|

市場調査レポート

商品コード

1708233

馬用画像サービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Equine Imaging Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 馬用画像サービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月28日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

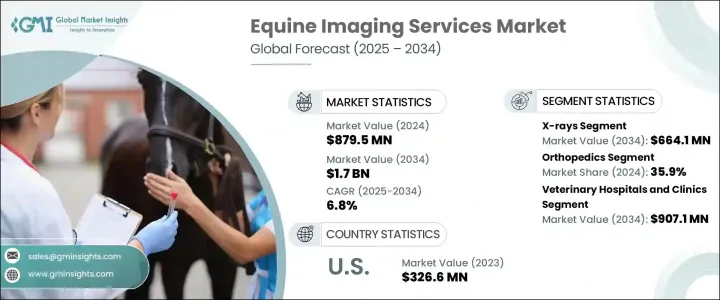

世界の馬用画像サービス市場は、2024年に8億7,950万米ドルと評価され、2025年から2034年にかけてCAGR 6.8%で成長すると予測されています。

この成長は、馬の関節炎、靭帯損傷などの筋骨格系疾患の有病率の上昇が原動力となっています。3Dイメージング、デジタルX線撮影、ポータブル機器などの画像診断技術の進歩が広く受け入れられ、市場拡大に寄与しています。さらに、馬のスポーツやレース分野の急成長により、傷害の予防や治療のための高度な画像ソリューションの必要性が高まっています。革新的な画像技術の開発に焦点を当てた獣医学研究とパートナーシップの増加が市場をさらに牽引しています。また、AIを搭載した診断ツールの受け入れが進んでいることも、馬の画像診断の効率と精度を高めており、獣医療現場にとって価値あるものとなっています。

馬用画像サービスには、診断と治療をサポートするために馬の解剖学的構造を可視化する診断技術が含まれます。これらのサービスでは、X線、超音波、磁気共鳴画像法(MRI)、コンピュータ断層撮影法(CT)、核画像を利用して、筋骨格系の問題、靭帯損傷、内部の異常を検出します。画像モダリティ別に見ると、世界市場はX線、超音波、MRI、核画像システム、CTスキャン、その他のモダリティに区分されます。X線セグメントは、2024年に3億5,520万米ドルの最高収益を上げ、2034年には6億6,410万米ドルに達し、CAGR 6.5%で成長すると予測されています。X線は、骨折、関節疾患、筋骨格系疾患の診断に最も一般的に使用される画像診断法です。手ごろな価格で入手でき、迅速な診断結果が得られるX線検査は、馬の獣医師にとって好ましい選択となっています。ポータブルX線装置は、現場での評価を可能にすることで診断プロセスをさらに簡素化し、馬を専門施設に運ぶ必要性を減らしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億7,950万米ドル |

| 予測金額 | 17億米ドル |

| CAGR | 6.8% |

市場は用途別に、整形外科、腫瘍学、循環器学、神経学、その他の用途に分類されます。整形外科分野は、スポーツ馬、競走馬、農耕馬における筋骨格系の損傷や関節障害の高い有病率を反映して、2024年の市場シェアの35.9%を占めました。馬の整形外科では、靭帯損傷、骨折、腱異常、変形性関節症の診断にX線検査やMRI検査が頻繁に使用されています。診断精度と治療計画のために高度な画像技術の採用が増加していることが、このセグメントの拡大を促進すると予想されます。馬のヘルスケアと診断への投資の増加は、整形外科画像サービスの需要を促進し、市場での地位を強化しています。

最終用途別では、世界市場は動物病院・診療所、動物診断センター、学術・研究機関に区分されます。動物病院と診療所は、6.6%の成長率で支配的な地位を占め、2034年までに9億710万米ドルに達すると予想されています。この優位性は、これらの施設でX線、CTスキャン、MRI、その他のモダリティなどの高度な画像技術が幅広く利用できることに起因しています。これらの病院や診療所は、馬の筋骨格系、神経系、内部障害の診断と治療に特化しているため、画像診断サービスには好適です。さらに、馬ヘルスケアへの支出の増加や馬主人口の増加が、これらの施設が提供する画像診断サービスの需要に拍車をかけています。高度な診断アプリケーションのための動物病院と研究機関との戦略的提携が、市場の成長をさらに促進しています。

2024年には、米国が北米の馬用画像サービス市場のリーダーとして浮上し、評価額は3億4,650万米ドルと、2023年の3億2,660万米ドルから増加しました。このリーダーシップは、米国の高度な獣医学インフラ、高い馬の飼育数、馬ヘルスケアへの多額の投資に起因しています。MRI、CT、デジタルX線撮影などの高度な画像技術を備えた専門クリニックや病院の存在が、国レベルでの成長を促進しています。獣医学研究に対する政府の支援と資金援助は、継続的な技術向上と相まって、米国の市場拡大にさらに貢献しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 馬の疾病の増加

- 画像技術の進歩

- 馬術スポーツ産業の成長

- モバイルイメージングサービスの拡大

- 業界の潜在的リスク&課題

- 高度な画像処理機器の高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:イメージングモダリティ別、2021年~2034年

- 主要動向

- X線

- 超音波検査

- MRIスキャン

- 核医学画像システム

- CTスキャン

- その他の画像モダリティ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 整形外科

- 腫瘍学

- 循環器

- 神経学

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 動物病院&クリニック

- 動物診断センター

- 学術・研究機関

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Chaparral Veterinary Medical Center

- Chine House Veterinary Hospital

- Daniel Equine Services

- Hagyard Equine Medical Institute

- IDEXX Laboratories

- IMV Imaging

- Mid-Atlantic Equine Medical Center

- Moore Equine P.C

- National Research Center on Equines.

