金属化バリアフィルム包装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Metalized Barrier Film Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708186

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

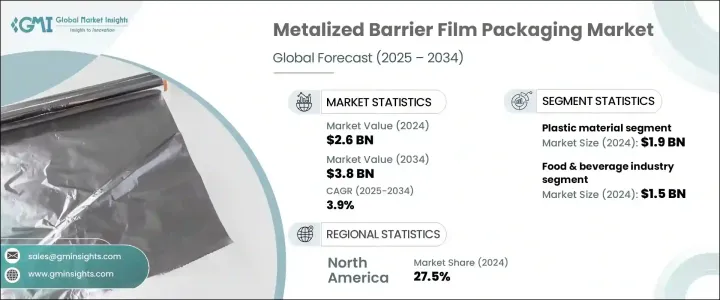

金属化バリアフィルム包装の世界市場は、2024年に26億米ドルと評価され、2025年から2034年にかけてCAGR 3.9%で成長すると予測されています。

この成長の主な要因は、製薬業界からの需要の高まりと、さまざまな分野での保存期間延長ニーズの高まりです。金属化バリアフィルムは、環境要因から高い保護を提供し、パッケージ商品の鮮度、風味、栄養品質を保持します。世界化が進み、包装食品や加工食品に対する消費者の嗜好が高まるにつれ、製造業者は、輸送時間が長くなっても製品の完全性を確保できるこれらのフィルムに注目するようになっています。特に製薬分野では、ブリスターパックや医療用パウチにおいてこれらのフィルムの恩恵を受けており、繊細な医薬品を確実に保護しています。ハイバリア・ソリューションと規制基準の遵守に重点を置くメーカーは、この分野での採用が増えると思われます。

賞味期限延長のニーズも市場拡大を後押しする重要な要因です。これらのフィルムは、包装された食品、医薬品、化粧品を効果的に保護し、腐敗を防ぎ、長期にわたって品質を維持します。消費者のライフスタイルがより速いペースで変化するにつれて、調理済み食品や加工食品への志向が高まり、先進パッケージング・ソリューションへの需要が高まっています。加えて、eコマースや国際貿易の増加により、輸送や保管中に製品を保護する堅牢なバリアフィルムのニーズが高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億米ドル |

| 予測金額 | 38億米ドル |

| CAGR | 3.9% |

市場は材料別に区分され、プラスチックがこの分野を支配し、2024年には19億米ドルを占める。プラスチックベースの金属化フィルムは、その軽量性、コスト効率、柔軟性により好まれています。消費者が持ち運び可能で便利な包装を選ぶようになるにつれ、フレキシブル・プラスチック・フィルムが牽引力を増しています。製品の鮮度を維持しながら防腐剤の必要性を減らすことができるため、大量生産用途に最適です。この動向は、品質保持のために優れた包装を必要とする調理済み食品や飲食品の人気の高まりによってさらに後押しされています。

最終用途産業別では、飲食品セグメントが最大の貢献者で、2024年の評価額は15億米ドルです。このセグメントの成長は、急速な都市化と消費者の習慣の変化によるもので、包装されたすぐに食べられる製品が好まれます。金属化バリアフィルムは、スナック菓子、コーヒー、乳製品、その他の包装食品に広く使用され、化学保存料に頼らずに鮮度を保ち、腐敗を防止します。持続可能なパッケージングを重視する規制の高まりと、環境に優しいソリューションを求める消費者の需要が、このセグメントの採用をさらに後押ししています。

北米は2024年に世界市場シェアの27.5%を占め、バリア性の高いパッケージングに対するニーズの高まりとeコマース部門の急成長がその原動力となっています。持続可能な包装材料の採用に対する政府の支援と消費者の嗜好の変化が、金属化バリアフィルム包装の採用を促進しています。米国は2024年に5億2,390万米ドルを占め、この地域市場をリードしています。輸送中に製品の完全性を維持するために高性能包装を必要とする包装食品の需要増がその要因です。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 賞味期限延長に対する需要の高まり

- 持続可能なバリアコーティングの進歩

- eコマースと食品宅配サービスの活況

- 急速な都市化と多忙なライフスタイル

- 医薬品包装の需要拡大

- 業界の潜在的リスク&課題

- リサイクルの限界と持続可能性の問題

- 生分解性代替品との競合

- 促進要因

- 成長の可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- プラスチック

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- ポリアミド(PA)

