|

市場調査レポート

商品コード

1716521

石油コークス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Petcoke Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 石油コークス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

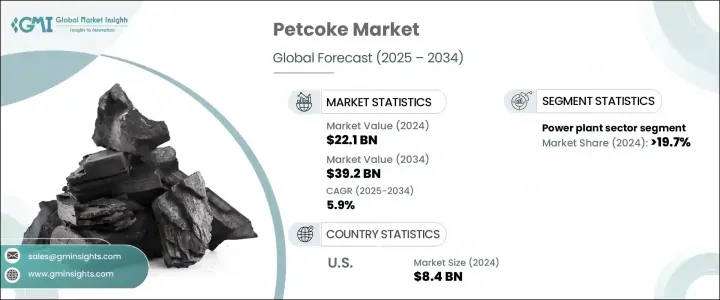

世界の石油コークス市場は2024年に221億米ドルと評価され、2025年から2034年にかけてCAGR 5.9%で拡大すると予測されています。

石油精製に由来する炭素リッチな固体であるペットコークスは、発電、セメント製造、鉄鋼生産などの産業にとって依然として重要な燃料源です。その高い発熱量と費用対効果により、従来の燃料よりも好ましい選択肢となっています。しかし、環境問題への懸念と規制圧力の高まりが、産業界に代替エネルギー源の探求を促しています。世界各国の政府は、石炭が環境に与える悪影響、特に炭素と硫黄の排出量が多いことから、石炭の使用を抑制する厳しい政策を実施しています。この変化は、石油コークスの使用を継続するために、よりクリーンな代替燃料を採用するか、高度な排出制御技術を導入するよう企業を後押ししています。

石油精製設備の増強は、石油コークスの利用可能量を増加させる重要な要因です。より多くの原油が精製されるにつれて、重質油を処理する際の製品別として、より大量の石油コークスが生産されます。さらに、セメントおよび鉄鋼業界からの安定した需要が、市場の成長をさらに後押ししています。これらの産業は、手ごろな価格と高いエネルギー生産量から石油コークスに依存しており、この材料の安定した需要を保証しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 221億米ドル |

| 予測金額 | 392億米ドル |

| CAGR | 5.9% |

石油コークス市場は、燃料用と焼成用に区分されます。燃料グレードの石油コークスは、セメント工場、発電所、鉄鋼生産施設で広く使用されているため、圧倒的なシェアを占めています。高い硫黄分と金属含有量に関する懸念にもかかわらず、石炭に代わるコスト効率の高い代替物であることに変わりはないです。

用途別の市場セグメンテーションには、発電所、セメント、鉄鋼、アルミニウム産業などが含まれます。2024年には、発電所セクターが石油コークス市場全体の19.7%以上を占め、エネルギー生産における重要な役割を浮き彫りにしています。火力発電所は、特に、よりクリーンな燃料が入手しにくい地域では、石油コークスに依存し続けています。

米国の石油コークス市場は顕著な成長を遂げており、評価額は2022年に80億米ドル、2023年に82億米ドル、2024年に84億米ドルに達します。拡大する鉄鋼および電力産業がこの需要を牽引し、ペットコークスの経済的利点、高いエネルギー収率、高炉の炭素源としての役割を活用しています。2024年の米国の消費量は5,440万トンに達し、主にこれらの産業用途に使用されます。天然ガスや石炭と比較した石油コークスのコスト効率は、依然としてその持続的な需要を支える重要な要因です。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションとテクノロジーの展望

