|

市場調査レポート

商品コード

1708187

クラウドストレージサービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cloud Storage Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| クラウドストレージサービス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

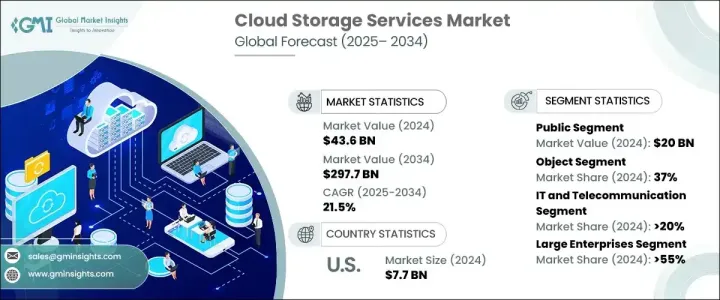

世界のクラウドストレージサービス市場は、2024年に436億米ドルと評価され、2025年から2034年にかけて21.5%のCAGRで成長すると予測されています。

リモートワークの増加により、クラウドストレージやファイル共有ソリューションの需要が高まっており、物理的にその場にいなくてもファイルの保存やアクセスができるようになっています。サービス・プロバイダーは、シームレスなファイル共有、安全なバックアップ、文書に関する容易なコラボレーションを可能にし、どこからでもファイルにリアルタイムでアクセスできるようにしています。クラウドストレージ・サービスの採用が拡大している背景には、ソーシャルメディア、デジタル・コンテンツ、IoT機器によって生成されるデータ量の増加もあります。スマート・ホーム・システムなどのIoT機器では大量のリアルタイム・データが収集されるため、拡張性の高いストレージ・ソリューションが必要となります。企業はクラウドストレージを利用して、こうしたデータを安全に保存・分析し、実用的な洞察を得ています。

メンテナンス・コストの削減も、クラウドストレージの採用を後押しする要因のひとつです。オンプレミスのデータ・ストレージ・インフラを維持するには、ハードウェア・メンテナンス、テクニカル・サポート、IT担当者など、多額の費用がかかります。クラウド・サービス・プロバイダーは、セキュリティ・パッチ、ソフトウェア・アップデート、ハードウェアの修理などのメンテナンスを行うため、専門の担当者は必要ないです。また、クラウドストレージ・システムは、ハードウェアの故障やデータ損失から保護するために、データ・リカバリーと冗長性を組み込んでいます。クラウド・プロバイダーは、異なる地域やデータセンター間でデータを複製し、シームレスな災害復旧プロセスを保証します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 436億米ドル |

| 予測金額 | 2,977億米ドル |

| CAGR | 21.5% |

パブリッククラウドサービスは、多要素認証(MFA)、データ暗号化、アクセス制御などのセキュリティ機能に重点的に投資しながら、世界なワークフォースのリモートアクセスとコラボレーションを可能にします。GDPR、HIPAA、ISO 27001などの業界標準や規制に準拠することで、データのセキュリティとプライバシーを確保しています。パブリック・クラウドストレージでは、企業はプロバイダーのデータセンターにデータを保存できるため、ハードウェアのメンテナンスやソフトウェアのアップデートが不要になります。パブリッククラウド環境とプライベートクラウド環境を組み合わせたハイブリッドクラウドモデルでは、必要に応じてワークロードを2つのクラウド間で移動できるため、運用の柔軟性が確保されます。

オブジェクト・ストレージ・システムは、メディアファイル、バックアップ、ログファイルなど、膨大な量の非構造化データを扱うように設計されています。そのアーキテクチャにより、企業は複雑な設定をすることなく、ストレージ容量をシームレスに拡張することができます。物理的なハードウェア・スケーリングが必要な従来のシステムとは異なり、オブジェクト・ストレージはそのプロセスを自動化します。ファイル・クラウドストレージは、そのリモートアクセスとセキュリティ強化により、市場で大きなシェアを維持すると予想されています。ユーザーはインターネット接続を通じて複数のデバイスからファイルにアクセスでき、プロバイダーは暗号化とMFAを提供して保護を強化しています。

