内視鏡検査におけるAIの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

AI in Endoscopy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708171

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

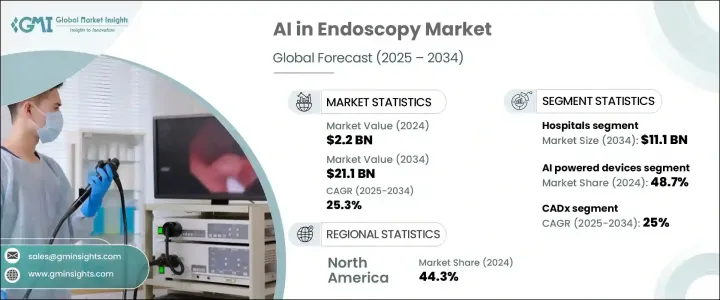

内視鏡検査におけるAIの世界市場は、2024年に22億米ドルと評価され、2025年から2034年にかけて25.3%の堅調なCAGRで拡大すると予測されています。

この市場の急成長は、世界の消化器疾患および関連疾患の急増による高度な診断ツールに対する需要の増加を反映しています。大腸がん、炎症性腸疾患、消化性潰瘍などの消化器疾患が増加の一途をたどるなか、ヘルスケアシステムは、より正確で迅速かつ信頼性の高い診断を提供するソリューションを早急に求めています。AIを活用した内視鏡検査は、臨床医がリアルタイムで異常を検出して治療する方法を再構築する変革的なツールとして台頭しています。人工知能は現在、診断精度の向上、臨床ワークフローの合理化、予測的洞察の提供において極めて重要な役割を果たしており、これらすべてが患者の転帰改善に寄与しています。

内視鏡検査にAIを組み込むことで、医師は病変、腫瘍、ポリープをより高い精度で特定できるようになり、人為的ミスを大幅に減らし、早期診断率を向上させることができます。世界中のヘルスケアプロバイダーが低侵襲手技に重点を置く中、AI技術は、強化された視覚化、リアルタイム分析、自動検出を提供し、最終的に臨床的意思決定プロセスを改善する上で不可欠となっています。AIアルゴリズムの継続的な進化は、高精細画像やロボット支援プラットフォームの統合と相まって、AIベースの内視鏡ソリューションの需要をさらに促進しており、この市場は医療機器メーカーやヘルスケア機関にとっても同様に重要な焦点となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 211億米ドル |

| CAGR | 25.3% |

内視鏡検査におけるAI市場は、胃腸、泌尿器、呼吸器、大腸内視鏡、その他など、手技の種類に基づいてセグメント化されます。このうち、消化器内視鏡検査分野が市場を独占し、2023年には6億3,120万米ドルを創出したが、これは主に消化器疾患の有病率の上昇に後押しされたものです。コンピュータ支援検出(CADe)システムなどのAI主導型ソリューションは、ポリープや腫瘍などの異常の正確な同定を可能にすることで、胃腸内視鏡検査に変革をもたらしつつあります。AIを活用したリアルタイムのビデオ解析や画像強調技術を特徴とするツールは、診断速度と精度を向上させ、迅速な臨床介入を促進しています。こうした進歩により、病院や診療所では、標準的な診断プロトコルの一部としてAIベースの内視鏡検査ツールを採用するようになっています。

コンポーネントの観点から、市場はAI搭載デバイス、ソフトウェア、サービスに分けられます。AI搭載デバイスセグメントは2024年に48.7%のシェアを占め、高度な診断および可視化技術への嗜好の高まりに支えられています。これらのデバイスは、ヘルスケアプロバイダーがより的を絞った効率的な内視鏡処置を行うことを可能にし、より迅速な診断と治療をサポートしています。低侵襲介入へのシフトは、リアルタイムのAI機能と相まって、最適化された結果を得るためのAIソフトウェアとシームレスに統合されたコンパクトで高性能な内視鏡ツールの開発における重要な技術革新を推進しています。

地域別では、北米が2024年に44.3%のシェアで内視鏡検査におけるAI市場をリードしており、強力なヘルスケア・インフラとAI技術の早期導入により米国が先陣を切っています。技術プロバイダーと医療機関の継続的な共同開発が革新的な製品開発を促進し、市場浸透を加速させています。同地域の研究開発への積極的な投資と、手続き効率と患者ケアを改善するためのAIの統合への注力は、世界市場における同地域の地位を引き続き強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 消化器疾患および呼吸器疾患の有病率の増加