第5章 市場規模・予測:グレード別、2021年~2034年

- 主要動向

- 燃料グレード

- 焼成石油コークス

第6章 市場規模・予測:物理的形状別、2021年~2034年

- 主要動向

- スポンジコークス

- パージコークス

- ショットコークス

- ニードルコークス

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 発電所

- セメント産業

- 鉄鋼業界

- アルミニウム産業

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ギリシャ

- ロシア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- トルコ

- クウェート

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- メキシコ

第9章 企業プロファイル

- BP

- Chevron Corporation

- Exxon Mobil

- HF Sinclair Corporation

- Husky Energy

- Marathon Petroleum Corporation

- Oxbow Corporation

- Phillips 66 Company

- Reliance Industries

- Saudi Aramco

- Shell plc

- Valero Energy Corp

- Indian Oil Corporation

- Rosneft

- TotalEnergies

The Global Petcoke Market was valued at USD 22.1 billion in 2024 and is projected to expand at a CAGR of 5.9% from 2025 to 2034. Petcoke, a carbon-rich solid derived from oil refining, remains a key fuel source for industries such as power generation, cement manufacturing, and steel production. Its high calorific value and cost-effectiveness make it a preferred choice over conventional fuels. However, rising environmental concerns and regulatory pressures are prompting industries to explore alternative energy sources. Governments worldwide are implementing stringent policies to curb coal usage due to its adverse environmental impact, particularly high carbon and sulfur emissions. This shift is pushing companies to either adopt cleaner alternatives or implement advanced emission control technologies to continue using petcoke.

The increasing expansion of refinery capacities is a crucial factor contributing to the growing availability of petcoke. As more crude oil is refined, higher volumes of petcoke are produced as a byproduct of processing heavy oil. Additionally, the steady demand from cement and steel industries further propels market growth. These industries rely on petcoke for its affordability and high energy output, ensuring a consistent demand for the material.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.1 Billion |

| Forecast Value | $39.2 Billion |

| CAGR | 5.9% |

The petcoke market is segmented into fuel-grade and calcined petcoke. Fuel-grade petcoke holds a dominant share due to its widespread use in cement plants, power stations, and steel production facilities. It remains a cost-effective alternative to coal despite concerns regarding its high sulfur and metal content.

Market segmentation by application includes power plants, cement, steel, and aluminum industries, among others. In 2024, the power plant sector accounted for over 19.7% of the total petcoke market share, highlighting its critical role in energy production. Thermal power plants continue to rely on petcoke, especially in regions where cleaner fuels are not readily accessible.

The U.S. petcoke market has experienced notable growth, with valuations of USD 8 billion in 2022, USD 8.2 billion in 2023, and USD 8.4 billion in 2024. The expanding steel and power industries drive this demand, capitalizing on petcoke's economic advantages, high energy yield, and role as a carbon source in blast furnaces. In 2024, U.S. consumption reached 54.4 million metric tonnes, primarily for these industrial applications. The cost-efficiency of petcoke compared to natural gas and coal remains a key factor supporting its sustained demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Grade, 2021 - 2034 (MT, USD Million)

- 5.1 Key trends

- 5.2 Fuel grade

- 5.3 Calcined petcoke

Chapter 6 Market Size and Forecast, By Physical Form, 2021 - 2034 (MT, USD Million)

- 6.1 Key trends

- 6.2 Sponge coke

- 6.3 Purge coke

- 6.4 Shot coke

- 6.5 Needle coke

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (MT, USD Million)

- 7.1 Key trends

- 7.2 Power plants

- 7.3 Cement industry

- 7.4 Steel industry

- 7.5 Aluminum industry

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (MT, USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Greece

- 8.3.5 Russia

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 Turkey

- 8.5.3 Kuwait

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Mexico

Chapter 9 Company Profiles

- 9.1 BP

- 9.2 Chevron Corporation

- 9.3 Exxon Mobil

- 9.4 HF Sinclair Corporation

- 9.5 Husky Energy

- 9.6 Marathon Petroleum Corporation

- 9.7 Oxbow Corporation

- 9.8 Phillips 66 Company

- 9.9 Reliance Industries

- 9.10 Saudi Aramco

- 9.11 Shell plc

- 9.12 Valero Energy Corp

- 9.13 Indian Oil Corporation

- 9.14 Rosneft

- 9.15 TotalEnergies