|

市場調査レポート

商品コード

1708208

上腕骨外側上顆炎治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Lateral Epicondylitis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 上腕骨外側上顆炎治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月21日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

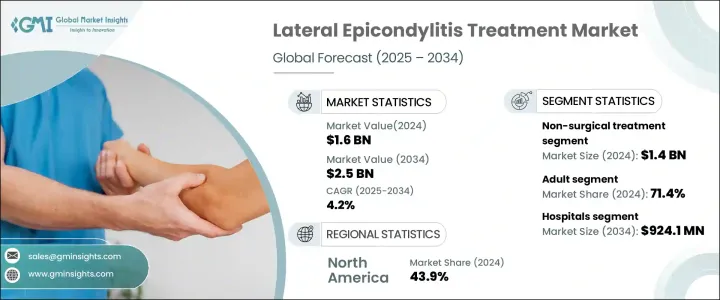

世界の上腕骨外側上顆炎治療市場は、2024年に16億米ドルと評価され、2025年から2034年にかけてCAGR 4.2%で成長すると予測されています。

一般にテニス肘として知られる外側上顆炎の有病率の増加は、主にスポーツやその他の活動への参加の増加によってもたらされています。衝撃の大きいスポーツや反復運動をする人が増えるにつれ、この疾患を発症する可能性は上昇の一途をたどっています。さらに、早期診断と治療オプションに対する意識の高まりが、外科的・非外科的介入に対する需要の高まりにつながっています。また、生物学的療法や低侵襲手術など、より安全で効果的な治療法の革新も著しいです。ヘルスケアプロバイダーが患者中心のアプローチを優先し、予防医療の重要性を強調するにつれて、理学療法やコルチコステロイド注射などの非侵襲的療法の需要が急増し、市場全体の成長に寄与しています。

市場拡大を後押しするもう1つの主要因は、外側上顆炎などの筋骨格系疾患にかかりやすい老年人口の増加です。特に新興経済諸国では高齢化が進んでおり、外科手術に比べて回復が早くリスクが低い非外科的治療を選択する傾向が強まっています。多血小板血漿(PRP)や幹細胞治療などの革新的な治療法は、疼痛管理や組織再生に有望な結果をもたらし、人気を集めています。これらの進歩は、従来の手術に代わる効果的な選択肢を提供するだけでなく、低侵襲な選択肢を好む患者の増加とも合致しており、市場の成長をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億米ドル |

| 予測金額 | 25億米ドル |

| CAGR | 4.2% |

上腕骨外側上顆炎治療市場は、非外科的治療と外科的治療のカテゴリーに大別され、非外科的治療がリードしています。2024年、非外科的治療分野の売上高は14億米ドルでした。理学療法、薬物療法、装具、衝撃波療法などの非外科的療法は、疼痛管理と回復促進において高い有効性を示しています。安全性が高く、ダウンタイムが短く、費用対効果に優れているため、これらの治療を好む患者は増えています。外側上顆炎の治療に保存的アプローチを求める人が増えるにつれ、非外科的療法の需要は増加の一途をたどると予想されます。

年齢層別に市場を分析すると、成人が圧倒的に多く、2024年の市場シェアの71.4%を占めました。成人は、日々の仕事やレクリエーション活動で繰り返される動作により、外側上顆炎を発症しやすいです。スポーツ競合の増加やフィットネス動向は、この疾患の有病率をさらに高め、効果的な治療オプションの必要性を促しています。さらに、疼痛管理ソリューションに対する需要が、外科手術以外の方法の継続的な進歩につながり、患者が安全で信頼できる治療オプションを利用できるようにしています。

米国の上腕骨外側上顆炎治療市場は、2024年に6億5,600万米ドルを創出し、世界情勢における主要プレーヤーとしての地位を確保しました。同国では、スポーツや肉体労働などの身体活動が盛んなため、外側上顆炎の患者数が増加しています。副腎皮質ステロイド注射や局所治療など、効果的な疼痛管理ソリューションの提供に重点を置き、米国市場は繁栄を続けています。生物学的療法と再生医療における継続的な研究開発努力は、世界の上腕骨外側上顆炎治療分野における同国の優位性をさらに強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 外側上顆炎とスポーツ関連傷害の増加

- 低侵襲手術への嗜好の高まり

- 治療方法の進歩

- 業界の潜在的リスク&課題

- 高い治療費

- 代替療法の利用可能性

- 促進要因

- 成長可能性分析

- 規制状況

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:治療タイプ別、2021年~2034年

- 主要動向

- 非外科手術治療

- 薬物療法

- 理学療法

- 装具と装具

- その他の非外科手術治療

- 外科手術治療

- 関節鏡手術

- 開腹手術

- その他の外科手術治療

第6章 市場推計・予測:年齢層別、2021年~2034年

- 主要動向

- 小児

- 成人

- 老年

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 整形外科クリニック

- 在宅医療

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 3M Company

- BTL

- DJO Global(Enovis)

