ビデオインターホン機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Video Intercom Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716592

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

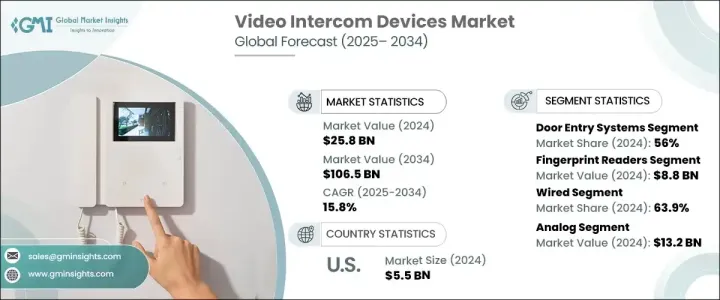

ビデオインターホン機器の世界市場は、2024年には258億米ドルとなり、2025年から2034年にかけてCAGR 15.8%で成長すると予測されています。

市場の急成長は、高度なホームセキュリティシステムに対する需要の高まりと、ワイヤレス通信技術における技術革新の高まりが原動力となっています。消費者の安全に対する関心が高まり、スマート・ホーム・セキュリティ・ソリューションの需要が高まっています。可処分所得の増加とホームセキュリティの研究開発への投資の増加が、これらのシステムの世界の普及をさらに促進しています。AIとスマートホーム技術の統合により、より効率的で安全、かつユーザーフレンドリーなシステムが実現し、ビデオインターホン機器の魅力が高まっています。クラウドベースやワイヤレスのセキュリティー・システムの人気が高まるにつれ、消費者は従来のソリューションから、リアルタイムの通知やモバイル機器による遠隔操作を提供するシステムの採用へとシフトしています。都市部への移住が加速し、共働き家庭が遠隔監視システムを求めるようになるにつれ、インテリジェントなセキュリティ・ソリューションへの需要は高まり続けています。

市場は、デバイスのタイプ別に、ハンドヘルド・デバイス、ドアエントリー・システム、ビデオ・ベビーモニターに区分されます。ドアエントリーシステムセグメントは、住宅や商業ビルにおける高度なセキュリティ機能へのニーズの高まりにより、2024年に世界のビデオインターホン機器市場の56%を獲得しました。IoTとAIベースの入退室管理システムの統合により、ユーザーの本人確認、遠隔管理、継続的な監視が可能になり、セキュリティが強化されています。増大するセキュリティ脅威に対処するためのスマートセキュリティソリューションへの注目の高まりが、ドアエントリーシステムの採用を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 258億米ドル |

| 予測金額 | 1,065億米ドル |

| CAGR | 15.8% |

アクセス制御の分野では、市場は指紋リーダー、パスワードアクセス、近接カード、無線アクセスに分けられます。指紋リーダー分野は、バイオメトリクス・セキュリティ・システムへの嗜好の高まりを反映して、2024年の市場規模は88億米ドルとなりました。住宅、商業、工業環境においてセキュリティへの関心が高まるにつれ、不動産所有者は、その信頼性、使いやすさ、不正アクセスを防止する能力から、バイオメトリックベースの制御システムを選ぶようになっています。指紋リーダーは非接触、高速、安全な認証を提供し、クレデンシャルの盗難や誤用のリスクを低減します。AIと指紋認証、クラウドベースのアクセス、モバイル認証の統合は、これらのシステムのセキュリティと利便性をさらに高める。

市場はシステムタイプ別に有線と無線に二分されます。有線セグメントは2024年に市場シェアの63.9%を占めました。高セキュリティ環境では、サイバー脅威に対する信頼性と回復力から有線ソリューションが好まれるためです。政府施設、軍事基地、重要なインフラサイトでは、最大限のセキュリティが要求され、有線システムは、無線の代替品と比較して、データ侵害やシステム中断に対する保護に優れています。

技術セグメントはアナログとIPベースのシステムに分けられます。アナログ・セグメントは、低帯域幅環境での信頼性により、2024年に132億米ドルを占める。インターネット接続に依存するIPベースのシステムとは異なり、アナログシステムは独立して動作するため、ブロードバンドの普及が制限されている古い建物や農村部に最適です。

最終用途別では、市場は自動車、商業、政府、住宅、その他に区分されます。商業セグメントは、スマートオフィスやコワーキングスペースにおける自動アクセス制御の需要増が牽引し、2024年には93億米ドルで市場をリードしました。IoTベースのオフィス環境の採用が増加したことで、非接触エントリー、訪問者記録、ビデオインターホンシステムによるセキュリティ向上のニーズが高まっています。2024年、米国市場は55億米ドルを占め、IoT、AI、クラウドベースの監視システムを統合し、住宅のセキュリティを向上させる洗練されたホームセキュリティソリューションへの需要が高まっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- ホームセキュリティシステムの需要増加

- 無線通信技術の進歩

- スマートホームの普及

- 都市化と集合住宅の増加

- IoTやオートメーションとの統合

- 業界の潜在的リスク&課題

- 高い初期導入費用とメンテナンス費用

- プライバシーとデータセキュリティへの懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:デバイスタイプ別、2021年~2034年

- 主要動向

- ドアエントリーシステム

- ハンドヘルド機器

- ビデオベビーモニター

第6章 市場推計・予測:アクセスコントロール別、2021年~2034年

- 主要動向

- 指紋リーダー

- パスワードアクセス

- 近接カード

- 無線アクセス

第7章 市場推計・予測:システム別、2021年~2034年

- 主要動向

- 有線

- ワイヤレス

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- アナログ

- IPベース

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 自動車

- 商業

- 官公庁

- 住宅

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ABB Ltd

- Aiphone

- Axis Communications AB

- ButterflyMX Inc.

