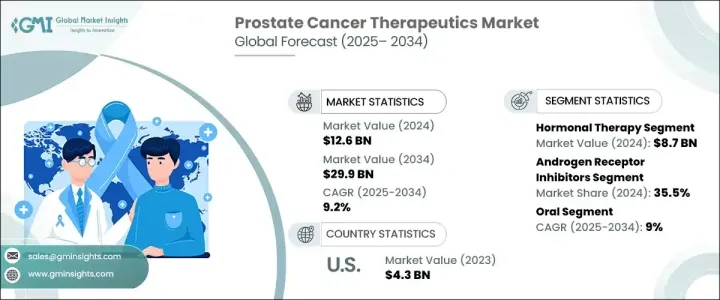

世界の前立腺がん治療市場は、2024年に126億米ドルを生み出し、2025年から2034年にかけてCAGR 9.2%で拡大すると予測されています。

同市場は、早期診断と効果的な治療オプションに関する意識の高まりと相まって、世界の前立腺がんの有病率の増加を主な要因として、大きな勢いを見せています。前立腺がんは男性に最も多いがんのひとつであり、ヘルスケアシステムは患者の予後を改善するために先進的な治療薬の導入に注力しています。男性人口の高齢化、罹患率の上昇、政府主導の取り組みやがん擁護団体を通じた患者意識の高まりは、引き続き市場の成長を促進しています。

さらに、精密医療の革新と、ゲノム検査、バイオマーカー同定、AI搭載画像診断などの高度診断ツールの統合が、前立腺がんの発見と治療計画に革命をもたらしています。製薬大手は、前立腺がんの耐性型を効果的に標的とすることができる新規薬剤や個別化療法を導入するための研究開発に多額の投資を行っており、病期が進行した患者に新たな希望をもたらしています。さらに、併用療法や免疫療法の採用が重視されるようになったことで、より安全で効率的な治療法への道が開かれ、治療の展望が大きく変わりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 126億米ドル |

| 予測金額 | 299億米ドル |

| CAGR | 9.2% |

市場は、ホルモン療法、化学療法、免疫療法、標的療法、その他の治療法など、さまざまな治療アプローチに基づいて区分されます。2024年には、ホルモン療法が市場を牽引し、87億米ドルの売上を計上しました。ホルモン療法は、アンドロゲンホルモンレベルを低下させることで、疾患の進行を抑制するという重要な役割を果たすため、前立腺がん管理の要であり続けています。これらのホルモン、特にテストステロンは、前立腺がんの成長を促進することが知られています。テストステロン産生を標的にして抑制することにより、ホルモン療法は腫瘍の大きさを著しく縮小し、症状を緩和し、患者の生存率向上に寄与します。進行症例や耐性症例により有効な次世代ホルモン剤の採用が増加していることが、世界市場におけるこの治療セグメントの優位性をさらに強固なものにしています。

薬剤クラス別では、アンドロゲン受容体阻害薬(ARI)が2024年の市場シェアの35.5%を占めています。ARIは、進行前立腺がん患者、特に従来のアンドロゲン除去療法(ADT)に反応しなくなった患者にとって重要な治療選択肢として浮上してきました。これらの阻害剤は、アンドロゲン受容体のシグナル伝達経路を遮断することにより作用し、がん細胞がアンドロゲンを利用して増殖するのを阻害します。早期および後期前立腺がん治療におけるARIの使用増加により、臨床転帰が改善され、現在の治療薬として不可欠なものとなっています。有効性と安全性のプロファイルが強化された新しいARIの導入も、今後数年間のARIの採用を後押しすると予想されます。

世界の前立腺がん治療市場は、2024年には北米が39.2%のシェアを占めました。同地域の主導的地位は、高度なヘルスケアインフラ、最先端のがん治療センター、腫瘍学研究への強力な注力によるところが大きいです。高水準の公的・私的投資、製薬会社と研究機関の共同努力が、この地域全体の前立腺がん治療の技術革新を継続的に推進しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 前立腺がんの有病率の増加