- Folsom Orthopaedics &Sports Medicine

- GlaxoSmithKline

- MedStar Health

- Merck &Co

- Novartis

- Ossur Corporate

- Pfizer

- Pharmascience

- ReLiva Physiotherapy &Rehab

- Scandinavian Physiotherapy Center

- Zimmer Biomet

The Global Lateral Epicondylitis Treatment Market was valued at USD 1.6 billion in 2024 and is projected to grow at a CAGR of 4.2% between 2025 and 2034. The growing prevalence of lateral epicondylitis, commonly known as tennis elbow, is primarily driven by increasing participation in sports and other physical activities. As more individuals engage in high-impact sports and repetitive motion exercises, the likelihood of developing this condition continues to rise. Additionally, heightened awareness about early diagnosis and treatment options has led to a higher demand for both surgical and non-surgical interventions. The market has also witnessed significant innovation in treatment modalities, including biological therapies and minimally invasive procedures, which offer safer and more effective solutions for managing the condition. As healthcare providers prioritize patient-centric approaches and emphasize the importance of preventive care, the demand for non-invasive therapies, such as physical therapy and corticosteroid injections, has surged, contributing to the overall market growth.

Another major factor propelling market expansion is the rising geriatric population, which is more susceptible to musculoskeletal conditions, such as lateral epicondylitis. The aging demographic, particularly in developed economies, is increasingly opting for non-surgical treatments that offer faster recovery times and lower risks compared to surgical procedures. Innovative therapies such as platelet-rich plasma (PRP) and stem cell treatments are gaining traction, offering promising outcomes in pain management and tissue regeneration. These advancements not only provide effective alternatives to traditional surgery but also align with the growing patient preference for minimally invasive options, further driving market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 4.2% |

The lateral epicondylitis treatment market is broadly segmented into non-surgical and surgical treatment categories, with non-surgical options leading the way. In 2024, the non-surgical treatment segment generated USD 1.4 billion in revenue. Non-surgical therapies, including physical therapy, medications, braces, and shockwave therapy, have demonstrated high efficacy in managing pain and accelerating recovery. Patients increasingly prefer these treatments due to their safety, reduced downtime, and cost-effectiveness. As more individuals seek conservative approaches to manage lateral epicondylitis, the demand for non-surgical therapies is expected to continue its upward trajectory.

When analyzing the market by age group, adults dominated the landscape, accounting for 71.4% of the market share in 2024. Adults are more prone to developing lateral epicondylitis due to repetitive movements involved in their daily work or recreational activities. The growing number of sports competitions and fitness trends has further increased the prevalence of this condition, driving the need for effective treatment options. Furthermore, the demand for pain management solutions has led to continuous advancements in non-surgical methods, ensuring that patients have access to safe and reliable treatment options.

The U.S. lateral epicondylitis treatment market generated USD 656 million in 2024, securing its position as a key player in the global landscape. The high incidence of physical activity, including sports and manual labor, has led to an increased number of lateral epicondylitis cases in the country. With a strong emphasis on providing effective pain management solutions, including corticosteroid injections and topical treatments, the U.S. market continues to thrive. Ongoing research and development efforts in biological therapies and regenerative medicine have further strengthened the country's dominance in the global lateral epicondylitis treatment sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of lateral epicondylitis and sports-related injuries

- 3.2.1.2 Growing preference for minimally invasive procedures

- 3.2.1.3 Advancement in treatment modalities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Availability of alternative therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Non-surgical treatment

- 5.2.1 Medications

- 5.2.2 Physical therapy

- 5.2.3 Orthotics and braces

- 5.2.4 Other non-surgical treatments

- 5.3 Surgical treatment

- 5.3.1 Arthroscopic surgery

- 5.3.2 Open surgery

- 5.3.3 Other surgical treatments

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pediatric

- 6.3 Adult

- 6.4 Geriatric

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Orthopedic clinics

- 7.5 Homecare settings

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 BTL

- 9.3 DJO Global (Enovis)

- 9.4 Folsom Orthopaedics & Sports Medicine

- 9.5 GlaxoSmithKline

- 9.6 MedStar Health

- 9.7 Merck & Co

- 9.8 Novartis

- 9.9 Ossur Corporate

- 9.10 Pfizer

- 9.11 Pharmascience

- 9.12 ReLiva Physiotherapy & Rehab

- 9.13 Scandinavian Physiotherapy Center

- 9.14 Zimmer Biomet