|

市場調査レポート

商品コード

1716449

コンパニオンアニマル用医薬品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Companion Animal Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コンパニオンアニマル用医薬品市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月20日

発行: Global Market Insights Inc.

ページ情報: 英文 134 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

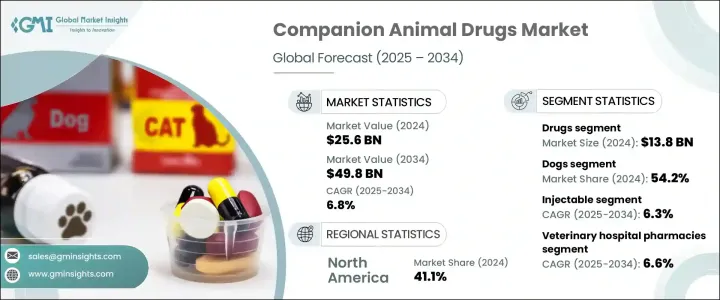

コンパニオンアニマル用医薬品の世界市場は、2024年に256億米ドルと評価され、2025年から2034年にかけてCAGR 6.8%で成長すると予測されています。

コンパニオンアニマルの採用が増加していること、ペットの慢性疾患の有病率が上昇していること、高度な治療や獣医学的ケアに投資するペットオーナーの意欲が高まっていることが、この成長を後押ししています。ペットの飼い主は動物を家族の一員と認識するようになっており、そのため動物の健康を確保するために予防医療、予防接種、投薬に出費するようになっています。こうした意識の変化が市場の拡大に大きく寄与しています。獣医学の進歩に伴い、革新的な製剤、標的療法、ドラッグデリバリー方法の改善により、治療効果と飼い主のコンプライアンスが向上し、市場の成長が加速しています。

2024年に138億米ドルと最も高い市場シェアを占めた医薬品分野は、ペットの慢性疾患や感染症の罹患率の上昇により、引き続き市場を独占しています。ペット飼育の増加とペットの人間化の動向は、抗生物質、抗炎症剤、寄生虫駆除剤の需要を押し上げています。製薬会社は研究開発に積極的に投資し、チュアブル錠や風味をつけた薬など、新しい製剤を導入することで、投与を容易にし、コンプライアンスを向上させています。規制当局の承認や動物用医薬品の技術革新も、この分野の持続的成長を促進する上で極めて重要な役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 256億米ドル |

| 予測金額 | 498億米ドル |

| CAGR | 6.8% |

動物タイプ別では、犬セグメントが2024年に54.2%の最大収益シェアを維持し、高い養子率や犬のケアへの支出増加が牽引しています。がんや糖尿病など、犬の慢性疾患に対する意識の高まりが、高度な治療や薬への需要の高まりにつながっています。これらの疾患の有病率の上昇は、効果的な治療法の必要性を浮き彫りにし、製薬会社が犬の健康をターゲットとした特殊な医薬品を開発することを促しています。包括的なヘルスケア・オプションが利用可能であることや、飼い主の支出が増加していることが、このセグメントの成長をさらに後押ししています。

2024年に最大の市場シェアを占めた注射剤投与経路は、予測期間中にCAGR 6.3%で大きな成長を遂げると予測されています。ワクチン、抗生物質、鎮痛薬などの注射薬は、作用発現が早く、投与量も正確であるため、緊急治療に最適です。注射薬デリバリー技術の進歩や針のない注射器の導入により、ペットと飼い主の双方にとって利便性が向上し、ストレスが軽減されたことが、このルートへの嗜好の高まりに寄与しています。

動物病院薬局は2024年に流通チャネルの大半を占め、2025年から2034年にかけてCAGR 6.6%で成長すると予測されています。これらの薬局は、処方薬、ワクチン、サプリメントを含む幅広い動物ヘルスケア製品を提供しており、ペットの飼い主にとって信頼できる情報源となっています。確立された評判、品質保証、調剤の専門知識は、市場での継続的な優位性の原動力となっています。

北米は2024年に41.1%の最大市場シェアを占め、米国は91億米ドルの収益を上げました。同地域は、発達した獣医医療制度、高いペット飼育率、ペットヘルスケアへの支出増加の恩恵を受けており、コンパニオンアニマル医薬品市場の継続的成長を支えています。主要企業の存在はさらに、革新的で効果的な医薬品の安定供給を保証し、この地域の市場拡大を促進しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界のペット保険需要の急増

- コンパニオンアニマルの肥満率の上昇

- 世界中でペットケアに対する政府支援の増加

- オンライン動物薬局の需要の高まり

- 業界の潜在的リスク&課題

- コンパニオンアニマル用医薬品に関連する高コスト

- 促進要因

- 成長の可能性分析

- 規制状況

- 北米

- 欧州

- アジア太平洋

- GAP分析

- 消費者行動動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 医薬品

- 抗寄生虫薬

- 抗炎症薬

- 抗感染症薬

- 副腎皮質ステロイド

- 精神安定剤

- 心臓血管薬

- 胃腸薬

- ワクチン

- 改良型生ワクチン(MLV)

- キルド不活化ワクチン

- 組み換えワクチン

- 薬用飼料添加物

- 抗生物質

- ビタミン

- アミノ酸

- 酵素

- 酸化防止剤

- プレバイオティクスとプロバイオティクス

- ミネラル

- 炭水化物

- プロパンジオール

第6章 市場推計・予測:動物タイプ別、2021年~2034年

- 主要動向

- 犬

- 猫

- 馬

- その他の動物タイプ

第7章 市場推計・予測:投与経路別、2021~2034年

- 主要動向

- 経口剤

- 注射剤

- 局所

- その他の投与経路

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 動物病院薬局

- eコマース

- 小売薬局

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ポーランド

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- 台湾

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- GCC諸国

- イスラエル

第10章 企業プロファイル

- Agrolabo

- Boehringer Ingelheim International

- Ceva Sante Animale

- Chanelle Pharma

- Dechra Pharmaceuticals

- Elanco Animal Health Incorporated

- Endovac Animal Health

- HIPRA

- Indian Immunologicals

- Merck.

