|

市場調査レポート

商品コード

1708192

移動体通信アンテナ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Mobile Communication Antenna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 移動体通信アンテナ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月17日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

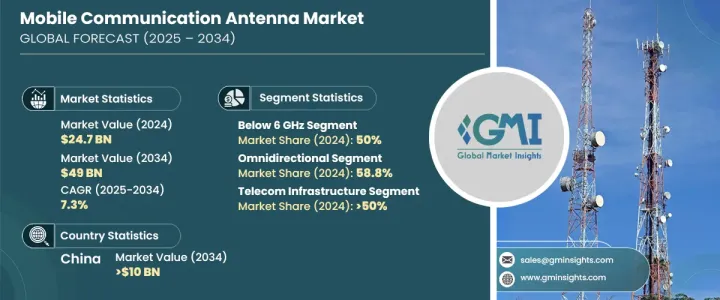

移動体通信アンテナの世界市場は、2024年に247億米ドルを生み出し、2025年から2034年にかけてCAGR 7.3%で成長すると予測されています。

5G技術の採用増加や様々な産業の急速なデジタル化に後押しされたスマートフォン需要の高まりが、市場成長を牽引しています。スマートフォンが高速インターネット、シームレス・ストリーミング、リアルタイム・アプリケーションをサポートするように進化するにつれ、高度で高性能な移動体通信アンテナのニーズは高まり続けています。5G対応デバイスの普及に伴い、通信事業者はより良い信号品質と強力な接続性を確保するため、アンテナネットワークを急速に拡大しています。また、モノのインターネット(IoT)やスマートデバイスの普及により、信頼性の高い移動体通信インフラへのニーズが高まり、アンテナ需要がさらに高まっています。

世界各国の政府や通信事業者は、5Gの展開に多額の投資を行い、既存のネットワークインフラをアップグレードし、6Gのような次世代技術の開発に注力しており、アンテナ設計の継続的な技術革新を推進しています。ネットワーク効率の向上とエネルギー消費の削減が重視されるようになったことで、都市部でも農村部でもシームレスなカバレッジを提供し、接続性を高めるエネルギー効率の高いアンテナシステムの採用が進んでいます。さらに、スマートシティ構想の台頭や、スマートホームシステムや産業オートメーションなどのコネクテッドデバイスの利用の増加が、移動体通信アンテナ市場の継続的な拡大に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 247億米ドル |

| 予測金額 | 490億米ドル |

| CAGR | 7.3% |

市場は周波数別に分類され、2024年には6GHz以下のセグメントが50%のシェアを占める。この周波数帯域は、4G LTEと5G展開の初期段階をサポートする上で重要な役割を果たしています。6GHz以下の周波数は、強力なカバレッジ、優れた屋内浸透性、信頼性の高い接続性を提供し、全国規模のモバイルネットワークに最適です。移動体通信事業者は、多様な地域で中断のないサービスを確保し、パフォーマンスを最適化することに取り組んでいるため、これらの周波数に対する需要は増加の一途をたどっています。6GHz以下とミリ波周波数を統合したハイブリッド・ネットワークの開発は、シームレスな接続性を確保し、市場拡大をさらに促進します。

アンテナの種類では、市場は無指向性アンテナと指向性アンテナに分けられ、2024年の市場シェアは無指向性アンテナが58.8%を占める。無指向性アンテナは、360度のカバレッジを提供できることから、通信インフラ、特に基地局やマクロセルで広く使用されています。モバイルネットワーク、IoTアプリケーション、スマートデバイスの普及が、無指向性アンテナの採用を促進しています。マルチバンドやエネルギー効率の高いアンテナ設計の技術的進歩は、消費電力を最小限に抑えながらネットワーク性能を向上させており、こうしたアンテナの需要をさらに押し上げています。

アジア太平洋の移動体通信アンテナ市場は、2024年には世界シェアの35%を占め、中国は2034年までに100億米ドルを生み出すと予測されています。同市場における中国のリーダーシップは、5G技術の積極的な展開、通信インフラへの多額の投資、デジタル化構想に対する政府の強力な支援によってもたらされています。5Gの展開を加速させ、6GとAI技術のイノベーションを推進する同国の動きは、先進的な移動体通信アンテナの需要を引き続き刺激し、同地域の主要促進要因としての地位を確固たるものにしています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- ネットワーク事業者

- インフラ事業者

- 規制機関

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主なニュースと取り組み

- ケーススタディ

- コスト内訳分析

- 規制状況

- 影響要因

- 促進要因

- スマートフォンの普及拡大

- IoTデバイスの増加

- 5Gネットワークの展開

- モバイルデータ利用の増加

- 業界の潜在的リスク&課題

- 開発・展開コストの高さ

- 技術的な複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:アンテナ別、2021年~2034年

- 主要動向

- 無指向性

- 指向性

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 基地局

- モバイル機器用アンテナ

- 屋内分散型アンテナ

- スモールセルアンテナ

第7章 市場推計・予測:周波数別、2021年~2034年

- 主要動向

- 6GHz未満

- 6 GHz~24 GHz

- 24 GHz~100 GHz

- 100GHz以上

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 通信インフラ

- IoTとスマートデバイス

- 自動車

- 防衛

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Alpha Wireless

- Amphenol Antenna Solutions

- Baylin Technologies

- Cobham Wireless

- CommScope

- Ericsson

- Huawei Technologies

- Infinite Electronics

- Laird Connectivity

- Molex

- Nokia

- PCTEL

- Qualcomm

- RFS(Radio Frequency Systems)