- ポリエチレン(PE)

- ナイロン

- その他

- 金属

第6章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 飲食品

- 医薬品

- エレクトロニクス

- パーソナルケアと化粧品

- その他

第7章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Aerolam Group

- Amcor

- Cosmo Films

- Dunmore

- Ester Industries

- Finfoil

- Flex Films

- Jindal Films

- Kolon Industries

- Nahar PolyFilms

- PC Laminations

- SRF

- Sumilon Group

- Taghleef Industries

- Toray

- Zhejiang Changyu New Materials

目次

The Global Metalized Barrier Film Packaging Market, valued at USD 2.6 billion in 2024, is expected to grow at a CAGR of 3.9% from 2025 to 2034. This growth is primarily driven by rising demand from the pharmaceutical industry and the increasing need for extended shelf life across various sectors. Metalized barrier films provide high protection against environmental factors, preserving the freshness, flavor, and nutritional quality of packaged goods. As globalization and consumer preferences for packaged and processed foods increase, manufacturers are turning to these films to ensure product integrity during extended transit times. The pharmaceutical sector, in particular, benefits from these films in blister packs and medical pouches, ensuring the protection of sensitive drugs. Manufacturers focusing on high-barrier solutions and adherence to regulatory standards will see increased adoption in this sector.

The need for longer shelf life is another significant factor fueling market expansion. These films effectively safeguard packaged foods, pharmaceuticals, and cosmetics, preventing spoilage and maintaining quality over time. As consumer lifestyles become more fast-paced, there is a greater inclination toward ready-to-eat and processed food products, driving demand for advanced packaging solutions. In addition, the rise in e-commerce and global trade has heightened the need for robust barrier films to protect products during transportation and storage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 3.9% |

The market is segmented by material, with plastic dominating this space, accounting for USD 1.9 billion in 2024. Plastic-based metalized films are preferred due to their lightweight nature, cost-efficiency, and flexibility. As consumers increasingly opt for portable and convenient packaging, flexible plastic films gain traction. Their ability to reduce the need for preservatives while maintaining product freshness makes them ideal for high-volume applications. This trend is further supported by the growing popularity of ready-to-eat foods and beverages, which require superior packaging to retain their quality.

By end-use industry, the food and beverage segment is the largest contributor, with a valuation of USD 1.5 billion in 2024. The segment's growth is attributed to rapid urbanization and changing consumer habits, which favor packaged and ready-to-eat products. Metalized barrier films are widely used in snacks, coffee, dairy, and other packaged foods, preserving freshness and preventing spoilage without relying on chemical preservatives. Increasing regulatory emphasis on sustainable packaging and consumer demand for eco-friendly solutions further boost adoption in this segment.

North America held 27.5% of the global market share in 2024, driven by the rising need for high-barrier packaging and the rapid growth of the e-commerce sector. Government support for adopting sustainable packaging materials, combined with changing consumer preferences, is promoting the adoption of metalized barrier film packaging. The United States led the regional market, accounting for USD 523.9 million in 2024, fueled by the growing demand for packaged foods that require high-performance packaging to maintain product integrity during transportation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for extended shelf life

- 3.2.1.2 Advancements in sustainable barrier coatings

- 3.2.1.3 Booming e-commerce & food delivery services

- 3.2.1.4 Rapid urbanization and busy lifestyles

- 3.2.1.5 Growing demand in pharmaceutical packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited recycling & sustainability issues

- 3.2.2.2 Competition from biodegradable alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastics

- 5.2.1 Polypropylene (PP)

- 5.2.2 Polyethylene Terephthalate (PET)

- 5.2.3 Polyamide (PA)

- 5.2.4 Polyethylene (PE)

- 5.2.5 Nylon

- 5.2.6 Others

- 5.3 Metals

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Pharmaceuticals

- 6.4 Electronics

- 6.5 Personal care and cosmetics

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Aerolam Group

- 8.2 Amcor

- 8.3 Cosmo Films

- 8.4 Dunmore

- 8.5 Ester Industries

- 8.6 Finfoil

- 8.7 Flex Films

- 8.8 Jindal Films

- 8.9 Kolon Industries

- 8.10 Nahar PolyFilms

- 8.11 PC Laminations

- 8.12 SRF

- 8.13 Sumilon Group

- 8.14 Taghleef Industries

- 8.15 Toray

- 8.16 Zhejiang Changyu New Materials

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日