小児向けイメージング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Pediatric Imaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708243

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

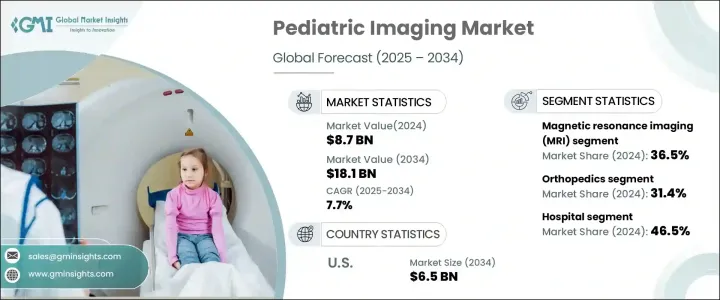

世界の小児向けイメージング市場は、2024年に87億米ドルと評価され、2025年から2034年にかけてCAGR 7.7%で成長すると予測されています。

小児向けイメージング診断は、乳幼児期から思春期までの小児の病状の診断と評価に重要な役割を果たしています。医療画像技術の進歩は小児放射線医学に革命をもたらし、放射線被曝に伴うリスクを最小限に抑えながら、安全性、正確性、効率性を向上させています。低放射線画像、AI主導の診断、3D画像技術などの最先端のイノベーションは、患者の転帰を大幅に改善し、このダイナミックな分野の成長を促進しています。小児疾患の有病率の増加、ヘルスケア専門家の意識の高まり、画像診断モダリティの継続的な開発が市場拡大をさらに後押ししています。さらに、小児向けイメージング診断における人工知能の統合は、診断プロセスを合理化し、より迅速で正確な解釈を可能にすることで、臨床的意思決定を向上させています。また、非侵襲的な診断手順が重視されるようになり、世界的に小児専門病院が増加していることも、高度な画像ソリューションの需要を後押ししています。

市場は、超音波、磁気共鳴画像(MRI)、コンピュータ断層撮影(CT)、X線などの画像モダリティ別に区分されます。MRIは2024年に36.5%の市場シェアを占め、若い患者を電離放射線に曝すことなく高解像度の画像を提供できることから、好まれる画像診断モダリティとしての地位を確立しました。MRIは神経、筋骨格系、軟部組織の診断に有効であるため、小児ヘルスケアに不可欠です。ノイズ低減機能、高速スキャン機能、小児に優しい設計などの最近の進歩により、MRI検査は小児患者にとってより身近でストレスの少ないものとなり、ヘルスケア施設での導入が増加しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 87億米ドル |

| 予測金額 | 181億米ドル |

| CAGR | 7.7% |

小児向けイメージングは用途別にも分類され、神経学、整形外科、心臓病学、腫瘍学、消化器病学などが主要分野です。整形外科分野は2024年に31.4%と最大のシェアを占め、小児の筋骨格系障害や傷害の罹患率の上昇がその要因となっています。非侵襲的な診断ソリューションに対する需要は高まっており、3Dイメージング、コーンビームCT、デジタルX線撮影などの技術革新は、整形外科診断の精度と効率を高める上で極めて重要な役割を果たしています。これらの技術進歩は、小児整形外科疾患の診断・治療方法を変革し、市場の成長をさらに後押ししています。

米国の小児向けイメージング市場は、2024年に30億米ドルと評価され、2025年から2034年にかけてCAGR 7.6%で成長すると予測されています。先天性心疾患や神経疾患など、小児の健康状態の蔓延が進んでいることが、高度なイメージング技術への需要を煽っています。ポータブル超音波診断装置と低放射線CTスキャンは、患者の安全性と快適性を確保しながら高品質の画像診断を提供できることから、人気を集めています。早期診断の継続的な重視と小児ヘルスケアインフラの拡充は、米国における小児向けイメージング診断サービスの力強い成長に寄与する主な要因です。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 小児疾患の増加

- 画像技術の進歩

- 認知度とアクセシビリティの向上

- 政府の支援イニシアティブ

- 業界の潜在的リスク&課題

- 放射線被曝の懸念

- 高度な画像処理機器の高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:イメージングモダリティ別、2021年~2034年

- 主要動向

- 超音波

- 磁気共鳴画像法(MRI)

- コンピュータ断層撮影(CT)