- Rohde &Schwarz

- Mobile Mark

- TAOGLAS

- TE Connectivity

- Tongyu Communication

- ZTE

The Global Mobile Communication Antenna Market generated USD 24.7 billion in 2024 and is expected to grow at a CAGR of 7.3% between 2025 and 2034. The rising demand for smartphones, fueled by the increasing adoption of 5G technology and the rapid digitalization of various industries, is driving market growth. As smartphones evolve to support high-speed internet, seamless streaming, and real-time applications, the need for advanced and high-performance mobile communication antennas continues to rise. With the proliferation of 5G-enabled devices, telecom operators are rapidly expanding antenna networks to ensure better signal quality and stronger connectivity. In addition, the Internet of Things (IoT) and smart devices have fueled the need for reliable mobile communication infrastructure, further boosting demand for antennas.

Governments and telecom operators worldwide are investing heavily in 5G deployments, upgrading existing network infrastructure, and focusing on developing next-generation technologies like 6G, driving continuous innovations in antenna designs. The growing emphasis on improving network efficiency and reducing energy consumption is leading to the adoption of energy-efficient antenna systems that provide seamless coverage and enhanced connectivity in urban and rural regions. Furthermore, the rise of smart city initiatives and the increasing use of connected devices, including smart home systems and industrial automation, are contributing to the ongoing expansion of the mobile communication antenna market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.7 Billion |

| Forecast Value | $49 Billion |

| CAGR | 7.3% |

The market is categorized by frequency, with the below 6 GHz segment holding a 50% share in 2024. This frequency range plays a crucial role in supporting 4G LTE and the initial phases of 5G deployments. Frequencies below 6 GHz provide strong coverage, excellent indoor penetration, and reliable connectivity, making them ideal for nationwide mobile networks. As mobile operators work to ensure uninterrupted service and optimize performance across diverse regions, the demand for these frequencies continues to grow. The development of hybrid networks that integrate below 6 GHz and millimeter-wave frequencies ensures seamless connectivity, further driving market expansion.

In terms of antenna types, the market is divided into omnidirectional and directional antennas, with the omnidirectional segment accounting for 58.8% of the market share in 2024. Omnidirectional antennas are widely used in telecom infrastructure, particularly in base stations and macro cells, due to their ability to provide 360-degree coverage. The growing deployment of mobile networks, IoT applications, and smart devices is driving the adoption of omnidirectional antennas. Technological advancements in multi-band and energy-efficient antenna designs are enhancing network performance while minimizing power consumption, further boosting demand for these antennas.

The Asia Pacific mobile communication antenna market held 35% of the global share in 2024, with China projected to generate USD 10 billion by 2034. China's leadership in the market is driven by its aggressive rollout of 5G technology, substantial investments in telecom infrastructure, and strong government support for digitalization initiatives. The country's push to accelerate 5G deployment and advance innovations in 6G and AI technologies continues to fuel demand for advanced mobile communication antennas, solidifying its position as a major growth driver in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Network operators

- 3.1.2 Infrastructure providers

- 3.1.3 Regulatory bodies

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Case studies

- 3.8 Cost breakdown analysis

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing smartphone adoption

- 3.10.1.2 Growing proliferation of IoT devices

- 3.10.1.3 Deployment of 5G networks

- 3.10.1.4 Rise in mobile data usage

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High costs of development and deployment

- 3.10.2.2 Technical complexity

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Antenna, 2021 – 2034 (USD Billion, Units)

- 5.1 Key trends

- 5.2 Omnidirectional

- 5.3 Directional

Chapter 6 Market Estimates & Forecast, By Application, 2021 – 2034 (USD Billion, Units)

- 6.1 Key trends

- 6.2 Base station

- 6.3 Mobile device antennas

- 6.4 Indoor distributed antennas

- 6.5 Small cell antennas

Chapter 7 Market Estimates & Forecast, By Frequency, 2021 – 2034 (USD Billion, Units)

- 7.1 Key trends

- 7.2 Below 6 GHz

- 7.3 6 GHz to 24 GHz

- 7.4 24 GHz to 100 GHz

- 7.5 Above 100 GHz

Chapter 8 Market Estimates & Forecast, By End Use, 2021 – 2034 (USD Billion, Units)

- 8.1 Key trends

- 8.2 Telecom infrastructure

- 8.3 IoT and smart devices

- 8.4 Automotive

- 8.5 Defense

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alpha Wireless

- 10.2 Amphenol Antenna Solutions

- 10.3 Baylin Technologies

- 10.4 Cobham Wireless

- 10.5 CommScope

- 10.6 Ericsson

- 10.7 Huawei Technologies

- 10.8 Infinite Electronics

- 10.9 Laird Connectivity

- 10.10 Molex

- 10.11 Nokia

- 10.12 PCTEL

- 10.13 Qualcomm

- 10.14 RFS (Radio Frequency Systems)

- 10.15 Rohde & Schwarz

- 10.16 Mobile Mark

- 10.17 TAOGLAS

- 10.18 TE Connectivity

- 10.19 Tongyu Communication

- 10.20 ZTE