|

市場調査レポート

商品コード

1708194

商用車用尿素タンク市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Commercial Vehicle Urea Tank Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 商用車用尿素タンク市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月17日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

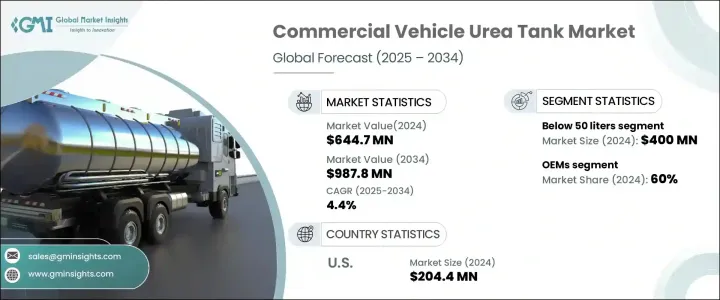

商用車用尿素タンクの世界市場は2024年に6億4,470万米ドルに達し、2025年から2034年にかけてCAGR 4.4%で成長すると予測されています。

市場成長の主な要因は、厳しい環境規制、選択的触媒還元(SCR)システムの採用増加、有害な窒素酸化物(NOx)排出量削減への取り組み強化などです。欧州連合(EU)、インド、中国など世界各国の政府・規制機関は、Euro VI、Bharat Stage VI(BS-VI)、China VIなどの厳しい排出基準を実施しており、商用車メーカーは高度な尿素噴射技術を統合する必要があります。これらのシステムは、排ガス規制への適合を確保しながら、燃料効率と性能を向上させる。

さらに、NOx排出が公衆衛生や環境に及ぼす悪影響に対する意識の高まりが、SCRシステムを搭載した車両への投資をフリート事業者に促しています。規制要件に適合した低燃費車両に対する需要の高まりは、尿素タンクの採用をさらに促進し、市場の持続的成長を位置づけています。先進的な排出ガス制御システムを搭載した新型モデルへの旧型商用車の置き換えが進んでいることも、市場の上昇に寄与している要因です。eコマースや都市型配送サービスの拡大など、物流・輸送分野の動向の変化も、効率的な排出ガス制御システムを搭載した商用車の需要を押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億4,470万米ドル |

| 予測金額 | 9億8,780万米ドル |

| CAGR | 4.4% |

商用車用尿素タンク市場は、容量別に50リットル未満、50~100リットル、100リットル以上の3つに区分されます。50リットル未満セグメントは2024年に4億米ドルを生み出し、配送バンや都市バスなどの小型・中型商用車に広く適用されているため、引き続き市場を独占しています。これらの車両は短距離路線を運行するため、尿素タンクの小型化による車両重量の軽減、燃料効率の向上、運行コストの削減といったメリットがあります。小型タンク製造の費用対効果と都市輸送ニーズへの適合性が、このセグメントの成長を促進しています。

市場は販売チャネルによっても区分され、OEM(相手先ブランド製造)とアフターマーケットが主要な貢献者となっています。OEM部門は2024年に60%の市場シェアを占めるが、これは主に新しく製造される商用車へのSCRシステムの統合が進んでいるためです。より厳しい排ガス規制が義務化されるにつれて、SCR技術は新車の標準装備となりつつあり、OEMが直接供給する尿素タンクへの安定した需要を牽引しています。OEM供給部品が好まれるのは、その高品質基準、車種との互換性、排ガス規制を満たす信頼性に起因します。

米国の商用車用尿素タンク市場は、2024年に2億440万米ドルを生み出し、2025年から2034年にかけてCAGR 4.7%で成長すると予想されています。この成長の原動力は、環境保護庁(EPA)などの機関が施行する厳しい排出規制と、商用車におけるSCRシステムの使用の増加です。EPAの温室効果ガス・フェーズ2規制とカリフォルニア州大気資源局(CARB)の義務化により、小型商用車と大型商用車の両方で尿素タンクの需要が大幅に増加しています。米国がよりクリーンな輸送技術と排出基準の強化を推進し続ける中、高性能尿素タンクの需要は着実に増加し、今後数年間の市場の成長をさらに高めると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料メーカー

- 部品メーカー

- メーカー

- 技術プロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの状況

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- コスト内訳分析

- 主要ニュース&イニシアティブ

- 影響要因

- 促進要因

- 商用車生産台数の伸びとフリートの拡大

- 尿素タンク技術の進歩

- 厳しい排ガス規制

- 物流・輸送産業の拡大

- 業界の潜在的リスク&課題

- SCRシステムと尿素タンクの初期コストの高さ

- 尿素の結晶化と凍結の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 50リットル未満

- 50~100リットル

- 100リットル以上

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ステンレス

- プラスチック

- 複合材料

第7章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- ACGB

- Amphenol

- Centro Incorporated

- Cummins

- Dongguan Zhengyang Electronic Mechanical(KUS Auto)

