|

市場調査レポート

商品コード

1708240

経口抗糖尿病薬の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測Oral Antidiabetic Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 経口抗糖尿病薬の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

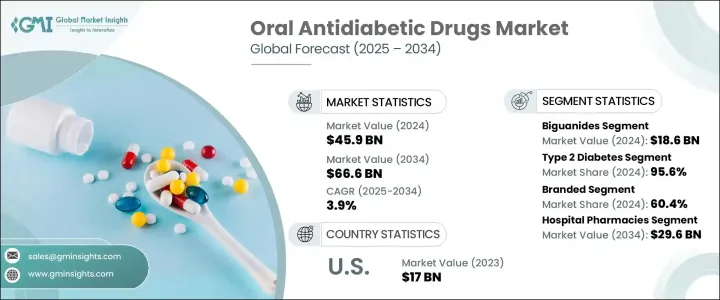

経口抗糖尿病薬の世界市場は、2024年に459億米ドルを生み出し、2025年から2034年にかけてCAGR3.9%で拡大すると予測されています。

この市場の成長は、糖尿病、特に2型糖尿病(T2DM)の世界の有病率の上昇が大きな原動力となっています。特に開発途上国でT2DMと診断される人が増えているのは、座りっぱなしのライフスタイルや食生活の乱れが原因です。インスリン抵抗性の主な原因である肥満は、血糖値を調整するための経口薬の需要をさらに高めています。ナトリウム-グルコース輸送タンパク質-2(SGLT-2)阻害薬やジペプチジルペプチダーゼ-4(DPP-4)阻害薬などの薬剤が人気を集めています。これらの薬剤は、血糖値の効果的なコントロールに加え、体重管理というその他の特典もあり、患者に包括的な解決策を提供します。

この市場は薬剤クラス別に、ビグアナイド薬、SGLT-2阻害薬、DPP-4阻害薬、スルホニル尿素薬、チアゾリジン系薬剤、メグリチニド薬、α-グルコシダーゼ阻害薬、その他のカテゴリーに区分されます。2024年には、ビグアナイド薬セグメントは186億米ドルを売り上げ、最も広く処方されているビグアナイド薬であるメトホルミンは、T2DMの第一選択薬としての優位性を維持しています。メトホルミンは、肝グルコース産生を低下させ、インスリン感受性を高めることによって血糖値を下げる作用があり、市場での地位を確固たるものにしています。さらに、ビグアナイド系薬剤は引き続き医療従事者の第一選択薬であり、市場の安定に大きく寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 459億米ドル |

| 予測金額 | 666億米ドル |

| CAGR | 3.9% |

疾患タイプを考慮すると、2024年には2型糖尿病セグメントが95.6%の圧倒的シェアを占めました。これは、世界中でT2DMの有病率が増加していることに直接関連しています。特に人口の多い国では、都市化、不健康な食習慣、運動不足がT2DMの早期発症の主な要因となっています。その結果、簡便で長期間の経口治療薬に対する需要が高まり、糖尿病管理における経口抗糖尿病薬の役割が高まっています。

北米では、経口抗糖尿病薬市場は2024年に41.1%のシェアを占めました。同地域の糖尿病有病率の高さは、薬剤製剤の進歩や患者の意識向上と相まって、今後も市場成長を牽引すると予想されます。高齢化、座りがちなライフスタイル、食生活の乱れといった要因が、同地域における糖尿病罹患率の上昇に寄与しています。さらに、遠隔医療やデジタルヘルスツールなどのヘルスケアにおける技術革新が、患者の病状管理を容易にし、経口抗糖尿病薬の採用をさらに後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 産業エコシステム分析

- 業界への影響要因

- 成長促進要因

- 2型糖尿病の有病率の上昇

- 経口薬への選好の高まり

- オンライン薬局とeコマースの拡大

- 併用療法の動向の高まり

- 業界の潜在的リスク・課題

- 新薬クラスの高コスト

- 副作用と安全性への懸念

- 成長促進要因

- 成長可能性分析

- 規制状況

- パイプライン分析

- 糖尿病の状況

- 世界の糖尿病患者数(地域別)、2024年

- 糖尿病患者数の多い国、2024年

- 世界の糖尿病死亡者数、地域別、2024年

- 世界の糖尿病患者数が最も多くなると予測される国、2045年

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場マトリックス分析

- 主要市場企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- ビグアナイド薬

- ジペプチジルペプチダーゼ4(DPP-4)阻害薬

- シタグリプチン

- リナグリプチン

- ビルダグリプチン

- サキサグリプチン

- アログリプチン

- その他のDPP-4阻害薬

- ナトリウム-グルコース輸送タンパク質-2(SGLT-2)阻害薬

- ダパグリフロジン

- エンパグリフロジン

- カナグリフロジン

- スルホニル尿素

- グリメピリド

- グリピジド

- グリブリド

- チアゾリジン系薬剤

- メグリチニド

- レパグリニド

- ナテグリニド

- α-グルコシダーゼ阻害薬

- その他の薬剤クラス別

第6章 市場推計・予測:疾患タイプ別、2021年~2034年

- 主要動向

- 2型糖尿病

- 1型糖尿病

第7章 市場推計・予測:治療薬タイプ別、2021年~2034年

- 主要動向

- ブランド薬

- ジェネリック医薬品

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Astellas Pharma

- AstraZeneca

- Bayer

- Boehringer Ingelheim

- Bristol Myers Squibb

- Eli Lilly and Company

- Glenmark Pharmaceuticals

- Johnson &Johnson(Janssen Pharmaceuticals)

