|

市場調査レポート

商品コード

1708185

リンパ腫治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Lymphoma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| リンパ腫治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

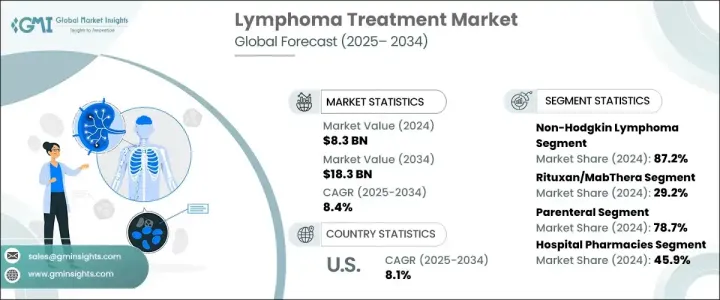

世界のリンパ腫治療市場は2024年に83億米ドルに達し、2025年から2034年にかけて8.4%のCAGRを示すと予測されています。

リンパ腫はリンパ系に影響を及ぼすがんの一種で、白血球の一種であるリンパ球の異常増殖から発生します。主にリンパ節に発現し、他の組織にも影響を及ぼすことがあります。非ホジキンリンパ腫とホジキンリンパ腫があり、ホジキンリンパ腫ではリード-スタンバーグ細胞の存在によって区別されます。症状はリンパ節腫脹、発熱、疲労、食欲不振などです。ホジキンリンパ腫の罹患率は、特に若年層で依然として高いが、地域によってはヘルスケアのインフラが不十分なため、生存率が低くなっています。この格差は、特に低所得地域における治療アプローチの改善の必要性を強調しています。

非ホジキンリンパ腫(NHL)は、その高い有病率と複数のサブタイプにより市場を独占しており、世界的に患者数が多いです。罹患率の増加が引き続き市場の成長を後押ししています。リツキシマブなどのモノクローナル抗体治療がリンパ腫治療に革命をもたらしました。リツキシマブはBリンパ球上のCD20分子を標的とし、非ホジキンリンパ腫と結節性リンパ球優位型ホジキンリンパ腫(NLPHL)の両方に有効であることが証明されています。この治療法は奏効率を高め、寛解期間を延長し、生存率を向上させ、リンパ腫治療の要としての地位を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 83億米ドル |

| 予測金額 | 183億米ドル |

| CAGR | 8.4% |

非経口投与は、2024年の市場シェアの78.7%を占め、その優位性を際立たせています。血流に直接薬剤を注入するこの方法は、薬剤の吸収が速く、早急な治療が必要な侵攻性リンパ腫に最適です。非経口投与は、免疫療法、CAR T細胞療法、大量化学療法などの高度な治療にとって重要な、正確な投与と制御された送達を可能にします。重篤な症状や腸の問題のために経口薬に耐えられない患者には、このアプローチが有効です。さらに、非経口投与は経口治療に反応しない再発または難治性のリンパ腫症例に依然として好ましい方法です。

病院薬局は、化学療法、免疫療法、CAR T細胞療法などの病院投与療法が広く使用されていることを背景に、2024年には45.9%と最大の市場シェアを占めています。これらの特殊な治療には慎重な準備とモニタリングが必要であり、病院内での治療が最適です。病院の薬局は依然として、こうしたオーダーメイドの薬や高コストの生物製剤の一次情報源となっています。専門的な腫瘍治療のための入院患者数の増加は、このセグメントの市場シェアをさらに高めています。

英国では、リンパ腫治療市場は2025年から2034年にかけて安定した成長が見込まれます。同地域ではリンパ腫の有病率が増加しており、革新的な治療ソリューションに対する需要が高まっています。精密医療、免疫療法、CAR T細胞療法の進歩がこの需要に応えています。さらに、ライフサイエンス産業戦略やBrexitを契機とした権限委譲の取り組みなどのイニシアチブが、英国の技術革新能力と国内治療生産能力を強化し、同地域の市場全体の成長を後押ししています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- リンパ腫の有病率の増加

