肺炎球菌ワクチン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Pneumococcal Vaccine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708202

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

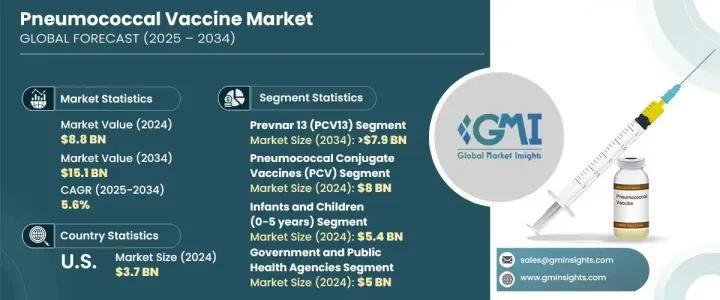

肺炎球菌ワクチンの世界市場は、2024年に88億米ドルと評価され、2025年から2034年にかけてCAGR 5.6%で成長すると予測されています。

肺炎球菌感染症の有病率の増加、ワクチン接種の重要性に関する一般市民の意識の高まり、世界の予防接種プログラムを推進する政府の積極的な取り組みなど、いくつかの要因がこの成長を後押ししています。ワクチン接種率の急上昇は、特に小児やハイリスク集団に対する義務的なワクチン接種スケジュールを実施するヘルスケア当局の取り組みが活発化していることに起因しています。研究開発の継続的な進歩により、より効果的で革新的な肺炎球菌ワクチンが製造され、より幅広い血清型に対応しています。これらのワクチンは、肺炎球菌によって引き起こされる肺炎、髄膜炎、敗血症などの生命を脅かす疾患の発生率を減少させる上で重要な役割を果たしています。

各国政府が予防ヘルスケアを優先し、肺炎球菌ワクチンを定期的な予防接種スケジュールに組み込んでいるため、市場の需要は大幅に増加すると予想されます。免疫不全患者や高齢者への予防接種がますます重視されるようになり、ワクチン製造業者にとって新たな機会が生まれています。さらに、製薬会社は国際保健機関と緊密に連携し、肺炎球菌感染症が公衆衛生上の大きな懸念であり続ける低所得地域において、これらのワクチンへのアクセスを拡大しようとしています。ワクチン研究への資金調達の増加と、新たな血清型をカバーする広域スペクトラムワクチンの開発イニシアティブが相まって、今後10年間の市場成長はさらに促進されると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 88億米ドル |

| 予測金額 | 151億米ドル |

| CAGR | 5.6% |

肺炎球菌ワクチンは、重症細菌感染症の予防に大きく貢献しています。最も広く使用されているワクチンのひとつである肺炎球菌ワクチンは、顕著な成長が見込まれ、CAGR 5.8%、2034年までに79億米ドルの売上が予測されます。複数の肺炎球菌血清型に対する有効性が証明されていることから、特に小児やハイリスクの成人集団で広く採用されています。同ワクチンは長期にわたって免疫を獲得できるため、ヘルスケアプロバイダーや政府による予防接種キャンペーンで好んで使用されています。肺炎、敗血症、髄膜炎を含む重症肺炎球菌性疾患に対する幅広い適用範囲により、このワクチンは世界の予防接種プログラムにおける地位を強化し続けています。

肺炎球菌ワクチン市場は、主に結合型ワクチンと多糖体ワクチンの2種類に分けられます。結合型ワクチンは、肺炎球菌感染症に対する予防効果が長期間持続することから、2024年には80億米ドルの売上を計上し、市場を席巻しました。特に5歳未満の小児における肺炎球菌性疾患の予防効果が高いことが、需要の増加に拍車をかけています。さらに、成人集団、特に免疫力が低下している人々や高齢者への適用拡大が、結合型ワクチンの採用を加速させています。肺炎球菌感染症の全体的な負担を軽減するその能力により、肺炎球菌ワクチンは定期的な予防接種スケジュールに望ましい選択肢として定着しています。

米国の肺炎球菌ワクチン市場は、2024年に37億米ドルを創出しました。高齢者は免疫機能の低下により肺炎球菌感染症に罹患するリスクが高いためです。予防ヘルスケアへの取り組みと全国的なワクチン接種プログラムにより、ワクチンの摂取率が大幅に上昇し、高リスク集団に対する予防効果が高まっています。製薬会社と政府機関は、より広範な肺炎球菌血清型を標的とする新しいワクチンの開発に継続的に取り組むことで、ワクチン接種率を高め続けており、市場の長期的な拡大をさらに後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 成長促進要因

- 肺炎球菌性疾患の有病率の増加

- 政府の予防接種プログラムとイニシアチブ

- 高齢化人口の増加

- 技術の進歩と新製品の発売

- 業界の潜在的リスク&課題

- ワクチンの高コスト

- ワクチン接種のためらいと認知度の低さ

- 成長促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- パイプライン分析

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ニューモシル(PCV10)

- ニューモバックス23(PPSV23)

- プレブナー13(PCV13)

- プレブナー20(PCV20)

- シンフロリックス(PCV10)

- バクスニューバンス(PCV15)

- その他の製品

第6章 市場推計・予測:ワクチンタイプ別、2021年~2034年

- 主要動向

- 肺炎球菌結合型ワクチン(PCV)

- 肺炎球菌多糖体ワクチン(PPSV)

第7章 市場推計・予測:年齢層別、2021年~2034年

- 主要動向

- 乳幼児・小児(0~5歳)

- 成人(18~64歳)

- 高齢者(65歳以上)

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- 政府・公衆衛生機関

- eコマース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Beijing Minhai Biological Technology

- Bio-Manguinhos/Fiocruz

- GlaxoSmithKline

- Merck &Co.