- Comelit Group

- Commend International GmbH

- Dahua Technologies Co. Ltd

- Doorbird

- Fermax

- Godrej &Boyce Mfg. Co. Ltd.

- Hangzhou Hikvision Digital Technology Co. Ltd

- Honeywell

- KOCOM Co., Ltd.

- Legrand

- Mivanta

- MOX Group Limited

- Panasonic Holdings Corporation

- Ring

- Siedle &Sohne OHG

- Xiamen Leelen Technology Co., Ltd

- Zicom

- ZKTeco

目次

The Global Video Intercom Devices Market was valued at USD 25.8 billion in 2024 and is anticipated to grow at a CAGR of 15.8% from 2025 to 2034. The rapid growth of the market is driven by the increasing demand for advanced home security systems and rising innovations in wireless communication technology. Consumers are more concerned about safety, leading to a higher demand for smart home security solutions. Rising disposable income and growing investments in research and development for home security have further fueled the adoption of these systems globally. The integration of AI with smart home technologies has enabled more efficient, secure, and user-friendly systems, enhancing the appeal of video intercom devices. With the increasing popularity of cloud-based and wireless security systems, consumers are shifting away from conventional solutions to adopt systems that offer real-time notifications and remote control through mobile devices. As urban migration accelerates and dual-income families seek remote surveillance systems, demand for intelligent security solutions continues to rise.

The market is segmented by device type into handheld devices, door entry systems, and video baby monitors. The door entry systems segment captured 56% of the global video intercom devices market in 2024, driven by the increasing need for advanced security features in residential and commercial buildings. Integration of IoT and AI-based access control systems has enhanced security by enabling user identity verification, remote management, and continuous surveillance. The growing focus on smart security solutions to address rising security threats is boosting the adoption of door entry systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.8 Billion |

| Forecast Value | $106.5 Billion |

| CAGR | 15.8% |

By access control, the market is divided into fingerprint readers, password access, proximity cards, and wireless access. The fingerprint readers segment was valued at USD 8.8 billion in 2024, reflecting the increasing preference for biometric security systems. As security concerns grow in residential, commercial, and industrial settings, property owners are opting for biometric-based control systems due to their reliability, ease of use, and ability to prevent unauthorized access. Fingerprint readers offer contactless, fast, and secure authentication, reducing the risk of credential theft or misuse. The integration of AI with fingerprint recognition, cloud-based access, and mobile authentication further enhances the security and convenience of these systems.

The market is bifurcated by system type into wired and wireless. The wired segment held 63.9% of the market share in 2024, as high-security environments favor wired solutions due to their reliability and resilience against cyber threats. Government facilities, military bases, and critical infrastructure sites require maximum security, and wired systems offer better protection against data breaches and system disruptions compared to wireless alternatives.

The technology segment is divided into analog and IP-based systems. The analog segment accounted for USD 13.2 billion in 2024 due to its reliability in low-bandwidth environments. Unlike IP-based systems that rely on internet connectivity, analog systems operate independently, making them ideal for older buildings and rural areas where broadband penetration is limited.

By end use, the market is segmented into automotive, commercial, government, residential, and others. The commercial segment led the market with USD 9.3 billion in 2024, driven by the rising demand for automated access control in smart offices and co-working spaces. Increased adoption of IoT-based office environments has fueled the need for contactless entry, visitor logging, and improved security through video intercom systems. In 2024, the US market accounted for USD 5.5 billion, with growing demand for sophisticated home security solutions that integrate IoT, AI, and cloud-based monitoring systems to improve residential security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for home security systems

- 3.6.1.2 Advancements in wireless communication technology

- 3.6.1.3 Rising adoption in smart homes

- 3.6.1.4 Growing urbanization and residential complexes

- 3.6.1.5 Integration with IoT and automation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial installation and maintenance costs

- 3.6.2.2 Privacy and data security concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Device Type, 2021-2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Door entry systems

- 5.3 Handheld devices

- 5.4 Video baby monitors

Chapter 6 Market Estimates & Forecast, By Access control, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Fingerprint readers

- 6.3 Password access

- 6.4 Proximity cards

- 6.5 Wireless access

Chapter 7 Market Estimates & Forecast, By System, 2021-2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Wired

- 7.3 Wireless

Chapter 8 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Analog

- 8.3 IP-based

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Commercial

- 9.4 Government

- 9.5 Residential

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABB Ltd

- 11.2 Aiphone

- 11.3 Axis Communications AB

- 11.4 ButterflyMX Inc.

- 11.5 Comelit Group

- 11.6 Commend International GmbH

- 11.7 Dahua Technologies Co. Ltd

- 11.8 Doorbird

- 11.9 Fermax

- 11.10 Godrej & Boyce Mfg. Co. Ltd.

- 11.11 Hangzhou Hikvision Digital Technology Co. Ltd

- 11.12 Honeywell

- 11.13 KOCOM Co., Ltd.

- 11.14 Legrand

- 11.15 Mivanta

- 11.16 MOX Group Limited

- 11.17 Panasonic Holdings Corporation

- 11.18 Ring

- 11.19 Siedle & Sohne OHG

- 11.20 Xiamen Leelen Technology Co., Ltd

- 11.21 Zicom

- 11.22 ZKTeco

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日