- Norbrook

- Symrise

- Vetoquinol

- Virbac

- Zoetis

The Global Companion Animal Drugs Market was valued at USD 25.6 billion in 2024 and is expected to grow at a CAGR of 6.8% from 2025 to 2034. The increasing adoption of companion animals, the rising prevalence of chronic diseases in pets, and the growing willingness of pet owners to invest in advanced treatments and veterinary care are fueling this growth. Pet owners increasingly perceive their animals as family members, prompting them to spend on preventive care, vaccinations, and medications to ensure their well-being. This shift in attitude has contributed significantly to the expansion of the market. As veterinary science continues to advance, innovative formulations, targeted therapies, and improved drug delivery methods are enhancing treatment efficacy and compliance among pet owners, thereby accelerating market growth.

The drugs segment, which accounted for the highest market share of USD 13.8 billion in 2024, continues to dominate the market due to the rising incidence of chronic diseases and infections in pets. Increased pet ownership and the growing trend of pet humanization have boosted the demand for antibiotics, anti-inflammatory drugs, and parasiticides. Pharmaceutical companies are actively investing in research and development to introduce novel formulations such as chewable tablets and flavored medications, making administration easier and improving compliance. Regulatory approvals and innovations in veterinary medicine have also played a pivotal role in driving the sustained growth of this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.6 Billion |

| Forecast Value | $49.8 Billion |

| CAGR | 6.8% |

By animal type, the dogs segment maintained the largest revenue share of 54.2% in 2024, driven by high adoption rates and increased spending on dog care. Growing awareness of chronic diseases among dogs, such as cancer and diabetes, has led to a higher demand for advanced treatments and medications. The rising prevalence of these conditions highlights the need for effective therapies, encouraging pharmaceutical companies to develop specialized drugs targeting canine health. The availability of comprehensive healthcare options and increased expenditure by pet owners further bolster segment growth.

The injectable route of administration, which held the largest market share in 2024, is anticipated to witness significant growth at a CAGR of 6.3% during the forecast period. Injectable drugs, including vaccines, antibiotics, and analgesics, offer rapid onset of action and precise dosing, making them ideal for emergency treatments. Advancements in injectable drug delivery technologies and the introduction of needle-free injectors have enhanced convenience and reduced stress for both pets and their owners, contributing to the growing preference for this route.

Veterinary hospital pharmacies dominated the distribution channel in 2024 and are projected to grow at a CAGR of 6.6% from 2025 to 2034. These pharmacies offer a wide range of animal healthcare products, including prescription drugs, vaccines, and supplements, making them a reliable source for pet owners. Their established reputation, quality assurance, and expertise in dispensing medications drive their continued dominance in the market.

North America accounted for the largest market share of 41.1% in 2024, with the U.S. generating USD 9.1 billion in revenue. The region benefits from a well-developed veterinary healthcare system, high pet ownership rates, and increased spending on pet healthcare, supporting the continuous growth of the companion animal drugs market. The presence of leading pharmaceutical companies further ensures a steady supply of innovative and effective drugs, driving the expansion of the market in this region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for pet insurance policies worldwide

- 3.2.1.2 Rising rate of obesity in companion animals

- 3.2.1.3 Increasing government support for pet care across the globe

- 3.2.1.4 Growing demand for online veterinary pharmacies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with companion animal drugs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 GAP analysis

- 3.6 Consumer behaviour trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Drugs

- 5.2.1 Antiparasitic

- 5.2.2 Anti-inflammatory

- 5.2.3 Anti-infectives

- 5.2.4 Corticosteroids

- 5.2.5 Tranquilizers

- 5.2.6 Cardiovascular drugs

- 5.2.7 Gastrointestinal drugs

- 5.3 Vaccines

- 5.3.1 Modified live vaccines (MLV)

- 5.3.2 Killed inactivated vaccines

- 5.3.3 Recombinant vaccines

- 5.4 Medicated feed additives

- 5.4.1 Antibiotics

- 5.4.2 Vitamins

- 5.4.3 Amino acids

- 5.4.4 Enzymes

- 5.4.5 Antioxidants

- 5.4.6 Prebiotics and probiotics

- 5.4.7 Minerals

- 5.4.8 Carbohydrates

- 5.4.9 Propandiol

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Horses

- 6.5 Other animal types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Topical

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacies

- 8.3 E-commerce

- 8.4 Retail pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Taiwan

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 GCC Countries

- 9.6.3 Israel

Chapter 10 Company Profiles

- 10.1 Agrolabo

- 10.2 Boehringer Ingelheim International

- 10.3 Ceva Sante Animale

- 10.4 Chanelle Pharma

- 10.5 Dechra Pharmaceuticals

- 10.6 Elanco Animal Health Incorporated

- 10.7 Endovac Animal Health

- 10.8 HIPRA

- 10.9 Indian Immunologicals

- 10.10 Merck.

- 10.11 Norbrook

- 10.12 Symrise

- 10.13 Vetoquinol

- 10.14 Virbac

- 10.15 Zoetis