|

市場調査レポート

商品コード

1708181

免疫毒素市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Immunotoxins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 免疫毒素市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

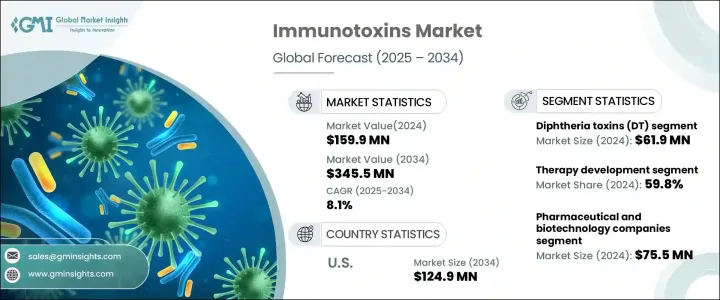

世界の免疫毒素市場は2024年に1億5,990万米ドルに達し、2025年から2034年にかけてCAGR 8.1%で成長すると予測されています。

免疫毒素は、モノクローナル抗体または標的分子と強力な毒素を組み合わせた治療薬です。そのメカニズムには、がん細胞や疾患細胞などの標的細胞表面に存在する抗原に抗体を結合させることが含まれます。その後、毒素成分が必須細胞プロセスを破壊することによって標的細胞を死滅させる。慢性疾患に対する標的療法の採用が増加していることが、市場成長の主な促進要因となっています。免疫毒素を含む標的療法は、疾患の原因となる細胞を特異的に攻撃するため、副作用が減少し、患者の転帰が改善します。こうした利点により、がんや慢性疾患管理における免疫毒素ベースの治療が増加し、市場拡大の原動力となっています。

市場は毒素の種類によって、ジフテリア毒素(DT)、炭疽菌ベースの毒素、シュードモナス外毒素(PE)、リボソーム不活性化タンパク質ベースの免疫毒素、その他の免疫毒素に区分されます。ジフテリア毒素(DT)セグメントは2024年に6,190万米ドルを占め、予測期間中にCAGR 8.1%で成長すると予想されています。この成長は、ジフテリア毒素の強力な治療ポテンシャルによるもので、標的細胞のタンパク質合成を阻害することで細胞死に至る。ジフテリア毒素とIL-2受容体標的フラグメントを組み合わせた融合タンパク質であるDenileukin diftitoxは、DTセグメントの成長を強化する殺細胞作用の一例です。特にジフテリア毒素ベースの免疫毒素に関する継続的な調査と規制当局の承認が、このセグメントの拡大にさらに貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億5,990万米ドル |

| 予測金額 | 3億4,550万米ドル |

| CAGR | 8.1% |

用途別では、生物医学研究と治療開発に分類されます。治療開発分野は2024年に59.8%のシェアで市場をリードしました。同分野の優位性は、がん罹患率の増加と臨床現場における免疫毒素の使用増加によるものです。白血病、リンパ腫、多発性骨髄腫などの血液学的悪性腫瘍の罹患率の増加が免疫毒素ベースの治療薬に対する需要を押し上げ、市場成長をさらに促進しています。

市場は最終用途に基づき、製薬・バイオテクノロジー企業、CRO・CMO、学術・研究機関、その他のエンドユーザーに分けられます。製薬・バイオテクノロジー企業は2024年に7,550万米ドルでこのセグメントを支配しています。これらの企業は、がんや慢性疾患に対する先進的な免疫毒素療法を開発するために研究開発に多額の投資を行っており、健康な細胞を温存しながら疾患細胞を標的とすることに注力しています。CRO、CMO、学術機関との提携は製品の商業化と開発を加速させ、市場開拓に大きく貢献しています。

米国の免疫毒素市場は大幅な成長が見込まれ、2034年には1億2,490万米ドルに達します。がん罹患率の増加と死亡率の上昇が、標的免疫毒素をベースとした治療法の需要を促進しており、同国市場の存在感をさらに高めています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- がんと慢性疾患の有病率の上昇

- 新規免疫毒素療法の承認拡大

- 標的治療への注目の高まり

- 業界の潜在的リスク&課題

- 免疫毒素開発における細胞毒性と製造に関する課題

- 促進要因

- 成長可能性分析

- 規制状況

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:毒素タイプ別、2021年~2034年

- 主要動向

- ジフテリア毒素(DT)