- X線

- その他の画像モダリティ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 神経

- 整形外科

- 循環器

- 腫瘍学

- 消化器内科

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 画像診断センター

- 小児科クリニック

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Agfa-Gevaert Group

- Analogic

- Canon

- Carestream Health

- Esaote

- FUJIFILM

- GE Healthcare

- Hyperfine

- Koninklijke Philips

- LMT Medical Systems

- Mindray

- Samsung Healthcare

- Shimadzu

- Siemens Healthineers

目次

The Global Pediatric Imaging Market was valued at USD 8.7 billion in 2024 and is projected to grow at a CAGR of 7.7% from 2025 to 2034. Pediatric imaging plays a crucial role in diagnosing and assessing medical conditions in children, from infancy through adolescence. Advances in medical imaging technology have revolutionized pediatric radiology, enhancing safety, accuracy, and efficiency while minimizing risks associated with radiation exposure. Cutting-edge innovations such as low-radiation imaging, AI-driven diagnostics, and 3D imaging techniques are significantly improving patient outcomes, fostering growth in this dynamic sector. The increasing prevalence of pediatric disorders, rising awareness among healthcare professionals, and continuous developments in imaging modalities are further propelling market expansion. Additionally, the integration of artificial intelligence in pediatric imaging is streamlining diagnostic processes, allowing for faster and more precise interpretations, thereby improving clinical decision-making. The growing emphasis on non-invasive diagnostic procedures and the increasing number of pediatric specialty hospitals worldwide are also fueling the demand for advanced imaging solutions.

The market is segmented by imaging modalities, including ultrasound, magnetic resonance imaging (MRI), computed tomography (CT), X-ray, and others. MRI held a 36.5% market share in 2024, establishing itself as a preferred imaging modality due to its ability to provide high-resolution images without exposing young patients to ionizing radiation. Its effectiveness in diagnosing neurological, musculoskeletal, and soft tissue conditions makes it indispensable in pediatric healthcare. Recent advancements, such as noise reduction features, faster scanning capabilities, and child-friendly designs, have made MRI procedures more accessible and less stressful for young patients, leading to increased adoption across healthcare facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.7 Billion |

| Forecast Value | $18.1 Billion |

| CAGR | 7.7% |

Pediatric imaging is also categorized by application, with key areas including neurology, orthopedics, cardiology, oncology, and gastroenterology. The orthopedics segment held the largest share at 31.4% in 2024, driven by the rising incidence of musculoskeletal disorders and injuries in children. The demand for non-invasive diagnostic solutions is escalating, and innovations such as 3D imaging, cone-beam CT, and digital radiography are playing a pivotal role in enhancing the accuracy and efficiency of orthopedic diagnostics. These technological advancements are transforming the way pediatric orthopedic conditions are diagnosed and treated, further bolstering market growth.

The U.S. Pediatric Imaging Market was valued at USD 3 billion in 2024 and is anticipated to grow at a CAGR of 7.6% from 2025 to 2034. The increasing prevalence of pediatric health conditions, including congenital heart defects and neurological disorders, is fueling demand for advanced imaging technologies. Portable ultrasound machines and low-radiation CT scans are gaining traction due to their ability to provide high-quality imaging while ensuring patient safety and comfort. The continued emphasis on early diagnosis and the expansion of pediatric healthcare infrastructure are key factors contributing to the strong growth of pediatric imaging services in the U.S.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of pediatric diseases

- 3.2.1.2 Advancements in imaging technologies

- 3.2.1.3 Growing awareness and accessibility

- 3.2.1.4 Supportive government initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Radiation exposure concerns

- 3.2.2.2 High costs of advanced imaging equipment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Imaging Modality, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Ultrasound

- 5.3 Magnetic resonance imaging (MRI)

- 5.4 Computed tomography (CT)

- 5.5 X-ray

- 5.6 Other imaging modalities

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Neurology

- 6.3 Orthopedics

- 6.4 Cardiology

- 6.5 Oncology

- 6.6 Gastroenterology

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic imaging centers

- 7.4 Pediatric clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Agfa-Gevaert Group

- 9.2 Analogic

- 9.3 Canon

- 9.4 Carestream Health

- 9.5 Esaote

- 9.6 FUJIFILM

- 9.7 GE Healthcare

- 9.8 Hyperfine

- 9.9 Koninklijke Philips

- 9.10 LMT Medical Systems

- 9.11 Mindray

- 9.12 Samsung Healthcare

- 9.13 Shimadzu

- 9.14 Siemens Healthineers

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 132 Pages

- 納期

- 2~3営業日