|

市場調査レポート

商品コード

1716591

IoTマイクロコントローラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測IoT Microcontroller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| IoTマイクロコントローラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月19日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

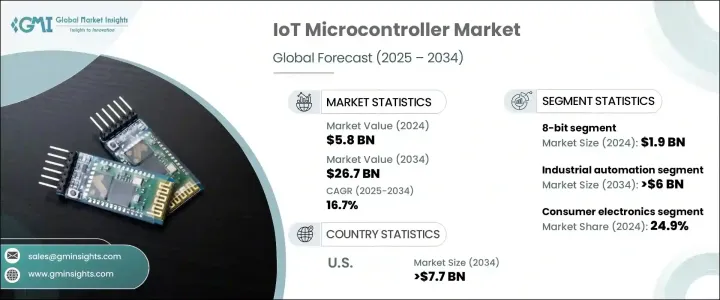

IoTマイクロコントローラの世界市場は、2024年に58億米ドルに達し、2025年から2034年にかけてCAGR 16.7%で成長すると予測されています。

この成長の原動力となっているのは、産業界全体におけるコネクテッドデバイスの急速な普及と、産業オートメーションおよびスマートテクノロジーの継続的な進歩です。IoT対応デバイスの導入が加速するにつれ、データを効率的に処理・管理できるマイクロコントローラの需要が急増しています。通信とリアルタイムのデータ処理を促進するように設計されたIoTマイクロコントローラは、家電、産業機械、ヘルスケア、スマートホームのエコシステム全体のアプリケーションの電源として重要な役割を果たしています。エネルギー効率が重視されるようになり、AI主導の技術がIoT機器に統合されたことで、高性能マイコンの需要はさらに高まっています。

産業界がデジタルトランスフォーメーションに移行し、インダストリー4.0の実践を受け入れるにつれ、予知保全、遠隔監視、プロセス最適化を強化するためのIoTマイクロコントローラへの依存度が高まることが予想されます。さらに、5Gコネクティビティの出現とエッジコンピューティングの普及が、複雑なデータプロセスをリアルタイムで管理できるより高度なマイコンの必要性を高めています。ウェアラブル、スマートホームデバイス、コネクテッドヘルスケア・ソリューションに対する需要の高まりも市場拡大に寄与しています。世界のスマートシティとコネクテッド・インフラストラクチャ・プロジェクトの進化は、IoTマイクロコントローラ市場の成長軌道をさらに強化しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 58億米ドル |

| 予測金額 | 267億米ドル |

| CAGR | 16.7% |

市場はマイクロコントローラタイプによって区分され、8ビット、16ビット、32ビットがあります。8ビットマイクロコントローラ市場は2024年に19億米ドルを生み出し、そのシンプルさ、費用対効果、低エネルギー消費の恩恵を受けています。これらのマイクロコントローラは、基本的なIoTアプリケーションに最適であり、電力効率が不可欠なバッテリー駆動デバイスに特に適しています。スマートホームデバイス、ウェアラブル、IoT対応家電の採用が増加していることから、特にスマート照明、リモコン、オートメーションシステムなどのアプリケーションで、8ビットマイクロコントローラの需要が高まっています。消費者がより手頃な価格でエネルギー効率の高いソリューションを求める中、こうしたマイクロコントローラの需要は引き続き堅調に推移すると予想されます。

IoTマイクロコントローラ市場は用途別にも分類され、主なセグメントは産業オートメーション、スマートホームデバイス、ウェアラブル、医療機器、テレマティクス、精密農業などです。産業オートメーションは、2034年までに60億米ドルを生み出すと予想されており、最大のセグメントとなっています。スマート製造やインダストリー4.0の普及により、自動車、航空宇宙、物流などの分野でIoTマイクロコントローラの利用が進んでいます。これらのマイコンは、予知保全を促進し、リアルタイムのモニタリングを可能にし、産業プロセスを最適化することで、全体的な運用効率を高め、ダウンタイムを削減します。

米国のIoTマイクロコントローラ市場は、スマートホーム技術やヘルスケアシステムの需要増加に牽引され、2034年までに77億米ドルを創出すると予測されています。主要企業は、高度なIoTアプリケーションの高まる要件に対応するため、マイクロコントローラの性能強化に多額の投資を続けています。CHIPS法などの政府のイニシアチブは、米国での半導体製造を強化し、海外サプライチェーンへの依存を減らし、米国IoTマイクロコントローラ市場のイノベーションを促進することを目的としています。このような取り組みにより、米国は世界のIoTマイクロコントローラ市場において重要な役割を果たすことが期待されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- コネクテッド・デバイスの普及

- 無線通信技術の進歩

- スマートホームデバイスの採用増加

- IoTデバイスの急速な普及

- 政府のイニシアティブとスマートシティプロジェクト

- 業界の潜在的リスク&課題

- 急速な技術変化

- サプライチェーンの混乱

- 促進要因

- 潜在成長力の分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 8ビット

- 16ビット

- 32ビット

第6章 市場推計・予測:用途別、2021年~2034年

- 産業オートメーション

- スマートホームデバイス

- ウェアラブル機器

- 医療機器

- テレマティクス

- 精密農業

- その他

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- コンシューマーエレクトロニクス

- 自動車

- ヘルスケア

- 産業

- 住宅

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Ambiq Micro, Inc.

- Analog Devices, Inc.