- Merck

- Novartis

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceuticals

The Global Oral Antidiabetic Drugs Market generated USD 45.9 billion in 2024 and is projected to expand at a CAGR of 3.9% from 2025 to 2034. The growth of this market is largely driven by the rising global prevalence of diabetes, particularly Type 2 diabetes (T2DM). The increasing number of people diagnosed with T2DM, especially in developing nations, can be traced back to the widespread adoption of sedentary lifestyles and poor dietary habits. Obesity, a major contributor to insulin resistance, has further intensified the demand for oral medications designed to regulate blood sugar levels. Medications such as sodium-glucose transport protein-2 (SGLT-2) inhibitors and dipeptidyl peptidase-4 (DPP-4) inhibitors are becoming more popular. These drugs offer the added benefit of weight management in addition to effectively controlling blood glucose levels, giving patients a comprehensive solution to their condition.

This market is segmented by drug class into biguanides, SGLT-2 inhibitors, DPP-4 inhibitors, sulfonylureas, thiazolidinediones, meglitinides, alpha-glucosidase inhibitors, and other categories. In 2024, the biguanides segment generated USD 18.6 billion, with Metformin, the most widely prescribed biguanide, maintaining its dominance as the first-line treatment for T2DM. Its ability to reduce blood glucose levels by lowering hepatic glucose production and increasing insulin sensitivity has solidified its position in the market. Furthermore, biguanides continue to be a primary choice for healthcare providers, contributing significantly to market stability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $45.9 Billion |

| Forecast Value | $66.6 Billion |

| CAGR | 3.9% |

When considering disease type, the Type 2 diabetes segment accounted for a dominant 95.6% share in 2024. This is directly linked to the increasing prevalence of T2DM worldwide. Urbanization, unhealthy eating habits, and a lack of physical activity are key contributors to the early onset of T2DM, particularly in large-population countries. Consequently, there is a rising demand for convenient, long-term oral treatment options, reinforcing the growing role of oral antidiabetic drugs in managing diabetes.

In North America, the oral antidiabetic drugs market held a 41.1% share in 2024. The region's high prevalence of diabetes, combined with ongoing advancements in drug formulations and increased patient awareness, is expected to continue driving market growth. Factors such as aging populations, sedentary lifestyles, and poor dietary habits are contributing to the rising incidence of diabetes in the region. Additionally, innovations in healthcare, such as telemedicine and digital health tools, have made it easier for patients to manage their condition, further boosting the adoption of oral antidiabetic drugs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of type 2 diabetes

- 3.2.1.2 Increased preference for oral medications

- 3.2.1.3 Expansion of online pharmacies and e-commerce

- 3.2.1.4 Growing trend for combination therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of newer drug classes

- 3.2.2.2 Side effects and safety concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Diabetes landscape

- 3.6.1 Number of diabetics worldwide, by region, 2024

- 3.6.2 Countries with the highest number of diabetics, 2024

- 3.6.3 Number of diabetes deaths worldwide, by region, 2024

- 3.6.4 Countries with the highest projected number of diabetics worldwide in 2045

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Biguanides

- 5.3 Dipeptidyl peptidase - 4 (DPP-4) inhibitors

- 5.3.1 Sitagliptin

- 5.3.2 Linagliptin

- 5.3.3 Vildagliptin

- 5.3.4 Saxagliptin

- 5.3.5 Alogliptin

- 5.3.6 Other DPP-4 inhibitors

- 5.4 Sodium-glucose transport protein-2 (SGLT-2) inhibitors

- 5.4.1 Dapagliflozin

- 5.4.2 Empagliflozin

- 5.4.3 Canagliflozin

- 5.5 Sulfonylureas

- 5.5.1 Glimepiride

- 5.5.2 Glipizide

- 5.5.3 Glyburide

- 5.6 Thiazolidinediones

- 5.7 Meglitinides

- 5.7.1 Repaglinide

- 5.7.2 Nateglinide

- 5.8 Alpha-glucosidase inhibitors

- 5.9 Other drug classes

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Type 2 diabetes

- 6.3 Type 1 diabetes

Chapter 7 Market Estimates and Forecast, By Medication Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Branded

- 7.3 Generic

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Astellas Pharma

- 10.2 AstraZeneca

- 10.3 Bayer

- 10.4 Boehringer Ingelheim

- 10.5 Bristol Myers Squibb

- 10.6 Eli Lilly and Company

- 10.7 Glenmark Pharmaceuticals

- 10.8 Johnson & Johnson (Janssen Pharmaceuticals)

- 10.9 Merck

- 10.10 Novartis

- 10.11 Novo Nordisk

- 10.12 Pfizer

- 10.13 Sanofi

- 10.14 Takeda Pharmaceuticals