- Elkamet

- Elkhart Plastics

- Gemini Group

- Hitachi Zosen

- ITB Group

- KaiLong

- Kingspan

- Robert Bosch

- Rochling

- Salzburger Aluminium

- Scania AB

- Shaw Development

- Solar Plastics

- SSI Technologies

- Yara International ASA

The Global Commercial Vehicle Urea Tank Market reached USD 644.7 million in 2024 and is projected to grow at a CAGR of 4.4% between 2025 and 2034. The market growth is primarily driven by stringent environmental regulations, rising adoption of selective catalytic reduction (SCR) systems, and increasing efforts to reduce harmful nitrogen oxide (NOx) emissions. Governments and regulatory bodies worldwide, such as the European Union, India, and China, are enforcing strict emission standards, including Euro VI, Bharat Stage VI (BS-VI), and China VI, which require commercial vehicle manufacturers to integrate advanced urea injection technologies. These systems enhance fuel efficiency and performance while ensuring compliance with emission norms.

Additionally, rising awareness about the adverse effects of NOx emissions on public health and the environment is encouraging fleet operators to invest in vehicles equipped with SCR systems. Growing demand for fuel-efficient vehicles that comply with regulatory requirements is further driving the adoption of urea tanks, positioning the market for sustained growth. The increasing replacement of older commercial vehicles with newer models featuring advanced emission control systems is another factor contributing to the market's upward trajectory. Evolving trends in the logistics and transportation sectors, including the expansion of e-commerce and urban delivery services, are also boosting the demand for commercial vehicles with efficient emission control systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $644.7 Million |

| Forecast Value | $987.8 Million |

| CAGR | 4.4% |

The commercial vehicle urea tank market is segmented by capacity into three categories: below 50 liters, 50 to 100 liters, and above 100 liters. The below 50 liters segment generated USD 400 million in 2024 and continues to dominate the market due to its widespread application in light and medium-duty commercial vehicles, such as delivery vans and urban buses. These vehicles operate on shorter routes and benefit from smaller urea tanks that reduce vehicle weight, enhance fuel efficiency, and lower operational costs. The cost-effectiveness of manufacturing smaller tanks and their compatibility with urban transport needs are driving this segment's growth.

The market is also divided based on sales channels, with Original Equipment Manufacturers (OEMs) and the aftermarket being the key contributors. The OEMs segment held a 60% market share in 2024, largely due to the increasing integration of SCR systems in newly manufactured commercial vehicles. As stricter emission standards become mandatory, SCR technology is becoming a standard feature in new vehicles, driving consistent demand for urea tanks supplied directly by OEMs. The preference for OEM-supplied components stems from their high-quality standards, compatibility with vehicle models, and reliability in meeting emission regulations.

The U.S. commercial vehicle urea tank market generated USD 204.4 million in 2024 and is expected to grow at a CAGR of 4.7% between 2025 and 2034. This growth is fueled by stringent emission regulations enforced by agencies such as the Environmental Protection Agency (EPA) and the increasing use of SCR systems in commercial vehicles. The implementation of the EPA's Greenhouse Gas Phase 2 regulations and California Air Resources Board (CARB) mandates has significantly boosted the demand for urea tanks in both light and heavy commercial vehicles. As the U.S. continues to push for cleaner transportation technologies and tighter emission standards, the demand for high-performance urea tanks is expected to rise steadily, further enhancing the growth of the market in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growth in commercial vehicle production & fleet expansion

- 3.7.1.2 Advancements in urea tank technology

- 3.7.1.3 Stringent emission regulations

- 3.7.1.4 Expansion of logistics & transportation industry

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs of SCR systems & urea tanks

- 3.7.2.2 Issues with urea crystallization & freezing

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Below 50 liters

- 5.3 50 to 100 liters

- 5.4 Above 100 liters

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Plastic

- 6.4 Composite

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Light Commercial Vehicles (LCV)

- 7.3 Medium Commercial Vehicles (MCV)

- 7.4 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ACGB

- 10.2 Amphenol

- 10.3 Centro Incorporated

- 10.4 Cummins

- 10.5 Dongguan Zhengyang Electronic Mechanical (KUS Auto)

- 10.6 Elkamet

- 10.7 Elkhart Plastics

- 10.8 Gemini Group

- 10.9 Hitachi Zosen

- 10.10 ITB Group

- 10.11 KaiLong

- 10.12 Kingspan

- 10.13 Robert Bosch

- 10.14 Rochling

- 10.15 Salzburger Aluminium

- 10.16 Scania AB

- 10.17 Shaw Development

- 10.18 Solar Plastics

- 10.19 SSI Technologies

- 10.20 Yara International ASA