|

市場調査レポート

商品コード

1716570

ユーティリティスケール空気絶縁変圧器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Utility Scale Air Insulated Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ユーティリティスケール空気絶縁変圧器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

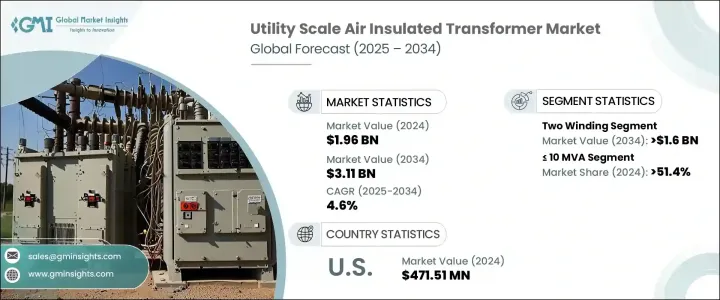

世界のユーティリティスケール空気絶縁変圧器市場の2024年の市場規模は19億6,000万米ドルで、2025年から2034年までのCAGRは4.6%と堅調な成長が見込まれています。

この成長の原動力となっているのは、急速な都市化、産業の成長、特に新興市場における経済の拡大により、世界中で電力需要が高まっていることです。エネルギー需要の増加は、各国に送配電網の近代化を促し、大規模な空気絶縁開閉装置(AIS)変圧器の採用をさらに加速させています。経済が拡大を続け、信頼性の高い送電に対する需要が急増する中、効率的で中断のない電力供給を確保するために、公益事業規模のAIS変圧器が極めて重要になってきています。特に、増大するエネルギー需要に対応するため、電気インフラの拡大・強化に注力している地域が、こうした変圧器技術の採用を促進しています。

AIS変圧器の需要が拡大する中、2巻変圧器セグメントが市場を独占し、2034年までに16億米ドルの収益が見込まれます。これらの変圧器は、特に長距離の電圧を昇圧または降圧する必要がある送電システムに不可欠です。コアと巻線技術、冷却機構、絶縁材料の強化を含むAIS変圧器設計の技術的進歩は、効率、性能、寿命の向上につながりました。こうしたアップグレードにより、現代の高需要電力網における信頼性がさらに高まっています。さらに、より高度な電力管理へのニーズの高まりと、持続可能なエネルギー・ソリューションへのシフトに伴い、この分野は進化を続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 19億6,000万米ドル |

| 予測金額 | 31億1,000万米ドル |

| CAGR | 4.6% |

同市場は、10 MVA以下、10 MVA~100 MVA、100 MVA~600 MVA、600 MVA超といった定格ごとに区分されます。このうち、10 MVA以下セグメントが最大の市場シェアを占め、2024年には市場の51.4%を占めると予測されています。石炭、天然ガス、水力、原子力を使用する大規模発電所は、効率的な電力処理と長距離送電のためにこれらの変圧器に大きく依存しているため、このセグメントは着実に成長すると見られています。

米国では、ユーティリティスケール空気絶縁変圧器市場は2024年に4億7,151万米ドルを創出しました。クリーンパワープランやグリーンニューディールといった連邦および州の政策により、米国は脱炭素化への取り組みを優先するようになりました。再生可能エネルギー導入の推進には、変電所や送電網を含む国内の送電インフラの大幅なアップグレードが必要です。再生可能エネルギーに伴う高い電力負荷を効率的に処理するため、AIS変圧器の需要は急増しています。米国が再生可能エネルギー容量を拡大し続ける中、耐久性、効率性、信頼性の高い電力インフラに対するニーズは高まる一方です。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:巻線別、2021年~2034年