- 治療選択肢の進歩

- 新規標的療法の承認拡大

- 業界の潜在的リスク&課題

- 高い治療費

- 診断の遅れ

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- ホジキンリンパ腫

- 非ホジキンリンパ腫

第6章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- リツキサン/マブラ

- レブリミド

- インブルビカ

- アドセトリス

- キイトルーダ

- オプジーボ

- その他の薬剤

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口剤

- 非経口剤

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- AstraZeneca

- Bayer

- Biogen

- BioGene

- Bristol-Myers Squibb

- Celgene

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Gilead Sciences

- Incyte

- Johnson &Johnson

- Juno Therapeutics

- Merck

- Novartis

- Seattle Genetics

- Takeda Pharmaceutical

The Global Lymphoma Treatment Market reached USD 8.3 billion in 2024 and is projected to exhibit a CAGR of 8.4% from 2025 to 2034. Lymphoma, a type of cancer affecting the lymphatic system, arises from abnormal proliferation of lymphocytes, a form of white blood cell. It primarily manifests in lymph nodes and can also affect other tissues. There are two primary types non-Hodgkin lymphoma and Hodgkin lymphoma-distinguished by the presence of Reed-Sternberg cells in Hodgkin lymphoma. Symptoms often include lymphadenopathy, fever, fatigue, and appetite loss. The burden of Hodgkin lymphoma remains high, especially among young populations, while inadequate healthcare infrastructure in some regions contributes to lower survival rates. This disparity emphasizes the need for improved treatment approaches, particularly in low-income regions.

Non-Hodgkin lymphoma (NHL) dominates the market due to its higher prevalence and multiple subtypes, resulting in a larger patient population worldwide. Increasing incidence rates continue to propel the market's growth. The use of monoclonal antibody therapies, such as Rituximab, has revolutionized lymphoma treatment. Rituximab targets the CD20 molecule on B lymphocytes and has proven effective in managing both NHL and nodular lymphocyte predominant Hodgkin lymphoma (NLPHL). The therapy enhances response rates, prolongs remission duration, and boosts survival rates, reinforcing its position as a cornerstone in lymphoma treatment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $18.3 Billion |

| CAGR | 8.4% |

Parenteral administration accounted for 78.7% of the market share in 2024, underscoring its dominance. This method, which involves injecting medication directly into the bloodstream, ensures rapid drug absorption, making it ideal for aggressive lymphomas requiring immediate intervention. Parenteral routes allow for precise dosing and controlled delivery, which is critical for advanced therapies such as immunotherapy, CAR T-cell therapy, and high-dose chemotherapy. Patients who are unable to tolerate oral medications due to severe symptoms or bowel issues benefit from this approach. Furthermore, parenteral administration remains the preferred method for relapsed or refractory lymphoma cases that do not respond well to oral treatments.

Hospital pharmacies held the largest market share at 45.9% in 2024, driven by the widespread use of hospital-administered therapies such as chemotherapy, immunotherapy, and CAR T-cell therapies. These specialized treatments require careful preparation and monitoring, which is best handled within a hospital setting. Hospital pharmacies remain the primary source for these tailored medications and high-cost biologics. The growing volume of hospital admissions for specialized oncology care further reinforces the segment's substantial market share.

In the United Kingdom, the lymphoma treatment market is expected to witness consistent growth between 2025 and 2034. The increasing prevalence of lymphoma in the region is driving demand for innovative treatment solutions. Advancements in precision medicine, immunotherapy, and CAR T-cell therapies are meeting this demand. Additionally, initiatives such as the Life Sciences Industrial Strategy and Brexit-driven devolution efforts are strengthening the UK's capacity to innovate and produce domestic treatments, boosting the region's overall market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of lymphoma

- 3.2.1.2 Advancements in treatment options

- 3.2.1.3 Growing approval of novel targeted therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Delayed diagnosis

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hodgkin lymphoma

- 5.3 Non-Hodgkin lymphoma

Chapter 6 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Rituxan/MabThera

- 6.3 Revlimid

- 6.4 Imbruvica

- 6.5 Adcetris

- 6.6 Keytruda

- 6.7 Opdivo

- 6.8 Other drug types

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Bayer

- 10.3 Biogen

- 10.4 BioGene

- 10.5 Bristol-Myers Squibb

- 10.6 Celgene

- 10.7 Eli Lilly and Company

- 10.8 F. Hoffmann-La Roche

- 10.9 Gilead Sciences

- 10.10 Incyte

- 10.11 Johnson & Johnson

- 10.12 Juno Therapeutics

- 10.13 Merck

- 10.14 Novartis

- 10.15 Seattle Genetics

- 10.16 Takeda Pharmaceutical