- 炭疽菌由来毒素

- シュードモナス外毒素(PE)

- リボソーム不活性化タンパク質ベースの免疫毒素

- その他の毒素タイプ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- バイオメディカル研究

- 治療開発

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製薬企業およびバイオテクノロジー企業

- CROおよびCMO

- 学術・研究機関

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Abcam

- Bio-Techne

- Cayman Chemical

- Creative Biolabs

- Enzo Biochem

- List Biological Labs

- Merck KGaA

- Quadratech Diagnostics

- Santa Cruz Biotechnology

- The Native Antigen Company

- Thermo Fisher Scientific

The Global Immunotoxins Market reached USD 159.9 million in 2024 and is expected to grow at a CAGR of 8.1% from 2025 to 2034. Immunotoxins are therapeutic agents that combine a monoclonal antibody or a targeting molecule with a potent toxin. Their mechanism involves binding the antibody to antigens present on the surface of target cells, such as cancerous or diseased cells. The toxin component then kills the targeted cells by disrupting essential cellular processes. The increasing adoption of targeted therapies for chronic conditions is a major driver of market growth. Targeted therapies, including immunotoxins, specifically attack disease-causing cells, reducing adverse reactions and improving patient outcomes. These benefits are driving the increased use of immunotoxin-based treatments in cancer and chronic disease management, fueling market expansion.

The market is segmented by toxin type into diphtheria toxins (DT), anthrax-based toxins, pseudomonas exotoxins (PE), ribosome-inactivating protein-based immunotoxins, and other immunotoxins. The diphtheria toxins (DT) segment accounted for USD 61.9 million in 2024 and is expected to grow at a CAGR of 8.1% during the forecast period. This growth is attributed to the strong therapeutic potential of diphtheria toxins, which work by inhibiting protein synthesis in targeted cells, leading to cell death. Denileukin diftitox, a fusion protein that combines diphtheria toxin with an IL-2 receptor-targeting fragment, exemplifies the cytocidal action that reinforces the growth of the DT segment. Ongoing research and regulatory approvals, particularly for diphtheria toxin-based immunotoxins, further contribute to the expansion of this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $159.9 Million |

| Forecast Value | $345.5 Million |

| CAGR | 8.1% |

By application, the market is categorized into biomedical research and therapy development. The therapy development segment led the market with a 59.8% share in 2024. Its dominance is driven by the increasing prevalence of cancer and the rising use of immunotoxins in clinical settings. The growing incidence of hematological malignancies such as leukemia, lymphoma, and multiple myeloma is boosting the demand for immunotoxin-based therapies, further propelling market growth.

Based on end use, the market is divided into pharmaceutical and biotechnology companies, CROs and CMOs, academic and research institutes, and other end users. Pharmaceutical and biotechnology companies dominated the segment with USD 75.5 million in 2024. These companies invest extensively in research and development to create advanced immunotoxin therapies for cancer and chronic diseases, focusing on targeting diseased cells while preserving healthy ones. Their collaborations with CROs, CMOs, and academic institutions accelerate product commercialization and development, contributing significantly to market growth.

The U.S. immunotoxins market is expected to witness substantial growth, reaching USD 124.9 million by 2034. The increasing prevalence of cancer and rising mortality rates are driving demand for targeted immunotoxin-based therapies, further strengthening the country's market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer and chronic diseases

- 3.2.1.2 Expanding regulatory approvals for new immunotoxin therapies

- 3.2.1.3 Growing focus on targeted therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Challenges related to cytotoxicity and manufacturing in the development of immunotoxins

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Toxin Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diphtheria toxins (DT)

- 5.3 Anthrax based toxins

- 5.4 Pseudomonas exotoxins (PE)

- 5.5 Ribosomes inactivating protein based immunotoxins

- 5.6 Other toxin types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Biomedical research

- 6.3 Therapy development

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical and biotechnology companies

- 7.3 CROs and CMOs

- 7.4 Academic and research institutes

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abcam

- 9.2 Bio-Techne

- 9.3 Cayman Chemical

- 9.4 Creative Biolabs

- 9.5 Enzo Biochem

- 9.6 List Biological Labs

- 9.7 Merck KGaA

- 9.8 Quadratech Diagnostics

- 9.9 Santa Cruz Biotechnology

- 9.10 The Native Antigen Company

- 9.11 Thermo Fisher Scientific