- 技術の進歩

- 意識の高まりとスクリーニングプログラム

- 業界の潜在的リスク&課題

- 高額な治療費

- 治療に伴う副作用

- 促進要因

- 成長可能性分析

- 規制状況

- 償還シナリオ

- パイプライン分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:治療別、2021年~2034年

- 主要動向

- ホルモン療法

- 化学療法

- 免疫療法

- 標的療法

- その他の療法

第6章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- アンドロゲン受容体阻害薬

- GnRH受容体拮抗薬

- PARP阻害薬

- 免疫チェックポイント阻害薬

- その他の薬剤クラス別

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口剤

- 注射剤

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 実店舗

- eコマース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Astellas Pharma

- AstraZeneca

- Bayer

- Dendreon Pharmaceuticals

- Exelixis

- Ferring

- GlaxoSmithKline

- Ipsen Pharma

- Johnson &Johnson

- Novartis

- Pfizer

- Sanofi

- Sumitomo Pharma America

- Takeda Pharmaceutical

- Tolmar

目次

The Global Prostate Cancer Therapeutics Market generated USD 12.6 billion in 2024 and is projected to expand at a CAGR of 9.2% from 2025 to 2034. The market is witnessing significant momentum, primarily driven by the growing prevalence of prostate cancer worldwide, coupled with increasing awareness around early diagnosis and effective treatment options. With prostate cancer ranking among the most common cancers in men, healthcare systems are focusing on adopting advanced therapeutics to improve patient outcomes. The aging male population, rising incidence rates, and a surge in patient awareness through government-led initiatives and cancer advocacy groups continue to foster market growth.

Moreover, innovations in precision medicine and the integration of advanced diagnostic tools like genomic testing, biomarker identification, and AI-powered imaging are revolutionizing prostate cancer detection and treatment planning. Pharmaceutical giants are heavily investing in research and development to introduce novel drugs and personalized therapies that can effectively target resistant forms of prostate cancer, offering renewed hope for patients with advanced disease stages. Additionally, the increased emphasis on combination therapies and the adoption of immunotherapies are transforming the therapeutic landscape, making way for safer and more efficient treatment modalities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.6 Billion |

| Forecast Value | $29.9 Billion |

| CAGR | 9.2% |

The market is segmented based on different therapeutic approaches, including hormonal therapy, chemotherapy, immunotherapy, targeted therapy, and other treatment options. In 2024, hormonal therapy led the market, generating USD 8.7 billion in revenue. Hormonal therapy remains a cornerstone in prostate cancer management as it plays a crucial role in controlling the disease's progression by lowering androgen hormone levels. These hormones, especially testosterone, are known to fuel prostate cancer growth. By targeting and suppressing testosterone production, hormonal therapies significantly reduce tumor size and alleviate symptoms, which contributes to improved patient survival rates. The growing adoption of next-generation hormonal agents that are more effective in advanced and resistant cases has further cemented the dominance of this therapeutic segment in the global market.

Based on drug classes, androgen receptor inhibitors (ARIs) accounted for 35.5% of the market share in 2024. ARIs have emerged as a vital treatment option for patients with advanced prostate cancer, especially those who no longer respond to traditional androgen deprivation therapy (ADT). These inhibitors work by blocking the androgen receptor signaling pathway, thereby preventing cancer cells from utilizing androgens for growth. The increased use of ARIs in both early and late-stage prostate cancer treatment has shown improved clinical outcomes, making them indispensable in the current therapeutic arsenal. The introduction of new ARIs with enhanced efficacy and safety profiles is also expected to boost their adoption over the coming years.

North America dominated the global prostate cancer therapeutics market with a 39.2% share in 2024. The region's leadership position is largely attributed to its advanced healthcare infrastructure, cutting-edge cancer care centers, and strong focus on oncology research. High levels of public and private investments, along with collaborative efforts between pharmaceutical companies and research institutions, are continuously propelling innovation in prostate cancer treatment across the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of prostate cancer

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects associated with treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hormonal therapy

- 5.3 Chemotherapy

- 5.4 Immunotherapy

- 5.5 Targeted therapy

- 5.6 Other therapies

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Androgen receptor inhibitors

- 6.3 GnRH receptor antagonists

- 6.4 PARP inhibitors

- 6.5 Immune checkpoint inhibitors

- 6.6 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Brick and mortar

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Astellas Pharma

- 10.2 AstraZeneca

- 10.3 Bayer

- 10.4 Dendreon Pharmaceuticals

- 10.5 Exelixis

- 10.6 Ferring

- 10.7 GlaxoSmithKline

- 10.8 Ipsen Pharma

- 10.9 Johnson & Johnson

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sumitomo Pharma America

- 10.14 Takeda Pharmaceutical

- 10.15 Tolmar

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日