- ARM Holdings

- Broadcom Inc.

- Espressif Systems

- Holtek Semiconductor Inc

- Infineon Technologies AG

- Intel Corporation

- Marvell Technology Group Ltd.

- Mediatek Inc.

- Microchip Technology Inc.

- Nuvoton Technology Corporation

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- ROHM Semiconductor Co., Ltd.

- Seiko Epson Corporation

- Silicon Laboratories

- STMicroelectronics

- Texas Instruments Incorporated

- Toshiba Electronic Devices &Storage Corporation

The Global IoT Microcontroller Market reached USD 5.8 billion in 2024 and is expected to grow at a CAGR of 16.7% between 2025 and 2034. This growth is fueled by the rapid proliferation of connected devices across industries and the ongoing advancements in industrial automation and smart technologies. As the adoption of IoT-enabled devices accelerates, the demand for microcontrollers that can efficiently process and manage data has surged. IoT microcontrollers, designed to facilitate communication and real-time data processing, play a crucial role in powering applications across consumer electronics, industrial machinery, healthcare, and smart home ecosystems. The growing emphasis on energy efficiency and the integration of AI-driven technologies into IoT devices further boost the demand for high-performance microcontrollers.

As industries transition toward digital transformation and embrace Industry 4.0 practices, the reliance on IoT microcontrollers to enhance predictive maintenance, remote monitoring, and process optimization is expected to escalate. Moreover, the emergence of 5G connectivity and the increasing popularity of edge computing are driving the need for more advanced microcontrollers capable of managing complex data processes in real time. The rising demand for wearables, smart home devices, and connected healthcare solutions is also contributing to market expansion. The evolution of smart cities and connected infrastructure projects worldwide further strengthens the growth trajectory of the IoT microcontroller market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $26.7 Billion |

| CAGR | 16.7% |

The market is segmented by the type of microcontroller, with 8-bit, 16-bit, and 32-bit variants. The 8-bit microcontroller market generated USD 1.9 billion in 2024, benefiting from its simplicity, cost-effectiveness, and low energy consumption. These microcontrollers are ideal for basic IoT applications, making them particularly well-suited for battery-operated devices where power efficiency is essential. The increasing adoption of smart home devices, wearables, and IoT-enabled consumer electronics is driving the demand for 8-bit microcontrollers, especially in applications such as smart lighting, remote controls, and automation systems. As consumers seek more affordable and energy-efficient solutions, the demand for these microcontrollers is expected to remain strong.

The IoT microcontroller market is also categorized by application, with major segments including industrial automation, smart home devices, wearables, medical devices, telematics, and precision farming. Industrial automation is expected to generate USD 6 billion by 2034, making it the largest segment. The widespread adoption of smart manufacturing and Industry 4.0 practices has propelled the use of IoT microcontrollers in sectors such as automotive, aerospace, and logistics. These microcontrollers facilitate predictive maintenance, enable real-time monitoring, and optimize industrial processes, enhancing overall operational efficiency and reducing downtime.

The U.S. IoT microcontroller market is projected to generate USD 7.7 billion by 2034, driven by increasing demand for smart home technologies and healthcare systems. Major companies continue to invest heavily in enhancing microcontroller performance to meet the growing requirements of advanced IoT applications. Government initiatives, such as the CHIPS Act, aim to strengthen local semiconductor manufacturing, reduce reliance on foreign supply chains, and foster innovation in the U.S. IoT microcontroller market. These efforts are expected to position the United States as a key player in the global IoT microcontroller landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 The proliferation of connected devices

- 3.2.1.2 Advancements in wireless communication technologies

- 3.2.1.3 Increased adoption of smart home devices

- 3.2.1.4 Rapid adoption of IoT devices

- 3.2.1.5 Government initiatives and smart city projects

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid technological changes

- 3.2.2.2 Supply chain disruptions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Product, 2021 – 2034 (USD Million)

- 5.1 8 Bit

- 5.2 16 Bit

- 5.3 32 Bit

Chapter 6 Market estimates & forecast, By Application, 2021 – 2034 (USD Million)

- 6.1 Industrial automation

- 6.2 Smart home devices

- 6.3 Wearable devices

- 6.4 Medical devices

- 6.5 Telematics

- 6.6 Precision farming

- 6.7 Others

Chapter 7 Market estimates & forecast, By End Use Industry, 2021 – 2034 (USD Million)

- 7.1 Consumer electronics

- 7.2 Automotive

- 7.3 Healthcare

- 7.4 Industrial

- 7.5 Residential

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ambiq Micro, Inc.

- 9.2 Analog Devices, Inc.

- 9.3 ARM Holdings

- 9.4 Broadcom Inc.

- 9.5 Espressif Systems

- 9.6 Holtek Semiconductor Inc

- 9.7 Infineon Technologies AG

- 9.8 Intel Corporation

- 9.9 Marvell Technology Group Ltd.

- 9.10 Mediatek Inc.

- 9.11 Microchip Technology Inc.

- 9.12 Nuvoton Technology Corporation

- 9.13 NXP Semiconductors N.V.

- 9.14 Renesas Electronics Corporation

- 9.15 ROHM Semiconductor Co., Ltd.

- 9.16 Seiko Epson Corporation

- 9.17 Silicon Laboratories

- 9.18 STMicroelectronics

- 9.19 Texas Instruments Incorporated

- 9.20 Toshiba Electronic Devices & Storage Corporation