- Pfizer

- Serum Institute of India

- Walvax Biotechnology

目次

The Global Pneumococcal Vaccine Market was valued at USD 8.8 billion in 2024 and is projected to grow at a CAGR of 5.6% between 2025 and 2034. Several factors are driving this growth, including the increasing prevalence of pneumococcal infections, rising public awareness about the importance of vaccination, and favorable government initiatives promoting immunization programs worldwide. The surge in vaccination rates can be attributed to growing efforts by healthcare authorities to implement mandatory vaccination schedules, particularly for children and high-risk populations. Ongoing advancements in research and development are leading to the production of more effective and innovative pneumococcal vaccines, catering to a wider range of serotypes. These vaccines play a crucial role in reducing the incidence of life-threatening conditions such as pneumonia, meningitis, and sepsis caused by Streptococcus pneumoniae.

As governments prioritize preventive healthcare and integrate pneumococcal vaccines into routine immunization schedules, market demand is set to rise significantly. The increasing focus on immunizing immunocompromised individuals and elderly populations is creating new opportunities for vaccine manufacturers. Furthermore, pharmaceutical companies are working closely with global health organizations to expand access to these vaccines in low-income regions, where pneumococcal diseases remain a major public health concern. Rising funding for vaccine research, coupled with initiatives to develop broad-spectrum vaccines that cover emerging serotypes, is expected to further boost market growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.8 Billion |

| Forecast Value | $15.1 Billion |

| CAGR | 5.6% |

The market is segmented based on product, with various pneumococcal vaccines contributing significantly to preventing severe bacterial infections. One of the most widely used vaccines is expected to experience notable growth, with a projected CAGR of 5.8%, generating USD 7.9 billion by 2034. Its proven efficacy in protecting against multiple Streptococcus pneumoniae serotypes has led to widespread adoption, especially in pediatric and high-risk adult populations. The vaccine's ability to provide long-term immunity makes it a preferred choice among healthcare providers and government vaccination campaigns. With its broad coverage against severe pneumococcal diseases, including pneumonia, sepsis, and meningitis, this vaccine continues to strengthen its position in global immunization programs.

The pneumococcal vaccine market is divided into two main types: conjugate vaccines and polysaccharide vaccines. Conjugate vaccines dominated the market in 2024, generating USD 8 billion due to their ability to offer long-lasting protection against pneumococcal infections. Their high effectiveness in preventing pneumococcal diseases, especially among children under five years old, has fueled their growing demand. Additionally, expanding applications among adult populations, particularly those with weakened immune systems and elderly individuals, are accelerating the adoption of conjugate vaccines. Their ability to reduce the overall burden of pneumococcal diseases has established them as the preferred choice for routine immunization schedules.

The U.S. pneumococcal vaccine market generated USD 3.7 billion in 2024. The rising elderly population in the country has been a key driver of this growth, as aging individuals face a higher risk of contracting pneumococcal infections due to declining immune function. Preventive healthcare efforts and nationwide vaccination programs have significantly increased vaccine uptake, ensuring better protection for high-risk populations. Pharmaceutical companies and government agencies continue to enhance vaccine coverage, with ongoing efforts to develop newer vaccines that target a broader range of pneumococcal serotypes, further supporting the market's long-term expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of pneumococcal diseases

- 3.2.1.2 Government immunization programs and initiatives

- 3.2.1.3 Growing aging population

- 3.2.1.4 Technological advancements and new product launches

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of vaccines

- 3.2.2.2 Vaccine hesitancy and low awareness

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pneumosil (PCV10)

- 5.3 Pneumovax 23 (PPSV23)

- 5.4 Prevnar 13 (PCV13)

- 5.5 Prevnar 20 (PCV20)

- 5.6 Synflorix (PCV10)

- 5.7 Vaxneuvance (PCV15)

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Vaccine Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pneumococcal conjugate vaccines (PCV)

- 6.3 Pneumococcal polysaccharide vaccines (PPSV)

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Infants and children (0–5 years)

- 7.3 Adults (18–64 years)

- 7.4 Elderly (65+ years)

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Government and public health agencies

- 8.5 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Beijing Minhai Biological Technology

- 10.2 Bio-Manguinhos/Fiocruz

- 10.3 GlaxoSmithKline

- 10.4 Merck & Co.

- 10.5 Pfizer

- 10.6 Serum Institute of India

- 10.7 Walvax Biotechnology

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日