ブロック・ストレージは、金融、ヘルスケア、ゲームなど、低遅延で高速なストレージを必要とする業界のデータ集約型アプリケーションに対応しています。これらの業界ではデータ量が増加しているため、高性能なブロック・ストレージ・ソリューションの需要は増加の一途をたどっています。コールドクラウドストレージは、アクセス頻度の低いデータに対して費用対効果が高く、その耐久性と複数の地域で利用可能なことから、大きな市場シェアを占めると予想されます。

クラウドストレージサービス市場は、BFSI、ヘルスケア、IT・通信、小売・消費財、メディア・エンターテインメント、製造、その他などの業界別で区分されます。IT・通信分野は2024年の市場シェアの20%以上を占め、顧客記録、ネットワークデータ、サービスログにクラウドストレージを活用しています。メディア・エンターテインメント企業も、高解像度のビデオコンテンツやオーディオファイルなどの大容量ファイルを管理するために、クラウドストレージに大きく依存しています。エンドユーザー別では、大企業が2024年に55%以上の市場シェアを占め、コンピューティング能力、ストレージ、ネットワーキング、セキュリティ、分析、災害復旧にクラウドサービスを活用しています。Infrastructure-as-a-Service(IaaS)およびSoftware-as-a-Service(SaaS)ソリューションは、クラウドを通じて仮想化されたコンピューティング・リソースと完全な管理アプリケーションを企業に提供します。

欧州は世界のクラウドストレージサービス市場の約25%を占めており、中でもドイツはデータプライバシー規制が厳しいため、大きな貢献をしています。GDPRの遵守により、クラウドプロバイダーはデータの暗号化、アクセス制御、監査証跡などの機能を提供し、データの安全性と規制の遵守を確保することが義務付けられています。欧州の企業では、厳しいデータセキュリティ要件に対応しつつ、コストとパフォーマンスのバランスを取るために、マルチクラウドやハイブリッドクラウド戦略を採用するケースが増えています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- クラウドストレージサービスプロバイダー

- クラウドストレージ・インフラストラクチャ・プロバイダー

- クラウド管理およびセキュリティ・サービス・プロバイダー

- 最終用途

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主なニュースと取り組み

- 使用事例

- 規制状況

- 影響要因

- 促進要因

- リモートワークの出現

- データ・セキュリティとバックアップに対する需要の高まり

- メンテナンスコストの削減

- データ復旧の容易さ

- 業界の潜在的リスク&課題

- メタデータの急増

- ランサムウェアの脅威

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- パブリック

- プライベート

- ハイブリッド

第6章 市場推計・予測:ストレージ別、2021年~2034年

- 主要動向

- オブジェクト

- ファイル

- ブロック

- コールド

第7章 市場推計・予測:業界別、2021年~2034年

- 主要動向

- BFSI

- ヘルスケア

- IT・通信

- 小売・消費財

- メディア・娯楽

- 製造業

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

- 個人

第9章 市場推計・予測:価格モデル別、2021年~2034年

- 主要動向

- 従量課金

- サブスクリプション型

- フリーミアム

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Adobe

- Alibaba

- Amazon

- Apple

- Backblaze

- Box

- Dell

- DigitalOcean

- Dropbox

- HPE

- IBM

- Microsoft

- Oracle

- OVHcloud

- pCloud

- RackSpace

- Tencent

- VMware

- Wasabi Technologies

The Global Cloud Storage Services Market was valued at USD 43.6 billion in 2024 and is projected to grow at a CAGR of 21.5% between 2025 and 2034. The rise of remote work has fueled the demand for cloud storage and file-sharing solutions, enabling teams to store and access files without being physically present. Service providers allow seamless file sharing, secure backups, and easy collaboration on documents, ensuring real-time access to files from any location. The growing adoption of cloud storage services is also driven by the increasing volume of data generated by social media, digital content, and IoT devices. Massive real-time data is collected by IoT devices, such as smart home systems, which require scalable storage solutions. Businesses use cloud storage to securely store and analyze this data for actionable insights.

