|

市場調査レポート

商品コード

1708188

整形外科スマートインプラント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Smart Orthopedic Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 整形外科スマートインプラント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

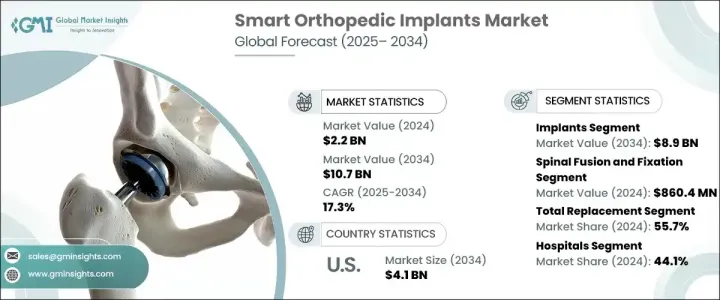

整形外科スマートインプラントトの世界市場は、2024年には22億米ドルと評価され、2025年から2034年にかけてCAGR 17.3%で成長すると予測されています。

整形外科スマートインプラントは、筋骨格系の状態を監視、診断、治療成果を高めるセンサーと接続機能を備えた革新的な医療機器です。これらのインプラントは、荷重、アライメント、治癒経過などの測定基準に関するリアルタイムデータを提供し、患者に合わせた治療を可能にし、治療効率を向上させる。個別化ヘルスケアに対する需要の高まりは、技術の進歩と相まって、これらのインプラントの採用を促進し、市場の大幅な成長に寄与しています。筋骨格系障害の症例の増加と老年人口の増加が、さらに需要を煽っています。変形性関節症、骨粗しょう症、骨折などの治療は、高齢化、座りっぱなしのライフスタイル、肥満によってますます一般的になっており、効果的な治療ソリューションの必要性を高めています。

市場はコンポーネントによって区分され、インプラントと電子部品が主なカテゴリーです。インプラントは2024年の市場収益の83.4%を占め、2034年には89億米ドルに達すると予測されています。これらのインプラント、特に人工膝関節や人工股関節は、骨の退行性疾患の治療に広く使用されており、市場の優位性を牽引しています。センサーや人工知能(AI)のような先進技術の統合は、インプラントの性能を向上させ、より良い患者の転帰とより高い採用率につながっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 107億米ドル |

| CAGR | 17.3% |

用途別では、整形外科スマートインプラント市場には脊椎固定、VCF治療、運動温存/非固定、脊椎除圧が含まれます。脊椎固定術と固定術は2024年に8億6,040万米ドルで市場を独占しました。これらの処置は、椎間板ヘルニア、脊柱側弯症、脊柱管狭窄症の治療に一般的に使用され、特に高齢化が進んでいます。リアルタイムのモニタリング用センサーの統合と固定技術の向上により、これらの手技の有効性が強化され、引き続き市場をリードしています。

手技タイプ別に分けると、全置換術、部分置換術、その他の手技があります。全置換術が支配的なセグメントとして浮上し、2024年には売上シェアの55.7%を占め、2034年には59億米ドルに達すると推定されています。退行性関節疾患の罹患率の上昇と人口の高齢化が、特に膝関節の全置換術の需要を牽引しています。これらの人工関節置換術は、重度の関節疾患に対する包括的なソリューションを提供し、より優れた機能性と長期的な救済を提供するため、市場の優位性が強化されています。

最終用途に基づき、市場は病院、外来手術センター、専門クリニック、その他の施設に区分されます。病院は、複雑な手術を管理し、包括的な術後ケアを提供する能力があるため、2024年には44.1%の最大の売上シェアを占めました。高度な手術能力、専門機器、集学的ケアにより、スマートインプラントを含む整形外科手術に好んで選ばれています。

米国では、整形外科スマートインプラントト市場は2023年に7億4,850万米ドルを占め、2034年には41億米ドルに達する大幅な成長が見込まれています。同国はヘルスケア革新に重点を置いており、強固なインフラ、広範な保険適用、最先端の整形外科ソリューションに対する認知度の向上が、多様な患者層における整形外科スマートインプラントの採用を後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 筋骨格系障害の有病率の増加