- Rainbow Equine Hospital

- Royal Veterinary College's Equine Referral Hospital

- Tennessee Equine Hospital

- VET.CT

- Vets Pets

- Virginia Equine Imaging

The Global Equine Imaging Services Market was valued at USD 879.5 million in 2024 and is projected to grow at a CAGR of 6.8% from 2025 to 2034. This growth is driven by the rising prevalence of musculoskeletal disorders such as arthritis, ligament injuries, and other conditions in horses. Advances in diagnostic imaging technologies, including 3D imaging, digital radiography, and portable machines, have gained widespread acceptance, contributing to market expansion. Moreover, the rapid growth of the equine sports and racing sectors has intensified the need for advanced imaging solutions for injury prevention and treatment. Increased veterinary research and partnerships focused on developing innovative imaging technologies are further driving the market. Higher acceptance of AI-powered diagnostic tools is also enhancing the efficiency and accuracy of equine imaging, making it a valuable addition to veterinary practices.

Equine imaging services involve diagnostic techniques that visualize a horse's anatomy to support diagnosis and treatment. These services utilize X-rays, ultrasound, magnetic resonance imaging (MRI), computed tomography (CT), and nuclear imaging to detect musculoskeletal issues, ligament injuries, and internal abnormalities. By imaging modality, the global market is segmented into X-rays, ultrasound, MRI, nuclear imaging systems, CT scans, and other modalities. The X-rays segment generated the highest revenue of USD 355.2 million in 2024 and is expected to reach USD 664.1 million by 2034, growing at a CAGR of 6.5%. X-rays remain the most commonly used imaging method for diagnosing fractures, joint problems, and musculoskeletal disorders. Their affordability, availability, and ability to deliver rapid diagnostic results make them a preferred choice for equine veterinarians. Portable X-ray machines have further simplified the diagnostic process by allowing on-site evaluations, reducing the need to transport horses to specialized facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $879.5 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 6.8% |

Based on application, the market is categorized into orthopedics, oncology, cardiology, neurology, and other applications. The orthopedics segment accounted for 35.9% of the market share in 2024, reflecting the high prevalence of musculoskeletal injuries and joint disorders in sport, racing, and farm horses. X-rays and MRI scans are frequently used for diagnosing ligament injuries, fractures, tendon abnormalities, and osteoarthritis in equine orthopedics. The growing adoption of advanced imaging technologies for diagnostic accuracy and treatment planning is expected to fuel the expansion of this segment. Increased investments in equine healthcare and diagnostics are driving the demand for orthopedic imaging services, reinforcing their market position.

By end use, the global market is segmented into veterinary hospitals and clinics, veterinary diagnostic centers, and academic and research institutes. Veterinary hospitals and clinics are expected to hold a dominant position with a growth rate of 6.6%, reaching USD 907.1 million by 2034. This dominance is attributed to the extensive availability of advanced imaging technologies such as X-rays, CT scans, MRI, and other modalities in these facilities. These hospitals and clinics specialize in diagnosing and treating equine musculoskeletal, neurological, and internal disorders, making them the preferred choice for imaging services. Additionally, increasing expenditure on equine healthcare and the rising population of horse owners have fueled the demand for imaging services offered by these facilities. Strategic collaborations between veterinary hospitals and research organizations for advanced diagnostic applications are further driving market growth.

In 2024, the US emerged as a leader in the North American equine imaging services market, with a valuation of USD 346.5 million, up from USD 326.6 million in 2023. This leadership is attributed to the country's advanced veterinary infrastructure, high equine population, and significant investments in equine healthcare. The presence of specialized clinics and hospitals equipped with advanced imaging technologies such as MRI, CT, and digital radiography is fostering growth at the country level. Government support and funding for veterinary research, combined with continuous technological enhancements, are further contributing to market expansion in the US.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of equine diseases

- 3.2.1.2 Advancements in imaging technologies

- 3.2.1.3 Growing equine sports industry

- 3.2.1.4 Expansion of mobile imaging services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced imaging equipment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Imaging Modality, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 X-rays

- 5.3 Ultrasound

- 5.4 MRI scans

- 5.5 Nuclear imaging systems

- 5.6 CT scans

- 5.7 Other imaging modalities

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Orthopedics

- 6.3 Oncology

- 6.4 Cardiology

- 6.5 Neurology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Veterinary hospitals & clinics

- 7.3 Veterinary diagnostic centers

- 7.4 Academic & research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Chaparral Veterinary Medical Center

- 9.2 Chine House Veterinary Hospital

- 9.3 Daniel Equine Services

- 9.4 Hagyard Equine Medical Institute

- 9.5 IDEXX Laboratories

- 9.6 IMV Imaging

- 9.7 Mid-Atlantic Equine Medical Center

- 9.8 Moore Equine P.C

- 9.9 National Research Center on Equines.

- 9.10 Rainbow Equine Hospital

- 9.11 Royal Veterinary College's Equine Referral Hospital

- 9.12 Tennessee Equine Hospital

- 9.13 VET.CT

- 9.14 Vets Pets

- 9.15 Virginia Equine Imaging