Reduced maintenance costs are another factor driving cloud storage adoption. Maintaining an on-premise data storage infrastructure involves significant expenses, including hardware maintenance, technical support, and IT personnel. Cloud service providers handle maintenance, including security patches, software updates, and hardware repairs, eliminating the need for specialized personnel. Cloud storage systems also incorporate data recovery and redundancy to protect against hardware failures or data loss. Cloud providers replicate data across different regions or data centers, ensuring a seamless disaster recovery process.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $43.6 Billion |

| Forecast Value | $297.7 Billion |

| CAGR | 21.5% |

Public cloud services enable remote access and collaboration for global workforces while investing heavily in security features such as multi-factor authentication (MFA), data encryption, and access control. Compliance with industry standards and regulations like GDPR, HIPAA, and ISO 27001 ensures data security and privacy. Public cloud storage allows organizations to store data in the provider's data centers, eliminating the need for hardware maintenance or software updates. Hybrid cloud models, which combine public and private cloud environments, allow organizations to move workloads between the two as needed, ensuring operational flexibility.

Object storage systems are designed to handle vast amounts of unstructured data, such as media files, backups, and log files. Their architecture allows businesses to scale storage capacity seamlessly without complex configurations. Unlike traditional systems that require physical hardware scaling, object storage automates the process. File cloud storage is expected to maintain a significant share of the market due to its remote accessibility and enhanced security. Users can access files from multiple devices through an internet connection, and providers offer encryption and MFA for added protection.

Block storage caters to data-intensive applications in industries like finance, healthcare, and gaming that require high-speed storage with low latency. As these industries generate increasing amounts of data, the demand for high-performance block storage solutions continues to rise. Cold cloud storage, which is more cost-effective for infrequently accessed data, is anticipated to hold a significant market share due to its durability and availability across multiple regions.

The cloud storage services market is segmented by industry verticals, including BFSI, healthcare, IT and telecommunication, retail and consumer goods, media and entertainment, manufacturing, and others. The IT and telecommunication segment accounted for over 20% of the market share in 2024, utilizing cloud storage for customer records, network data, and service logs. Media and entertainment companies also rely heavily on cloud storage to manage large files, including high-resolution video content and audio files. By end-use, large enterprises held a market share of over 55% in 2024, leveraging cloud services for computing power, storage, networking, security, analytics, and disaster recovery. Infrastructure-as-a-Service (IaaS) and Software-as-a-Service (SaaS) solutions provide businesses with virtualized computing resources and complete managed applications through the cloud.

Europe holds approximately 25% of the global cloud storage services market, with Germany being a major contributor due to its strict data privacy regulations. GDPR compliance mandates that cloud providers offer features such as data encryption, access controls, and audit trails to ensure data security and regulatory adherence. European organizations increasingly adopt multi-cloud and hybrid cloud strategies to balance cost and performance while addressing stringent data security requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Cloud storage service providers

- 3.2.2 Cloud storage infrastructure providers

- 3.2.3 Cloud management and security service providers

- 3.2.4 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Use cases

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Emergence of remote work location

- 3.9.1.2 Rising demand for data security and back up

- 3.9.1.3 Less maintenance cost

- 3.9.1.4 Ease in data recovery

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Surge in Metadata

- 3.9.2.2 Threats of ransomware

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Public

- 5.3 Private

- 5.4 Hybrid

Chapter 6 Market Estimates & Forecast, By Storage, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Object

- 6.3 File

- 6.4 Block

- 6.5 Cold

Chapter 7 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Healthcare

- 7.4 IT and telecommunication

- 7.5 Retail and consumer goods

- 7.6 Media and entertainment

- 7.7 Manufacturing

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

- 8.4 Individual

Chapter 9 Market Estimates & Forecast, By Pricing Model, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Pay-as-you-go

- 9.3 Subscription-based

- 9.4 Freemium

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Adobe

- 11.2 Alibaba

- 11.3 Amazon

- 11.4 Apple

- 11.5 Backblaze

- 11.6 Box

- 11.7 Dell

- 11.8 DigitalOcean

- 11.9 Dropbox

- 11.10 Google

- 11.11 HPE

- 11.12 IBM

- 11.13 Microsoft

- 11.14 Oracle

- 11.15 OVHcloud

- 11.16 pCloud

- 11.17 RackSpace

- 11.18 Tencent

- 11.19 VMware

- 11.20 Wasabi Technologies