- 低侵襲手術の採用増加

- リアルタイムの画像診断と診断のためのAIアルゴリズムの進歩

- 業界の潜在的リスク&課題

- 高い導入コストと設備コスト

- AI導入における規制・倫理上の課題

- 促進要因

- 成長可能性分析

- 規制状況

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:内視鏡タイプ別、2021年~2034年

- 主要動向

- 消化器内視鏡

- 泌尿器内視鏡

- 呼吸器内視鏡

- 大腸内視鏡

- その他のタイプ

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- AI搭載デバイス

- ソフトウェア

- サービス

第7章 市場推計・予測:CADタイプ別、2021年~2034年

- 主要動向

- CADx

- CADe

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 専門クリニック

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Ambu

- Fujifilm

- Hoya

- Intuitive Surgical

- Iterative Scopes

- Magentiq Eye

- Medtronic

- NEC Corporation

- Odin Vision

- Olympus

- PENTAX Medical

- Wision Al

- Wuhan EndoAngel Medical Technology

目次

The Global AI in Endoscopy Market was valued at USD 2.2 billion in 2024 and is projected to expand at a robust CAGR of 25.3% from 2025 to 2034. The rapid growth of this market reflects the increasing demand for advanced diagnostic tools driven by a surge in gastrointestinal and related disorders worldwide. As gastrointestinal diseases, including colorectal cancer, inflammatory bowel disease, and peptic ulcers, continue to rise, healthcare systems are urgently seeking solutions that offer more accurate, faster, and reliable diagnoses. AI-powered endoscopy is emerging as a transformative tool that is reshaping how clinicians detect and treat abnormalities in real time. Artificial intelligence is now playing a pivotal role in enhancing diagnostic accuracy, streamlining clinical workflows, and delivering predictive insights, all contributing to better patient outcomes.

The integration of AI in endoscopy procedures allows physicians to identify lesions, tumors, and polyps with higher precision, significantly reducing human error and improving early diagnosis rates. With healthcare providers worldwide focusing on minimally invasive procedures, AI technologies are becoming essential in providing enhanced visualization, real-time analysis, and automated detection, ultimately improving clinical decision-making processes. The continuous evolution of AI algorithms, coupled with the integration of high-definition imaging and robotic-assisted platforms, is further driving the demand for AI-based endoscopy solutions, making this market a critical focus for medical device manufacturers and healthcare institutions alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $21.1 Billion |

| CAGR | 25.3% |

The AI in endoscopy market is segmented based on procedure types, including gastrointestinal, urological, respiratory, colonoscopy, and others. Among these, the gastrointestinal endoscopy segment dominated the market and generated USD 631.2 million in 2023, largely propelled by the rising prevalence of gastrointestinal conditions. AI-driven solutions such as computer-aided detection (CADe) systems are transforming gastrointestinal endoscopy by enabling precise identification of abnormalities like polyps and tumors. Tools featuring AI-powered real-time video analysis and image enhancement technologies are improving diagnostic speeds and accuracy, facilitating quicker clinical interventions. These advancements are encouraging hospitals and clinics to adopt AI-based endoscopy tools as part of their standard diagnostic protocols.

From a component perspective, the market is divided into AI-powered devices, software, and services. The AI-powered devices segment accounted for a 48.7% share in 2024, underpinned by the growing preference for advanced diagnostic and visualization technologies. These devices are enabling healthcare providers to perform more targeted and efficient endoscopic procedures, supporting faster diagnosis and treatment. The shift toward minimally invasive interventions, coupled with real-time AI capabilities, is driving significant innovations in the development of compact, high-performance endoscopic tools that integrate seamlessly with AI software for optimized outcomes.

Regionally, North America led the AI in endoscopy market with a 44.3% share in 2024, spearheaded by the U.S. due to its strong healthcare infrastructure and early adoption of AI technologies. Ongoing collaborations between technology providers and healthcare institutions are fostering innovative product development and accelerating market penetration. The region's proactive investment in R&D and focus on integrating AI to improve procedural efficiency and patient care continue to strengthen its position in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of gastrointestinal and respiratory diseases

- 3.2.1.2 Rising adoption of minimally invasive surgeries

- 3.2.1.3 Advancements in AI algorithms for real-time imaging and diagnostics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and equipment costs

- 3.2.2.2 Regulatory and ethical challenges in AI deployment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type of Endoscopy, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Gastrointestinal endoscopy

- 5.3 Urological endoscopy

- 5.4 Respiratory endoscopy

- 5.5 Colonoscopy

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 AI powered devices

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By Type of CAD, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 CADx

- 7.3 CADe

Chapter 8 Market Estimates and Forecast, End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 Fujifilm

- 10.3 Hoya

- 10.4 Intuitive Surgical

- 10.5 Iterative Scopes

- 10.6 Magentiq Eye

- 10.7 Medtronic

- 10.8 NEC Corporation

- 10.9 Odin Vision

- 10.10 Olympus

- 10.11 PENTAX Medical

- 10.12 Wision Al

- 10.13 Wuhan EndoAngel Medical Technology

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日