- 主要動向

- 2巻線

- オートトランス

第6章 市場規模・予測:定格別、2021年~2034年

- 主要動向

- 10 MVA以下

- 10 MVA~100 MVA未満

- 100 MVA~600 MVA未満

- 600 MVA

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- ARTECHE

- Celme

- CG Power &Industrial Solutions

- DAIHEN Corporation

- Eaton

- Elsewedy Electric

- General Electric

- Hyosung Heavy Industries

- IMEFY GROUP

- Kirloskar Electric Company

- Mitsubishi Electric Corporation

- Ormazabal

- Pfiffner Group

- Schneider Electric

- Siemens Energy

- Toshiba International Corporation

- Trench Group

The Global Utility Scale Air Insulated Transformer Market was valued at USD 1.96 billion in 2024 and is expected to grow at a robust CAGR of 4.6% from 2025 to 2034. This growth is driven by the rising demand for electricity across the globe, spurred by rapid urbanization, industrial growth, and the expansion of economies, especially in emerging markets. The increasing need for energy is prompting nations to modernize their power transmission and distribution networks, further accelerating the adoption of Air Insulated Switchgear (AIS) transformers on a large scale. As economies continue to expand and the demand for reliable electricity transmission surges, utility-scale AIS transformers are becoming crucial to ensure efficient and uninterrupted power supply. In particular, regions focusing on expanding and enhancing their electrical infrastructure to meet growing energy needs are driving the adoption of these transformer technologies.

With the demand for AIS transformers growing, the two-winding transformer segment is expected to dominate the market, with an estimated revenue generation of USD 1.6 billion by 2034. These transformers are essential for transmission systems, particularly when it is required to either step up or step down voltage over long distances. The technological advancements in AIS transformer design, including enhancements in core and winding technology, cooling mechanisms, and insulation materials, have led to improved efficiency, performance, and longevity. These upgrades make them even more reliable in modern, high-demand power grids. Furthermore, this segment continues to evolve with the growing need for more sophisticated power management and the shift toward sustainable energy solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.96 Billion |

| Forecast Value | $3.11 Billion |

| CAGR | 4.6% |

The market is segmented into different ratings, including <= 10 MVA, > 10 MVA to <= 100 MVA, > 100 MVA to <= 600 MVA, and > 600 MVA. Among these, the <= 10 MVA segment is predicted to hold the largest market share, with 51.4% of the market in 2024. This segment is set to grow steadily, as large-scale power plants that use coal, natural gas, hydro, and nuclear energy rely heavily on these transformers for efficient power handling and transmission over long distances.

In the U.S., the Utility Scale Air Insulated Transformer Market generated USD 471.51 million in 2024. Federal and state policies such as the Clean Power Plan and the Green New Deal have positioned the country to prioritize decarbonization efforts. The push toward renewable energy adoption requires significant upgrades to the nation's power transmission infrastructure, including substations and transmission networks. To efficiently handle the higher power loads associated with renewable energy sources, the demand for AIS transformers has escalated. As the U.S. continues to expand its renewable energy capacity, the need for durable, efficient, and reliable power infrastructure will only intensify.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Winding, 2021 - 2034, (USD Million, '000 Units)

- 5.1 Key trends

- 5.2 Two winding

- 5.3 Auto transformer

Chapter 6 Market Size and Forecast, By Rating, 2021 - 2034, (USD Million, '000 Units)

- 6.1 Key trends

- 6.2 ≤ 10 MVA

- 6.3 > 10 MVA to ≤ 100 MVA

- 6.4 > 100 MVA to ≤ 600 MVA

- 6.5 > 600 MVA

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, (USD Million, '000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Russia

- 7.3.4 UK

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 ARTECHE

- 8.3 Celme

- 8.4 CG Power & Industrial Solutions

- 8.5 DAIHEN Corporation

- 8.6 Eaton

- 8.7 Elsewedy Electric

- 8.8 General Electric

- 8.9 Hyosung Heavy Industries

- 8.10 IMEFY GROUP

- 8.11 Kirloskar Electric Company

- 8.12 Mitsubishi Electric Corporation

- 8.13 Ormazabal

- 8.14 Pfiffner Group

- 8.15 Schneider Electric

- 8.16 Siemens Energy

- 8.17 Toshiba International Corporation

- 8.18 Trench Group