- 先進国および新興経済諸国における高齢者人口の増加

- 個別化医療へのシフト

- スマートインプラント分野における技術の進歩

- 業界の潜在的リスク&課題

- 厳しい規制の枠組み

- インプラントの高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 今後の市場動向

- ギャップ分析

- 技術的展望

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- インプラント

- 人工膝関節置換術

- 人工股関節置換術

- 脊椎固定術

- 骨折固定

- その他のインプラント

- 電子部品

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 脊椎固定

- VCF治療

- 運動温存/非固定

- 脊椎減圧術

第7章 市場推計・予測:手技タイプ別、2021年~2034年

- 主要動向

- 全置換術

- 部分置換術

- その他の処置タイプ

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Canary Medical

- Exactech

- Medtronic

- SpineGuard

- Stryker

- Zimmer Biomet

The Global Smart Orthopedic Implants Market was valued at USD 2.2 billion in 2024 and is expected to grow at a CAGR of 17.3% from 2025 to 2034. Smart orthopedic implants are innovative medical devices equipped with sensors and connectivity features that monitor, diagnose, and enhance treatment outcomes for musculoskeletal conditions. These implants offer real-time data on metrics such as load, alignment, and healing progress, enabling personalized patient care and improving treatment efficiency. Increasing demand for personalized healthcare, coupled with advancements in technology, is driving the adoption of these implants, contributing to significant market growth. Rising cases of musculoskeletal disorders and a growing geriatric population further fuel the demand. Conditions such as osteoarthritis, osteoporosis, and fractures are becoming increasingly common due to aging, sedentary lifestyles, and obesity, boosting the need for effective treatment solutions.

The market is segmented based on components, with implants and electronic components as the primary categories. Implants accounted for 83.4% of the market revenue in 2024 and are projected to reach USD 8.9 billion by 2034. These implants, particularly for knee and hip replacements, are widely used to treat degenerative bone conditions, which drives their market dominance. The integration of advanced technologies like sensors and artificial intelligence (AI) enhances implant performance, leading to better patient outcomes and greater adoption rates.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 17.3% |

By application, the smart orthopedic implants market includes spinal fusion and fixation, VCF treatment, motion preservation/non-fusion, and spinal decompression. Spinal fusion and fixation dominated the market with a value of USD 860.4 million in 2024. These procedures are commonly used to treat herniated discs, scoliosis, and spinal stenosis, particularly among the aging population. The integration of sensors for real-time monitoring and improved fixation techniques enhances the effectiveness of these procedures, ensuring their continued market leadership.

When segmented by procedure type, the market includes total replacement, partial replacement, and other procedures. Total replacement emerged as the dominant segment, accounting for 55.7% of the revenue share in 2024, and is estimated to reach USD 5.9 billion by 2034. The rising incidence of degenerative joint diseases and an aging population drive the demand for total replacement procedures, particularly for knee joints. These procedures provide comprehensive solutions for severe joint conditions, offering better functionality and long-term relief, which reinforces their market dominance.

Based on end use, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and other facilities. Hospitals held the largest revenue share of 44.1% in 2024 due to their capability to manage complex surgeries and provide comprehensive post-operative care. Their advanced surgical capabilities, specialized equipment, and multidisciplinary care make them the preferred choice for orthopedic procedures involving smart implants.

In the United States, the smart orthopedic implants market accounted for USD 748.5 million in 2023 and is expected to grow significantly, reaching USD 4.1 billion by 2034. The country's emphasis on healthcare innovation, robust infrastructure, widespread insurance coverage, and increasing awareness of cutting-edge orthopedic solutions drive the adoption of smart orthopedic implants across diverse patient demographics.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of musculoskeletal disorders

- 3.2.1.2 Rising geriatric population in developed as well as developing economies

- 3.2.1.3 Shift towards personalized medicine

- 3.2.1.4 Technological advancements in the field of smart implants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost of implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Gap analysis

- 3.7 Technological landscape

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implants

- 5.2.1 Knee arthroplasty

- 5.2.2 Hip arthroplasty

- 5.2.3 Spine fusion

- 5.2.4 Fracture fixation

- 5.2.5 Other implants

- 5.3 Electronic components

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Spinal fusion and fixation

- 6.3 VCF treatment

- 6.4 Motion preservation/ non - fusion

- 6.5 Spinal decompression

Chapter 7 Market Estimates and Forecast, By Procedure Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Total replacement

- 7.3 Partial replacement

- 7.4 Other procedure types

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Specialty clinics

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Canary Medical

- 10.2 Exactech

- 10.3 Medtronic

- 10.4 SpineGuard

- 10.5 Stryker

- 10.6 Zimmer Biomet